Most Canadians believe this:

“If I earn more, I’ll move into a higher tax bracket and lose money.”

That belief leads to poor financial decisions—turning down overtime, hesitating to increase income, or misunderstanding how taxes actually work. It’s also wrong.

Understanding tax brackets isn’t just about taxes. It directly affects how you think about earning, saving, and making financial decisions as a family.

This article contains affiliate links. We may earn a commission if you open an account — at no cost to you. We only recommend products we’ve researched and trust.

Taxes

Taxes

In This Article

- What Are Tax Brackets in Canada?

- How Tax Brackets Actually Work

- Marginal vs. Average Tax Rate

- Example: How Tax Brackets Work in Practice

- Do You Pay More Tax If You Earn More?

- Why Your Bonus Looks Over-Taxed

- Federal and Provincial Tax

- Why Avoiding a Higher Tax Bracket Can Cost You

- How Tax Brackets Affect Real Decisions

- Where This Fits in Your Financial Plan

- The Bottom Line

- Frequently Asked Questions

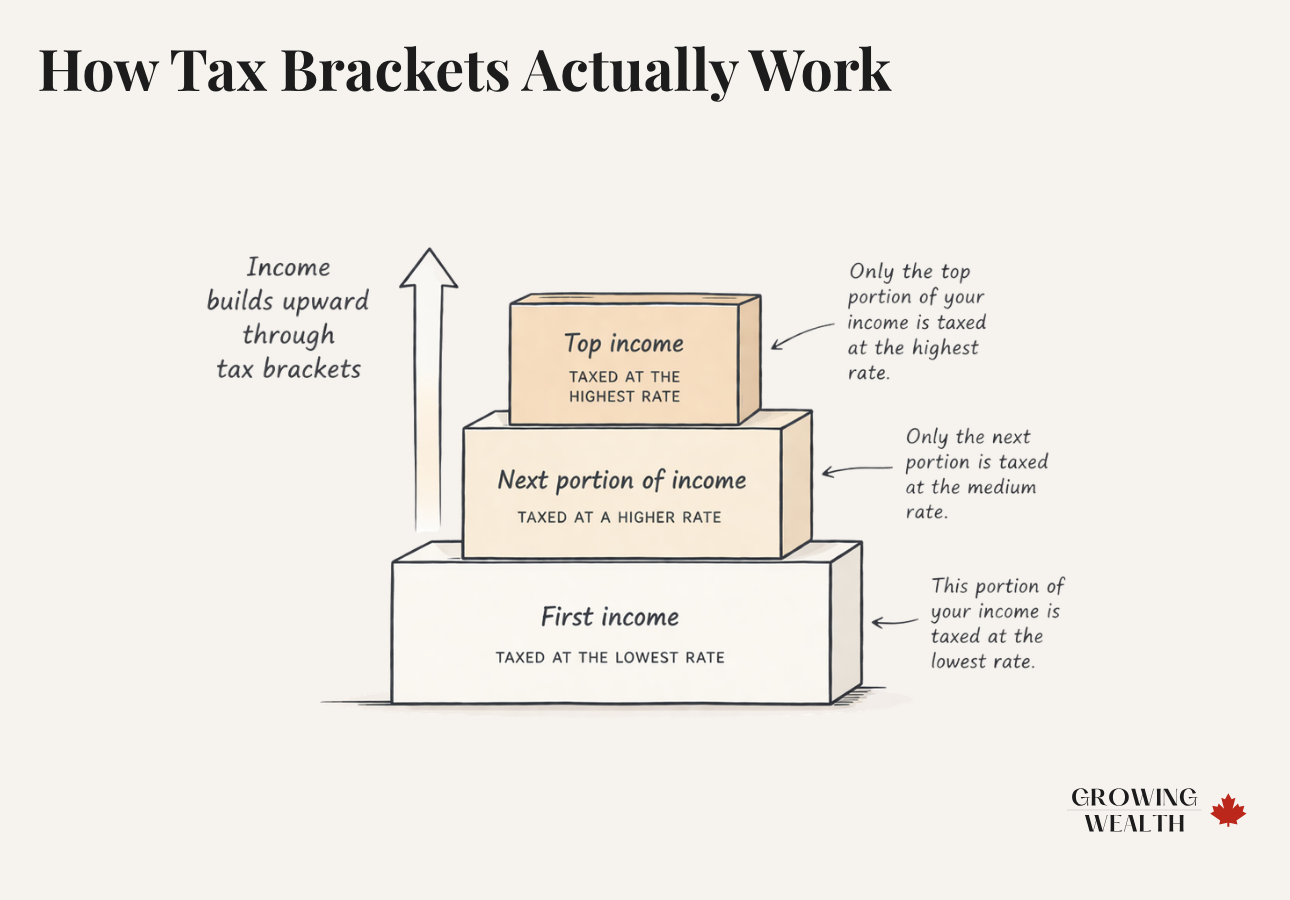

What Are Tax Brackets in Canada?

Tax brackets in Canada are ranges of income taxed at increasing rates. But the key detail most people miss is this:

Only the income within each bracket is taxed at that rate—not your entire income.

Canada uses a progressive tax system, which means your income is taxed in layers. As your income increases, each additional portion is taxed at a higher rate—but the lower portions remain taxed at lower rates.

- The first portion of your income is taxed at the lowest rate

- The next portion is taxed at a higher rate

- Only your highest income is taxed at your top rate

This layered approach is what prevents higher earnings from putting you in a worse financial position.

How Tax Brackets Actually Work

Instead of thinking of one tax rate, think of your income as a stack of layers. Each layer is taxed differently.

For example, if you earn $60,000, that income is spread across multiple tax brackets. You don’t jump into a single flat rate. Instead, each portion is taxed progressively from lowest to highest.

Once you see it this way, the idea of “jumping into a higher bracket and losing money” stops making sense.

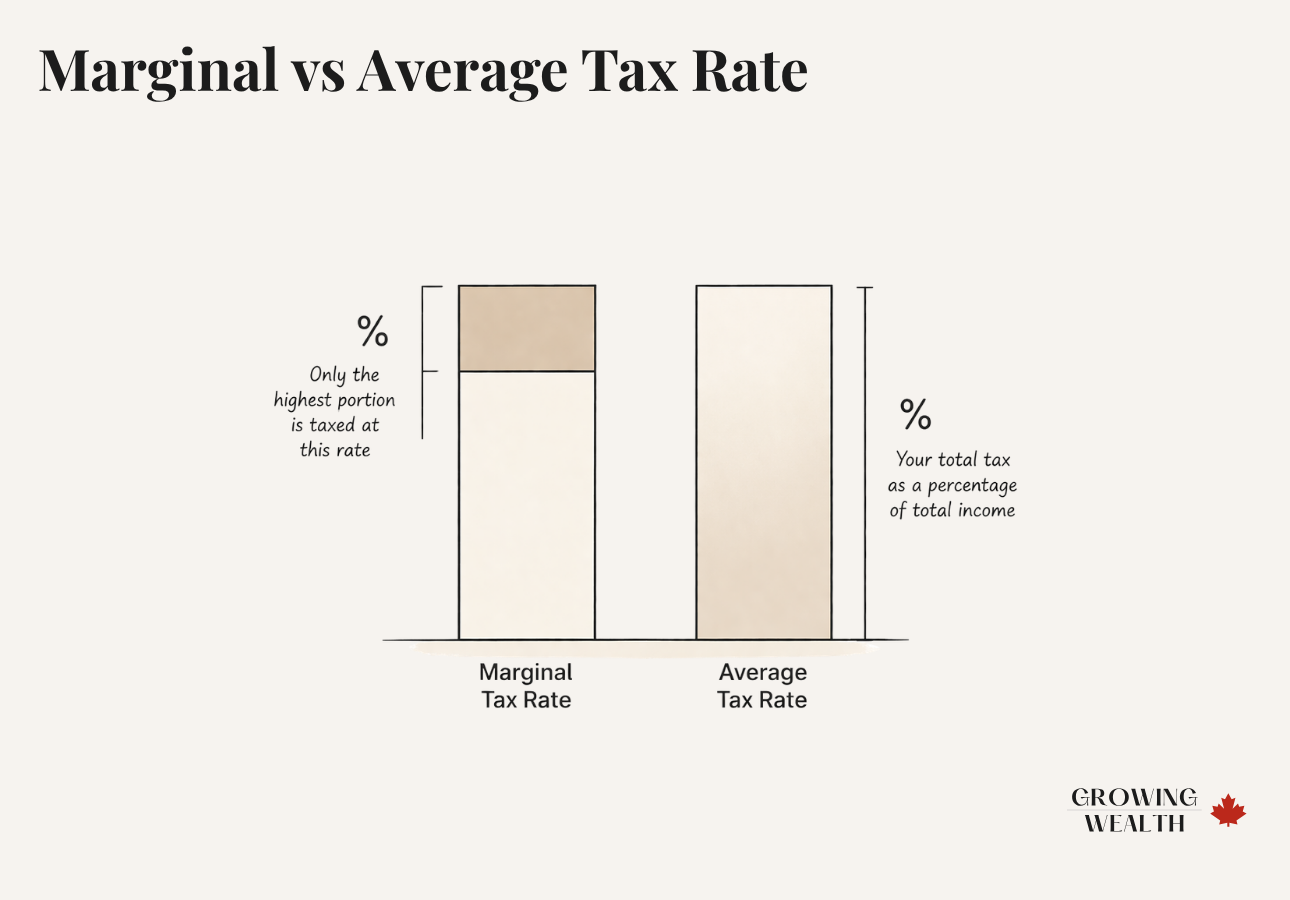

Marginal vs. Average Tax Rate (The Part Most People Miss)

This is where most misunderstandings come from—and where things start to click.

Marginal Tax Rate

Your marginal tax rate is the tax rate applied to your next dollar of income—the rate that matters when you get a raise, earn a bonus, or take on additional income.

Average Tax Rate

This represents your true overall tax burden—and it’s always lower than your marginal rate.

Why This Distinction Matters

Many people assume:

“I’m in a 30% tax bracket, so I pay 30% on everything.”

In reality, only your top income is taxed at that rate. The rest is taxed at lower levels. Understanding this removes a lot of unnecessary hesitation around earning more.

Example: How Tax Brackets Work in Practice

A simple way to see this is through real income levels.

| Income | Marginal Rate | Total Tax | Average Rate |

|---|---|---|---|

| $40,000 | ~20% | ~$6,000 | ~15% |

| $60,000 | ~30% | ~$13,000 | ~22% |

| $100,000 | ~40% | ~$30,000 | ~30% |

Even as income increases, your average tax rate rises gradually, not suddenly. This is the key reason higher earnings don’t “cancel themselves out.”

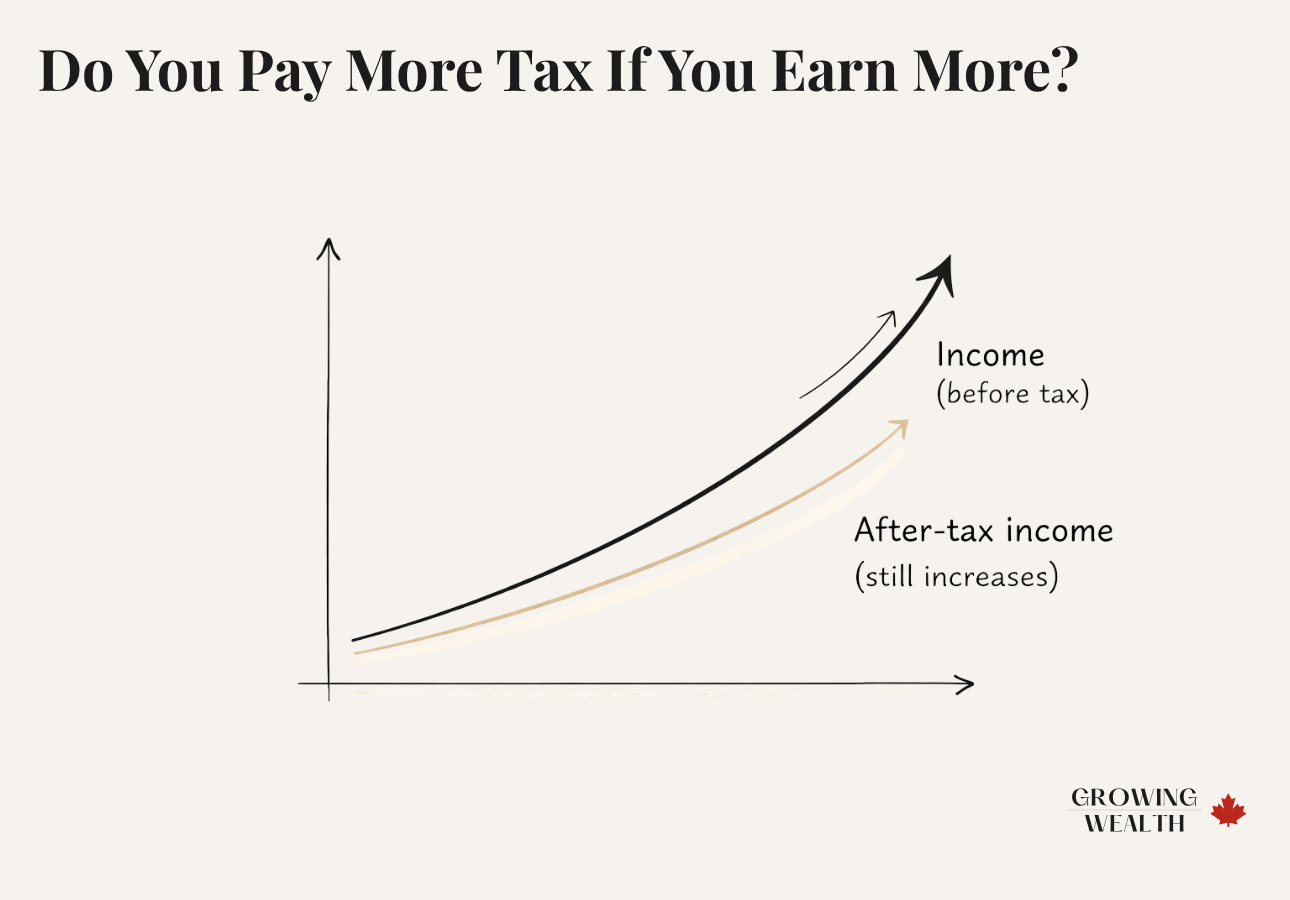

Do You Pay More Tax If You Earn More?

Yes—but only on the additional income.

Your first $60,000 is taxed exactly the same as before. Only the extra $5,000 is taxed at your higher marginal rate—and you still keep the majority of it.

There is no situation where earning more leaves you with less money after tax.

Why Your Bonus Looks Over-Taxed

Bonuses often create confusion because they appear to be taxed differently. When you receive a bonus, a larger portion may be withheld upfront. This leads many people to assume the bonus is being taxed at a higher rate.

- Your employer is estimating tax based on that larger payment

- More tax is withheld temporarily

- Your final tax amount is calculated when you file your return

Once everything is reconciled, your bonus is taxed just like your regular income.

Federal and Provincial Tax (Why Location Matters)

In Canada, your total tax rate is a combination of federal tax and provincial tax. These two layers are applied together, which is why your actual marginal rate depends on where you live.

For example, someone earning the same income in Ontario and Alberta will pay different total tax rates due to provincial differences.

You can view the current federal and provincial tax brackets directly on the Canada Revenue Agency website, which outlines both sets of rates and how they apply across provinces.

Why Avoiding a Higher Tax Bracket Can Cost You

Some Canadians turn down raises, decline overtime, or skip a side project specifically to “stay out of a higher bracket.” It feels like a smart move. It isn’t.

Turning down income to stay in a lower bracket. Because only the income inside the new bracket is taxed at the higher rate, refusing it doesn’t protect your take-home pay—it guarantees you keep less of it. A $5,000 raise you turn down is $5,000 you never collect, even though you’d have kept the majority of it after tax.

The same logic applies to overtime, bonuses, and freelance work. Every additional dollar still adds to your take-home pay. There is no income level where earning more results in a smaller paycheque.

The real cost isn’t the tax bracket. It’s the decision to leave money on the table based on a misunderstanding of how the system works.

How Tax Brackets Affect Real Decisions

Once you understand how the system works, it changes how you evaluate everyday financial decisions.

Additional income is taxed at your marginal rate, but you still keep a significant portion. The net result is always positive.

Extra income follows the same structure. It may be taxed at a higher marginal rate, but it still increases your total income.

RRSP contributions reduce your taxable income, which can shift income out of higher tax brackets and lower your overall tax. This is one of the key reasons RRSPs are more effective at higher income levels, especially when you’re comparing RRSP vs TFSA strategies in Canada.

Not all income is taxed the same way.

| Income Type | Tax Treatment |

|---|---|

| Employment income | Fully taxable |

| Capital gains | Partially taxable |

| Dividends | Taxed differently |

| Interest | Fully taxable |

As your finances grow, these differences start to matter more.

Where This Fits in Your Financial Plan

Tax brackets are just one piece of a broader financial system. They connect directly to how you build habits, structure your finances, and make long-term decisions. Building strong financial habits is what turns knowledge into results, which is why understanding the power of financial habits is just as important as understanding taxes.

At the same time, tax brackets don’t exist in isolation—they’re part of the bigger system covered in Canadian income taxes explained for families, where everything from credits to deductions fits together.

When you understand how taxes work, you stop making decisions based on incorrect assumptions, you evaluate opportunities more clearly, and you make more effective long-term choices.

The Bottom Line

Understanding how tax brackets actually work removes one of the most common (and costly) misconceptions in personal finance.

Instead of reacting based on fear, you start making decisions with clarity. You stop hesitating to take a raise or earn more income, you understand that every additional dollar increases your take-home pay, you make more informed decisions about RRSP contributions and tax planning, and you avoid limiting your income because of incorrect assumptions.

Over time, this shift changes how you approach earning, saving, and planning. Instead of trying to avoid taxes, you begin to work with the system—and that leads to better long-term financial outcomes.

Frequently Asked Questions

No. Only the income above that threshold is taxed at the higher rate.

Because of withholding. Your actual tax is calculated when you file your return.

The tax rate applied to your next dollar of income.

Your total tax paid divided by your total income.

Federal brackets are the same, but provincial rates differ.

Ready to take the next step? Read How to Reduce Your Tax Bill in Canada — specific tactics on RRSPs, TFSAs, deductions, and credits to optimize your tax strategy and keep more of what you earn.