Investing

Investing

Most Canadians open an RRSP, start contributing, and pick a few ETFs.

That part they get right.

What they miss is the next step — deciding where each investment should actually live. Because putting the same portfolio inside every account is one of the most common and quietly expensive mistakes in personal finance.

An RRSP isn’t just a retirement account. It’s a tax strategy. And when you use it like one, you can end up with meaningfully more money at retirement without changing a single investment.

This guide breaks down exactly what to hold in your RRSP, what to keep out of it, and why the placement matters more than most people realize.

This article contains affiliate links. We may earn a commission if you open an account — at no cost to you. We only recommend products we’ve researched and trust.

- Quick Answer

- Who This Guide Is For

- What an RRSP Actually Does

- The Core Idea: Asset Location

- What to Hold in Your RRSP

- What NOT to Hold in Your RRSP

- Asset Location at a Glance

- A Real Example

- Common Mistakes That Cost You Money

- How This Fits Into Your Bigger Financial Picture

- The Bottom Line

- Frequently Asked Questions

Quick Answer

The best investments to hold in an RRSP in Canada are tax-inefficient assets — things like bonds, REITs, and U.S. dividend stocks. These benefit the most from tax deferral and are taxed heavily when held outside a registered account. High-growth investments, on the other hand, are usually better placed in a TFSA, where gains are completely tax-free. The rest of this guide shows you how that plays out in practice — and how to set up your accounts so they work together.

Who This Guide Is For

- You have an RRSP and you’re wondering if you’re using it the right way

- You have both an RRSP and a TFSA and don’t know which investments go where

- You’re just getting started investing and want to set things up correctly from the beginning

- You’ve been holding the same portfolio across every account and want to know if there’s a smarter approach

What an RRSP Actually Does

Before you can decide what to hold inside your RRSP, it helps to be clear on how the account works.

When you contribute to an RRSP, you get a tax deduction upfront — meaning you reduce your taxable income in the year you contribute. Your investments then grow tax-deferred inside the account. And when you eventually withdraw, that money is taxed as income.

That last part is the one most people gloss over.

Everything that comes out of an RRSP is taxed as income — no matter how it grew. There’s no capital gains rate. No dividend tax credit. Just income tax at whatever bracket you’re in.

That changes how you should think about what you put in there.

The goal isn’t just to grow your investments. It’s to use the RRSP to shelter the investments that are taxed the most heavily outside of it — so your overall tax bill over your lifetime is as low as possible.

When you see it that way, the strategy becomes a lot clearer — and it’s the same thinking that drives the decision of whether an RRSP or TFSA deserves your money first.

The Core Idea: Asset Location

There’s a strategy that most financial advisors use but rarely explain clearly to their clients. It’s called asset location — and it’s simply the idea that where you hold an investment matters as much as what you hold.

Not all investments are taxed the same when held in a taxable account:

- Interest income From bonds and GICs — taxed at your full marginal rate every year

- U.S. dividends Subject to a 15% withholding tax outside an RRSP

- REIT distributions Often classified as income — taxed at full marginal rate

- Canadian dividends Benefit from the dividend tax credit — already tax-efficient

- Capital gains Only 50% taxable in Canada — also relatively efficient

The RRSP shelters everything inside it from annual taxation. So the question becomes: which investments benefit most from that shelter?

What to Hold in Your RRSP in Canada

Bonds and Fixed Income

Bonds are almost universally better inside an RRSP.

Outside a registered account, interest income is taxed at your full marginal rate every year — even if you don’t sell anything. If you’re in a 40% tax bracket, you’re handing 40 cents of every dollar of interest to the government, annually.

Inside an RRSP, that tax is deferred until withdrawal. Your bond returns compound at their full rate, year after year.

For most investors, a simple bond ETF like iShares Core Canadian Universe Bond Index ETF (XBB) or Vanguard Canadian Aggregate Bond Index ETF (VAB) is a sensible choice to hold here.

U.S. Dividend Stocks and ETFs

This one surprises a lot of people.

When you hold U.S. dividend-paying stocks or ETFs in a TFSA, the U.S. government withholds 15% of your dividends before you even see them — and Canada doesn’t give you a tax credit to offset it. That money is just gone.

Inside an RRSP, it’s different. Thanks to the Canada–U.S. tax treaty, U.S. dividends are not subject to withholding tax when held in an RRSP. The full dividend comes through.

This means an ETF like VTI (Vanguard Total Stock Market ETF) or VYM (Vanguard High Dividend Yield ETF) should generally live in your RRSP, not your TFSA — even though TFSA growth is tax-free.

REITs (Real Estate Investment Trusts)

REITs are real estate investments you can buy on the stock market, and they’re required to distribute most of their income to shareholders.

The problem is those distributions are often classified as income rather than capital gains or dividends — which makes them taxed at your full marginal rate in a non-registered account.

Inside an RRSP, that income tax drag disappears and the distributions compound tax-deferred. Over a long holding period, that difference adds up.

Actively Managed or Higher-Turnover Funds

If you use any actively managed funds that trade frequently, they tend to generate more taxable events — realized gains distributed to you each year. In a non-registered account, you pay tax on those every single year.

Inside an RRSP, that’s a non-issue. Everything compounds tax-deferred regardless of how often the fund trades.

What NOT to Hold in Your RRSP

Knowing what to keep out is just as important.

Canadian Dividend Stocks

This one catches a lot of investors off guard.

Canadian dividend stocks — like the big banks, utilities, or telecom companies — are actually quite tax-efficient when held in a non-registered account. They benefit from the dividend tax credit, which significantly reduces the effective tax rate on that income.

Inside an RRSP, that advantage disappears entirely. The dividends compound tax-deferred, which sounds good — but when you eventually withdraw, it all comes out as income, and you lose the tax credit completely.

For Canadian dividend stocks, a non-registered taxable account is usually the better home.

High-Growth Investments

Here’s the trade-off that trips people up.

Your RRSP defers tax. Your TFSA eliminates it.

If you hold a high-growth investment inside your RRSP and it 10x’s over 30 years, every dollar of that gain eventually gets taxed as income when you withdraw. If you hold that same investment in a TFSA, the entire gain is yours — zero tax.

The math almost always favours putting your highest-growth assets in your TFSA and your income-heavy assets in your RRSP. If you’re still deciding which account to prioritize, our RRSP vs TFSA breakdown walks through exactly how to choose based on your income and timeline.

Cash and Short-Term Savings

Holding cash or very short-term savings in your RRSP uses up valuable contribution room without meaningfully benefiting from tax deferral.

If you need liquid savings, that money belongs outside your registered accounts — in a high-interest savings account or set aside as part of your emergency fund — somewhere accessible, with no contribution room implications.

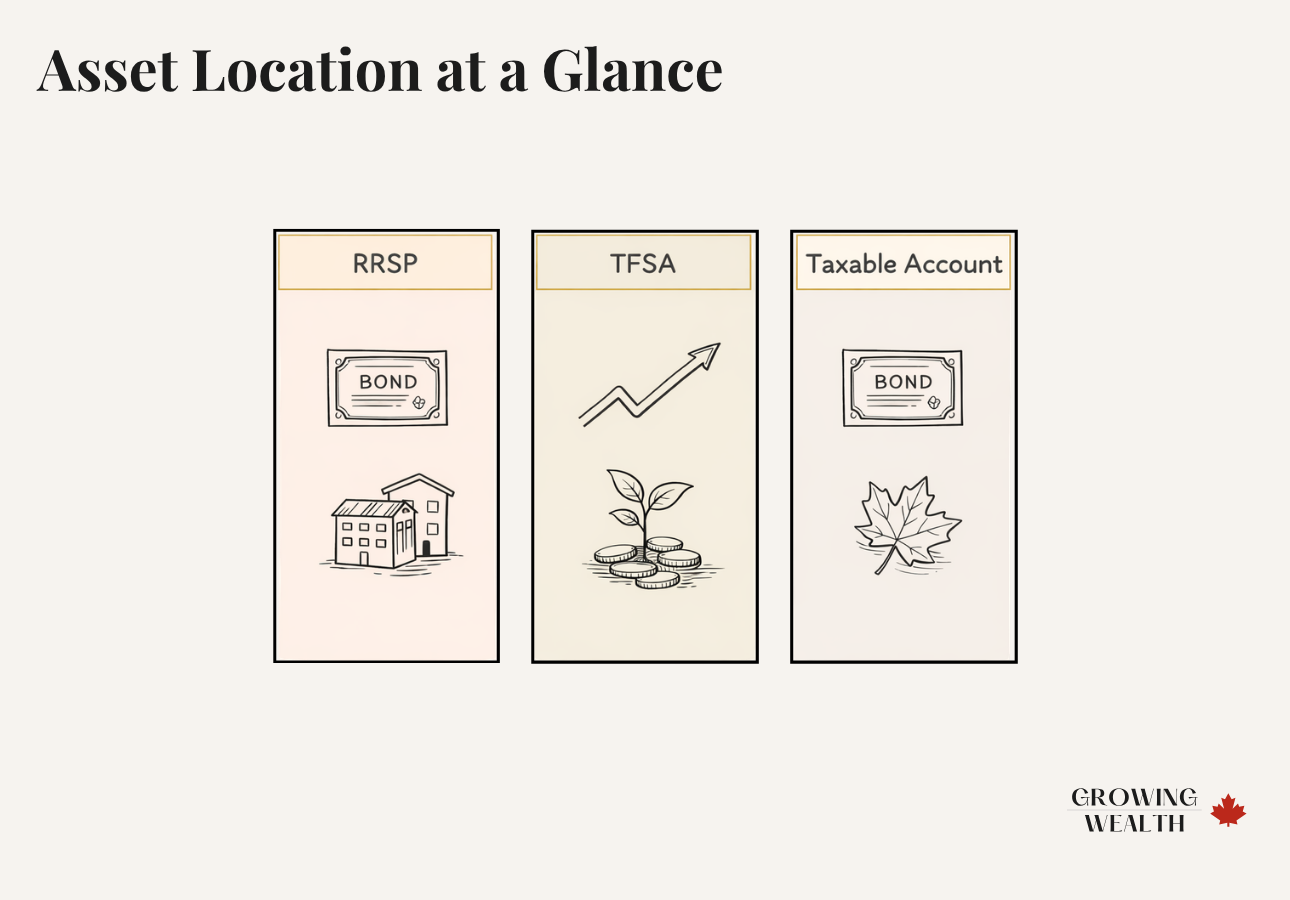

Asset Location at a Glance

Once you’re thinking in terms of asset location, here’s how the three account types divide up:

| Investment Type | Best Account | Why |

|---|---|---|

| Bonds / Bond ETFs | RRSP | Interest taxed at full rate outside |

| U.S. Dividend Stocks / ETFs | RRSP | No withholding tax via Canada–U.S. treaty |

| REITs | RRSP | Distributions taxed as income outside |

| High-Growth ETFs / Stocks | TFSA | Gains grow and withdraw completely tax-free |

| Canadian Dividend Stocks | Taxable Account | Dividend tax credit makes them efficient outside |

| Cash / Emergency Fund | Outside registered accounts | Needs accessibility; don’t waste contribution room |

Where each investment type belongs — bonds and REITs in your RRSP, growth assets in your TFSA, and Canadian dividend stocks in a taxable account where they keep their tax advantage.

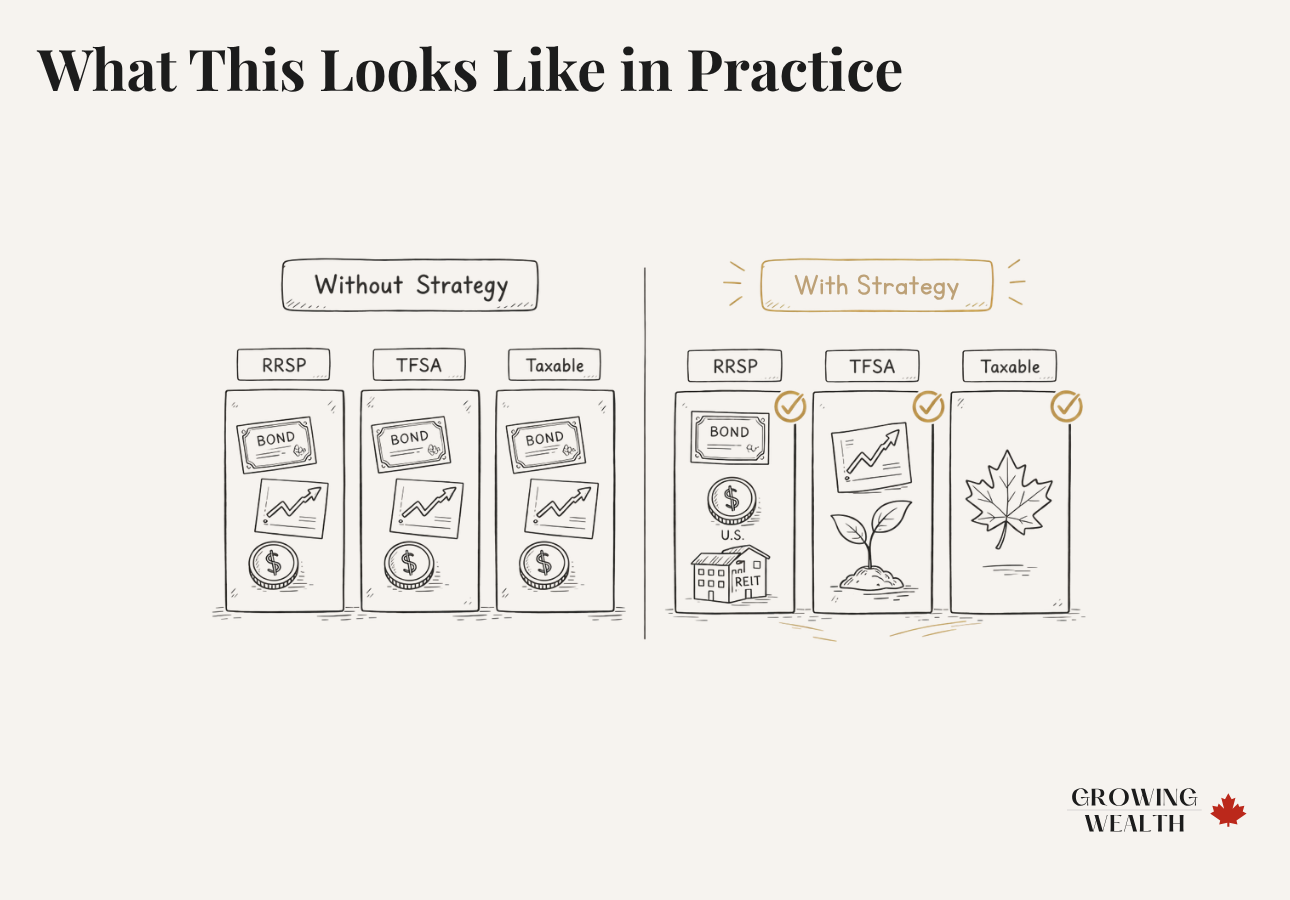

A Real Example: What This Looks Like in Practice

Say you’re a Canadian household earning around $110,000 with the following investments:

- 🇨🇦 Canadian equity ETF (VCN)

- 🇺🇸 U.S. equity ETF (VTI)

- 📊 Bond ETF (XBB)

- 🏦 A few Canadian bank stocks

Without a strategy, the same investments end up everywhere. With asset location, each account holds what it’s actually designed for.

- All four investments spread randomly across RRSP, TFSA, and taxable

- No thought given to which account best suits each asset

- Works — but quietly costs you in unnecessary tax drag

- RRSP: XBB (bond ETF) + VTI (U.S. equity)

- TFSA: VCN (Canadian equity ETF)

- Taxable: Canadian bank stocks (keep the dividend tax credit)

Nothing about the investments changes. Only where they live.

Over 20–30 years, the tax savings from this kind of intentional placement can be significant — not because you picked better investments, but because you reduced the drag on the ones you already had.

Common Mistakes That Cost You Money

Holding the Same Portfolio Everywhere

This is by far the most common issue. It’s tempting to simplify by having identical holdings in your RRSP, TFSA, and non-registered account. But it ignores the completely different tax treatment each account provides.

Treating the RRSP as a “Safe” Account for Cash

Some people put GICs or cash inside their RRSP because it feels conservative. But low-return, short-term money doesn’t benefit from tax deferral. You’re using up contribution room that can never be recovered.

Ignoring Withdrawal Tax When Choosing Investments

Every dollar inside your RRSP will eventually be taxed as income. That has implications for how aggressively you should use it and what you put in there. If you plan to have a high income in retirement, RRSP withdrawals could push you into a high tax bracket — which changes the strategy. Understanding how RRSP contributions reduce your taxes and where to actually invest inside your RRSP are good next steps once the basics are in place.

How This Fits Into Your Bigger Financial Picture

Asset location is just one piece of a larger system.

It works best when you’ve already handled the foundations: an emergency fund, a manageable debt load, and a clear plan for how much you’re saving each month.

Once those are in place, thinking about where your investments live is one of the higher-leverage things you can do — because it improves your outcome without requiring more money, more risk, or more effort. It’s the kind of decision that fits naturally into a simple family finance system, works well alongside a consistent investing approach like dollar-cost averaging, and compounds over time when backed by strong financial habits.

The Bottom Line

Most investors focus almost entirely on what to buy.

The investors who end up with more money at retirement tend to focus on where things live too.

Your RRSP is best used for the investments that get taxed the hardest outside of it — bonds, U.S. dividends, REITs. Your TFSA is best used for your highest-growth assets, where those gains can compound and withdraw completely tax-free.

That’s the whole strategy. It doesn’t require complicated trades or a financial advisor. It just requires understanding that each account plays a different role — and placing your investments accordingly.

The right investments in the right accounts. That’s how you keep more of what you earn.Now that you know what to hold in your RRSP, read RRSP vs TFSA: Which Should You Prioritize? — the complete guide to deciding which account deserves your money first based on your income and timeline.

Frequently Asked Questions

The best investments for an RRSP are tax-inefficient assets — bonds, REITs, and U.S. dividend-paying stocks or ETFs. These are taxed heavily in non-registered accounts, so they benefit the most from the RRSP’s tax deferral.

Yes, ETFs are one of the most popular and practical investments for an RRSP. Bond ETFs and U.S.-focused equity ETFs are especially effective because they align well with the RRSP’s tax advantages while keeping costs low.

For U.S. dividend-paying stocks and ETFs, the RRSP is almost always better. Under the Canada–U.S. tax treaty, U.S. dividends are not subject to the 15% withholding tax when held in an RRSP. That same exemption does not apply in a TFSA.

A straightforward approach for beginners: hold a bond ETF and a U.S. broad-market ETF in your RRSP, and hold Canadian equity or global growth ETFs in your TFSA. Keep it simple, keep costs low, and revisit as your portfolio grows.

Yes. An RRSP is an account type, not a guaranteed investment. Your returns depend entirely on what you hold inside it. Stocks, ETFs, and mutual funds all carry market risk.

In most cases, no. Cash doesn’t take advantage of tax deferral, and holding it in your RRSP wastes contribution room that you can never get back. If you need liquid savings, keep them in a high-interest savings account outside your registered accounts.

The RRSP gives you a tax deduction today but taxes your withdrawals as income later. The TFSA gives no upfront deduction but lets your investments grow and be withdrawn completely tax-free. That difference is why high-growth investments tend to belong in a TFSA, and income-heavy investments tend to belong in an RRSP.

There’s no magic number, but most Canadians do well with two to four ETFs covering bonds, U.S. equity, and possibly international equity. The key isn’t how many — it’s whether the right assets are in the right account.

It depends on your income. If you’re in a high tax bracket now and expect to be in a lower bracket in retirement, prioritizing your RRSP makes sense — the deduction is worth more today. If you’re in a lower bracket or expect higher income in retirement, the TFSA often wins. Most families benefit from contributing to both. For a deeper breakdown, see our RRSP vs TFSA guide.

Asset location is the strategy of placing each investment in the account type that gives it the best tax treatment. Bonds in your RRSP. Growth stocks in your TFSA. Canadian dividend stocks in a taxable account. It doesn’t change what you invest in — just where you hold it. Over decades, that difference can add up to thousands of dollars in tax savings.