Registered Accounts

Registered Accounts

This article contains affiliate links. We may earn a commission if you open an account — at no cost to you. We only recommend products we’ve researched and trust.

Every spring, Canadians compare RRSP refund sizes like they’re scores on a test — bigger is better, and a smaller refund means something went wrong. It doesn’t work that way. The refund itself tells you almost nothing. What actually matters is your marginal tax rate, because that single number determines whether a $10,000 RRSP contribution saves you $2,000 or $4,300 — and whether an RRSP is even the right move for you this year compared to a TFSA. This article walks through the real math, using actual 2025 tax brackets and three Canadian income levels, so you can see exactly where you land.

Is an RRSP Contribution Worth It for You?

Before the full explanation, here’s the direct answer based on your situation. All scenarios assume Ontario rates.

| Your Situation | RRSP Recommendation |

|---|---|

| Income above $100,000 | Strong yes. Marginal rate is ~43%. Every $1,000 contributed saves roughly $430 in tax this year. |

| Income $60,000–$100,000 | Yes, especially if you expect lower income in retirement. Marginal rate ~30–43%. Solid deduction value. |

| Income below $50,000 | Consider TFSA first. Low marginal rate means the deduction is modest. TFSA flexibility is often more valuable. |

| Expecting a big income year (bonus, commission, parental leave ending) | Yes, and contribute this year specifically. The deduction is worth more when your income is elevated. |

| No emergency fund yet | Not yet. RRSP money is hard to access without tax consequences. Build your emergency fund first. |

In This Article

- How the RRSP Tax Deduction Works

- Real Canadian Examples at Three Income Levels

- Why the Same Contribution Saves More at Higher Incomes

- The Refund vs. Tax Savings Distinction

- Contribution Room and the 2026 Limit

- The Spousal RRSP Strategy

- When RRSP Contributions Make Sense — and When They Don’t

- Where to Open Your RRSP

- Frequently Asked Questions

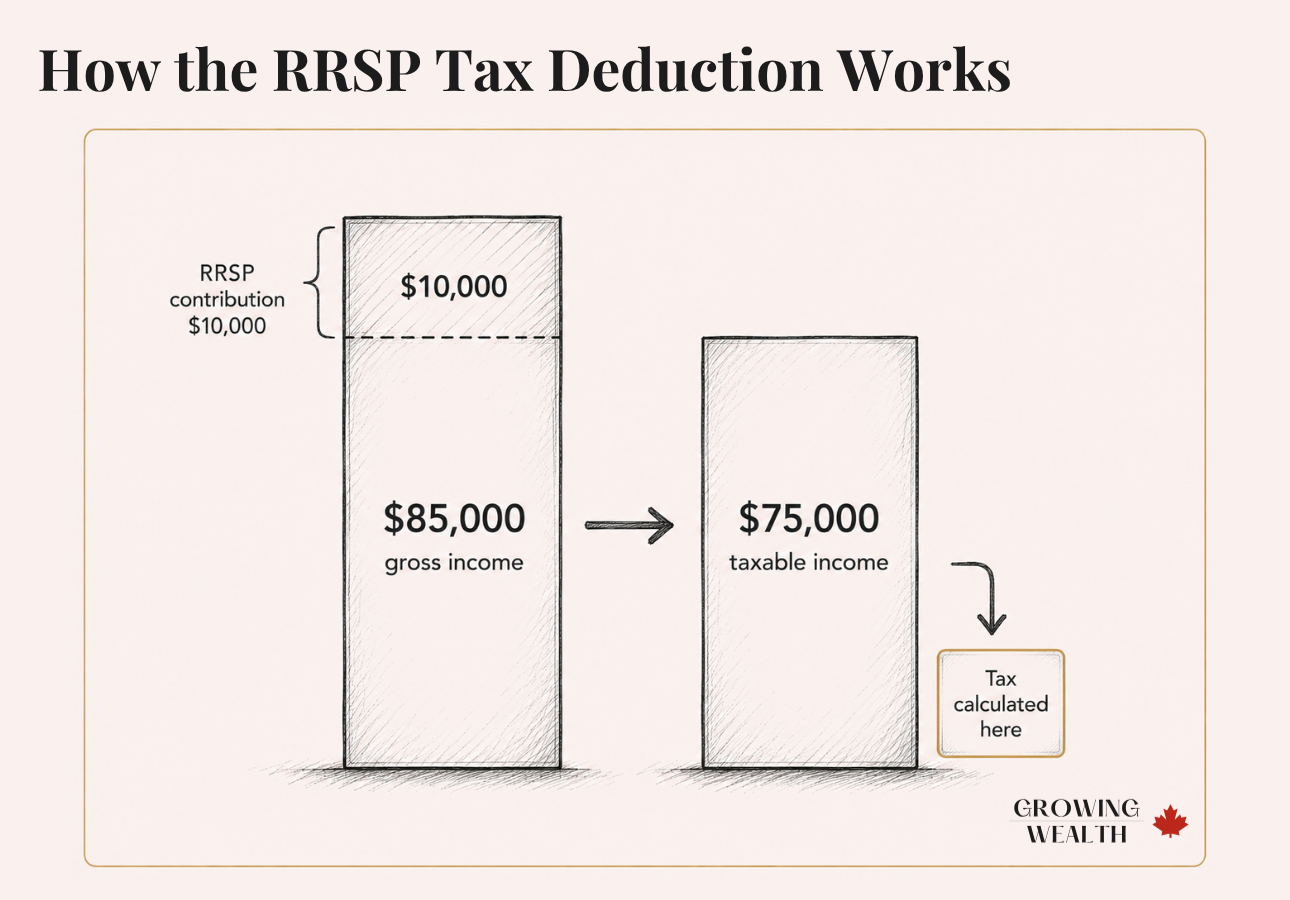

How the RRSP Tax Deduction Works

An RRSP contribution gives you a tax deduction — not a tax credit. That distinction is worth understanding before anything else.

A tax credit reduces the tax you owe directly. A tax deduction reduces your taxable income. RRSPs fall into the second category: when you contribute, that amount is subtracted from your income before the CRA calculates what you owe.

The mechanics on your tax return follow this sequence:

Employment, self-employment, rental income, or other sources — all counted as gross income.

Your RRSP contribution is subtracted here, along with any other eligible deductions.

What remains after deductions is your taxable income — the number the CRA actually taxes.

Both levels of tax are calculated on that lower taxable income — resulting in a smaller bill.

So if you earned $85,000 in Ontario and contributed $10,000 to your RRSP, the CRA taxes you as if you earned $75,000. You don’t avoid tax on that $10,000 permanently — you defer it until you withdraw it in retirement, ideally in a lower-income year.

A reliable formula for estimating your tax savings:

RRSP contribution × your marginal tax rate ≈ tax reduction this year

Your marginal tax rate is the combined federal + provincial rate applied to your last dollar of income. It’s not a flat rate on your whole income — only the top slice. This is why the same RRSP contribution saves different amounts depending on how much you earn.

To understand how Canada’s tax system works in more depth — including how federal and provincial taxes stack — that’s worth reading before diving into registered accounts.

Real Canadian Examples at Three Income Levels

These examples use 2025 combined federal + Ontario provincial marginal rates. Your province and exact income will produce slightly different numbers, but the proportions hold across the country.

Federal: 14.5% on income in the first bracket

Ontario: 9.15% on income above $52,886 + 5.05% on income below

$5,000 contribution × 29.65% = ~$1,483 in tax savings

Taxable income drops from $55,000 → $50,000

The deduction exists and it’s real money, but at this income level the TFSA deserves a serious look first. Jamie’s marginal rate is relatively low, and TFSA withdrawals are tax-free — a meaningful advantage if she might need the funds before retirement.

Federal: 20.5% on income above $57,375

Ontario: 9.15% on income above $52,886

Ontario surtax begins to apply above $100K, not yet relevant

$10,000 contribution × 33.89% = ~$3,389 in tax savings

Taxable income drops from $85,000 → $75,000

This is the sweet spot for RRSP contributions. Marcus is solidly in a bracket where deferrals are meaningful, and if he expects to retire at a lower income, he’s locking in a real long-term advantage. A $10,000 contribution in a marginal 33.89% bracket today might be withdrawn in retirement at 20–25% — that’s a permanent tax saving, not just a deferral.

Federal: 26% on income above $114,750

Ontario: 11.16% on income above $105,776

Ontario surtax adds ~2.25% effective above this level

$15,000 contribution × 43.41% = ~$6,512 in tax savings

Taxable income drops from $130,000 → $115,000

At this income, the RRSP is one of the most powerful tax tools available to Priya. She’s shielding income taxed at 43 cents on the dollar. Even if she withdraws at a 30% rate in retirement, she keeps the difference — roughly 13 cents per dollar — permanently. On a $15,000 contribution that’s nearly $2,000 in structural tax savings over and above the deferral value.

Why the Same Contribution Saves More at Higher Incomes

The same $10,000 RRSP contribution can save you $2,000 or $4,300 depending purely on your income. This is Canada’s progressive tax bracket system at work.

Canada taxes income in layers. The first portion of your income is taxed at the lowest federal rate. As your income climbs through successive brackets, each additional dollar is taxed at a higher rate — your “marginal rate.” Your RRSP contribution reduces your taxable income from the top down, so it always displaces the income that was being taxed at your highest rate. You can see the current federal rates directly on the CRA’s tax rate page.

| Income (Ontario) | Marginal Rate | Tax Saved on $10,000 RRSP |

|---|---|---|

| $50,000 | ~29.65% | ~$2,965 |

| $85,000 | ~33.89% | ~$3,389 |

| $130,000 | ~43.41% | ~$4,341 |

This is why the common advice “max your RRSP every year” oversimplifies things. A $10,000 contribution by someone earning $45,000 saves roughly $1,400 less than the same contribution by someone earning $130,000. Neither is wrong — but the value proposition is very different.

The Refund vs. Tax Savings Distinction

One of the most consistent misunderstandings about RRSPs: the refund is not the same thing as your tax savings.

“I got a $3,000 refund from my RRSP contribution, so I saved $3,000 in taxes.”

Your employer withheld tax assuming no RRSP contribution. The refund is overpaid tax being returned — it would exist regardless.

Here’s the actual sequence:

Calculated on your full salary — with no RRSP deduction factored in.

The contribution reduces your taxable income on your T1 return.

Based on the lower taxable income — less tax was genuinely owed than was withheld.

What was withheld minus what was owed — your money, returned. Not a government bonus.

The refund is real money, but it’s not the full picture. The actual tax advantage of an RRSP is tax deferral: you avoid tax now at your working-years marginal rate, and pay tax later at your retirement marginal rate — which is typically lower.

If you contribute $10,000 while earning $130,000 (43% bracket) and eventually withdraw it in retirement at $60,000 income (29% bracket), you’ve permanently saved approximately $1,400 in tax on that $10,000 — in addition to years of tax-sheltered growth inside the account.

The practical takeaway: don’t evaluate RRSP decisions based on the refund size alone. Evaluate them based on the tax rate difference between now and retirement. That spread is the real return.

Contribution Room and the 2026 Limit

You can’t simply contribute whatever you want — every Canadian has a personal RRSP contribution limit, and exceeding it triggers penalties.

Your personal limit for 2026 is the lesser of $33,810 or 18% of your 2025 earned income, plus any unused contribution room carried forward from previous years. So if you earned $100,000 in 2025, you generated $18,000 in new room for 2026 — well under the $33,810 ceiling.

Unused room carries forward indefinitely. If you didn’t contribute last year (or for several years), that room accumulates and you can use it any time. Check your CRA My Account for your exact available room — it’s listed in the RRSP/TFSA section.

For a detailed breakdown of how contribution room is calculated and tracked, see our RRSP contribution room guide.

What happens if you overcontribute?

The CRA allows a $2,000 lifetime overcontribution buffer — no penalty on the first $2,000 over your limit. Beyond that, the penalty is 1% per month on the excess until it’s corrected. A $5,000 overcontribution costs $50 per month until you withdraw or offset it. Always verify your available room before contributing.

Pension adjustments (PA)

If you have a defined benefit or defined contribution pension through your employer, your new RRSP room is reduced each year by a pension adjustment (PA) amount shown in box 52 of your T4. This is the CRA’s way of equalizing savings opportunities between pension plan members and those without one. If your PA is high, your RRSP room might be minimal or zero for that year.

The Spousal RRSP Strategy

If you and your partner have significantly different incomes, a spousal RRSP is one of the most efficient tax tools available to Canadian families — and it’s often overlooked.

Here’s how it works: the higher-earning spouse contributes to an RRSP in the lower-earning spouse’s name. The contributor gets the tax deduction at their higher marginal rate. In retirement, withdrawals are attributed to the account holder — the lower earner — who pays tax at their lower rate.

Situation: One spouse earns $130,000 (43% marginal rate in Ontario). The other earns $50,000 (29% marginal rate). The higher earner contributes $15,000 to a spousal RRSP.

Tax saved now (deduction at 43%): ~$6,512

In retirement: If both spouses have equal income (~$60,000 each), the $15,000 is eventually withdrawn at ~29%, not 43%. The couple permanently retains the difference.

The attribution rules apply if the lower-earning spouse withdraws within three years of a contribution — the income would be taxed back to the contributor. Plan the timing accordingly.

Spousal RRSPs don’t require a separate account type — your financial institution can open one alongside your regular RRSP. The contribution limit applies to the contributor’s room, not the account holder’s.

When RRSP Contributions Make Sense — and When They Don’t

- Your marginal rate is above 30%

- You expect lower income in retirement than now

- Income is temporarily elevated (bonus, severance, commission year)

- You’re income-splitting with a lower-earning spouse

- You have unused contribution room from high-income years

- The money can stay invested long-term — you won’t need it for 5+ years

- Your income is low enough that the deduction is minimal

- You don’t have an emergency fund yet

- You might need the money in the next few years

- You receive income-tested government benefits (GIS, OAS clawback)

- You expect to retire at a higher income than you earn now

- High-interest debt (credit cards, short-term loans) is outstanding

For most Canadian households, the sequence that makes sense is: stable cash flow → emergency fund → debt strategy → then registered accounts. RRSPs tend to work best when they’re part of a coordinated household financial system rather than a standalone decision made in isolation every February.

The RRSP vs. TFSA choice is a recurring decision for most Canadians. If you’re not sure which account to use first, the RRSP vs TFSA comparison breaks down the decision by income level and retirement scenario.

Where to Open Your RRSP

Two options worth considering depending on how hands-on you want to be with your investments.

Canada’s largest online brokerage. Open a self-directed RRSP and hold ETFs, stocks, or managed portfolios. No account minimum, no annual fee, and commission-free trades on Canadian and US stocks. Good for investors who want control without paying advisor fees.

Open a Wealthsimple RRSP →If you’re contributing now but not ready to invest yet, EQ Bank’s RRSP Savings Account earns competitive interest with no fees and no minimums. A good place to park contributions while deciding on your investment strategy — especially for contributions made right before the deadline.

Open an EQ Bank RRSP →For more on which account type is right for your investments, see where to put your RRSP.

The Bottom Line

RRSP contributions reduce your taxable income — but the value of that reduction depends entirely on your marginal tax rate. At $85,000 in Ontario, a $10,000 contribution saves roughly $3,400 this year and defers tax until retirement. At $130,000, the same contribution saves over $4,300. At $45,000, the case for TFSA first is legitimate.

The refund you receive isn’t a bonus — it’s overpaid tax coming back. The real advantage is the rate differential: paying tax on this income at your retirement rate instead of your working-years rate. The larger that gap, the more powerful the RRSP becomes.

Contribute in high-income years. Use spousal RRSPs if your household incomes differ significantly. And always verify your available room through CRA My Account before contributing to avoid the 1% monthly overcontribution penalty.

If you’re unsure whether RRSP or TFSA is the right move this year, the income-level decision framework in our RRSP vs TFSA guide is the clearest place to start.Frequently Asked Questions

Multiply your RRSP contribution by your combined federal and provincial marginal tax rate. If you earn $85,000 in Ontario (marginal rate ~33.89%), a $10,000 contribution saves approximately $3,389 in taxes this year. The exact amount varies by province and by whether your contribution pushes you into a lower bracket. Your Notice of Assessment or a tax calculator can give you a more precise number.

No. A tax refund means your employer withheld more tax than you owed once the RRSP deduction was applied. The government is returning money that was yours all along — it’s not a bonus or grant. The real benefit of the RRSP is tax deferral: you pay less tax now, at your working-years rate, and pay tax later at your retirement rate, which is typically lower.

Consider the TFSA first if your income is below roughly $50,000, if you expect your income to be higher in retirement than it is now, or if you might need access to the money before retirement. At lower marginal rates, the RRSP deduction is modest, and the TFSA’s tax-free withdrawals and flexibility are often more valuable. Once your income rises above $60,000–$65,000, RRSP contributions generally become more compelling.

The 2026 RRSP contribution limit is $33,810 — or 18% of your 2025 earned income, whichever is less. If your 2025 income was $100,000, you generated $18,000 in new room. Unused room from prior years carries forward indefinitely, so your total available room may be higher. Check CRA My Account for your exact figure, which is also shown on your Notice of Assessment.

Yes. Contributions made in the first 60 days of 2026 — up to the March 2, 2026 deadline — can be claimed on your 2025 tax return. You also have the option to carry the deduction forward to a future year, which makes sense if you expect a higher income (and higher tax rate) in 2026 or beyond. Most people claim immediately, but the flexibility exists.

The contribution is still made and still inside your RRSP growing tax-sheltered — but you defer claiming the deduction on your tax return. This is a legitimate strategy. If you contribute now during a lower-income year but expect significantly higher income next year, waiting to claim the deduction until next year’s return gives you a larger tax reduction. The CRA allows you to carry forward unused RRSP deductions indefinitely.

With a spousal RRSP, the higher-earning spouse (the contributor) makes contributions into an account registered in the lower-earning spouse’s name. The contributor claims the deduction at their higher marginal rate. In retirement, withdrawals are taxed as income for the account holder — the lower earner — who typically pays a lower rate. This income-splitting can save a couple thousands of dollars per year in retirement. Attribution rules apply if the account holder withdraws within three years of a contribution, which would shift the tax back to the contributor.

Yes. The CRA allows a $2,000 lifetime overcontribution buffer with no penalty. Beyond that, the penalty is 1% per month on the excess amount until it’s corrected — either by withdrawing the excess or generating new contribution room. A $5,000 overcontribution costs $50 per month. Always verify your available room in CRA My Account before contributing, especially if you’ve changed employers, received pension adjustments, or have been making regular contributions for several years.

Not sure whether RRSP or TFSA is the better move for your situation? Read RRSP vs TFSA: Which Should You Max Out? — a side-by-side comparison by income level, retirement scenario, and access needs.