Buying a home in Canada is one of the biggest financial decisions you’ll ever make — and it doesn’t end on closing day. There’s the purchase itself, the ongoing costs of ownership nobody warns you about, and eventually, your mortgage renewal, where thousands of dollars can be won or lost depending on how prepared you are.

This guide walks you through all three stages: buying, owning, and renewing. Whether you’re saving for your first down payment or heading into your second mortgage term, you’ll find the numbers, the steps, and the decisions that actually matter.

This article contains affiliate links. We may earn a commission if you open an account — at no cost to you. We only recommend products we’ve researched and trust.

In This Guide

Buying a Home in Canada

How Much Home Can You Actually Afford?

Before you start browsing listings, you need a realistic number — not what the bank says you can borrow, but what you can comfortably carry without sacrificing everything else in your financial life.

A good starting point is the gross debt service (GDS) ratio: your monthly housing costs (mortgage, property tax, heat) should be no more than 32% of your gross monthly income. Your total debt service (TDS) ratio — which adds in other debts like car payments and student loans — should stay below 44%.

In practice, many Canadians borrow right up to those limits. That’s not necessarily wrong, but it leaves no cushion for a leaky roof, a job change, or a rate increase at renewal.

For a deeper look at the math, check out our guide on how much house you can afford in Canada.

Real Example

A household earning $120,000/year has a gross monthly income of $10,000. At 32% GDS, they can allocate up to $3,200/month to housing costs. On a $480,000 mortgage at 5% over 25 years, the monthly payment is roughly $2,800 — leaving some room for property tax and heat within that ceiling.

If you’re still building your down payment, the FHSA and Home Buyers’ Plan used together are the most tax-efficient way to get there — a couple can access up to $200,000 in combined registered savings for a single purchase. Just remember: your savings target isn’t just the down payment — you’ll also need cash on hand for closing costs in Canada, which typically run 1.5–4% of the purchase price and can’t be rolled into your mortgage.

The Stress Test: What It Means and Why It Matters

Every mortgage applicant in Canada — whether you’re putting 5% down or 20% — must pass the federal mortgage stress test. This means you have to qualify at the higher of either:

- Your actual mortgage rate + 2%, or

- 5.25% (the regulatory floor)

If your lender offers you a 5-year fixed rate of 4.89%, you must prove you could afford payments at 6.89%. This is intentional — it creates a buffer in case rates rise at renewal.

The stress test applies to all federally regulated lenders (banks). Credit unions in some provinces operate under provincial rules and may have different requirements, though most apply similar standards.

| Purchase Price | Minimum Down Payment |

|---|---|

| Up to $500,000 | 5% |

| $500,001 – $999,999 | 5% on first $500K + 10% on remainder |

| $1,000,000+ | 20% |

If your down payment is less than 20%, you’ll pay CMHC mortgage default insurance — a premium added to your mortgage balance, ranging from 2.8% to 4% of the insured amount. On a $500,000 mortgage with 5% down, that’s up to $19,000 added to what you owe. You can find the current premium rates on the CMHC website.

Putting 20% or more down eliminates this cost entirely — which is why it’s worth the extra saving time if your budget allows.

Where to Build Your Down Payment

Two government programs exist specifically to help Canadians save for a first home.

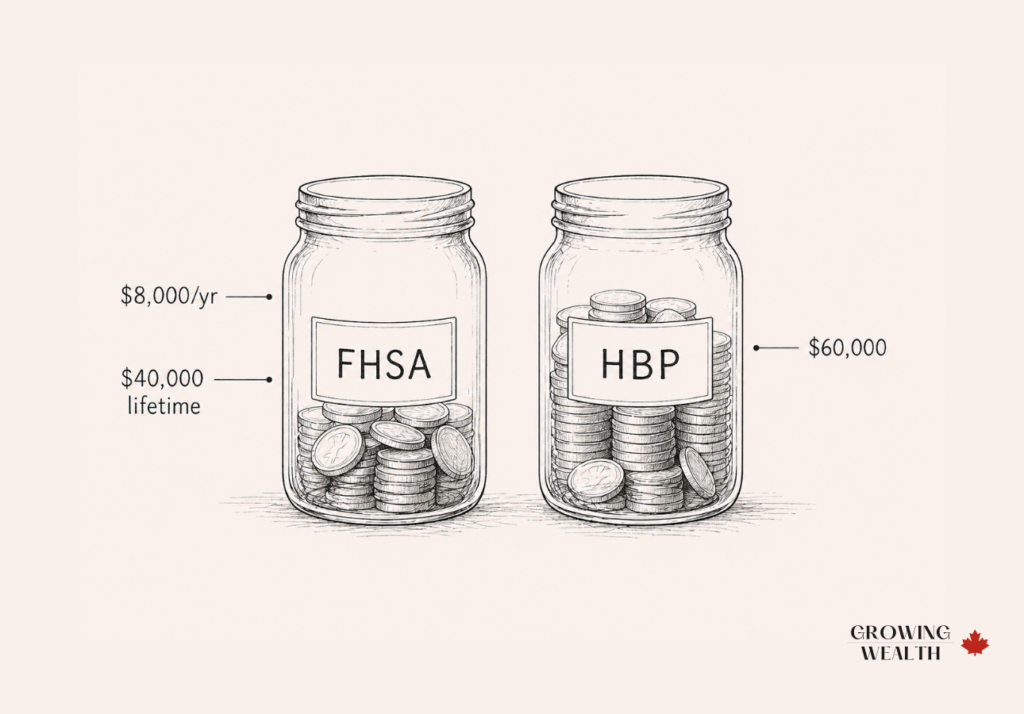

FHSA (First Home Savings Account)

The FHSA is the newer and more powerful of the two. It combines RRSP-style tax deductions with TFSA-style tax-free growth and withdrawals — as long as the money is used to buy a qualifying first home. You can contribute up to $8,000/year, with a lifetime limit of $40,000. Unused contribution room carries forward one year. For a full breakdown, see our FHSA guide.

The Home Buyers’ Plan (HBP)

The Home Buyers’ Plan lets you withdraw up to $60,000 from your RRSP tax-free to use toward a first home purchase (as of 2024). You have 15 years to repay the amount back into your RRSP, starting two years after the year of withdrawal. If you don’t repay the annual minimum, that amount is added to your taxable income for the year. The full repayment rules are outlined on the CRA’s Home Buyers’ Plan page.

The two programs can be used together. A couple could combine $80,000 from two FHSAs and $120,000 from two RRSPs via the HBP — a combined $200,000 toward a down payment, all with significant tax advantages. If you want your FHSA or RRSP savings invested while you save, Wealthsimple offers simple, low-cost portfolios with no account minimums.

Getting Pre-Approved

A mortgage pre-approval does two things: it tells you how much a lender is willing to offer you, and it locks in your interest rate for 90–120 days while you shop.

Pre-approval is not a guarantee of financing — it’s conditional on the property appraising at the purchase price and your financial situation not changing before closing. Don’t quit your job, take on new debt, or make large purchases between pre-approval and closing. For the full step-by-step process — including what documents you need and how the stress test affects your maximum — see our mortgage pre-approval guide.

To get pre-approved, you’ll typically need:

- Proof of income (T4s, NOAs, recent pay stubs)

- Proof of employment (letter from employer)

- Bank statements showing your down payment

- ID and SIN

- Consent to a credit check

Your credit score plays a significant role in whether you’re approved and at what rate. Most lenders want to see a score of 680 or higher for the best rates. If yours needs work, our guide on improving your credit score covers the steps that actually move the needle.

Closing Costs: The Expenses Most Buyers Underestimate

The down payment is the big number everyone focuses on, but closing costs can add another 1.5%–4% of the purchase price — most of it due on or before closing day.

| Cost | Typical Range |

|---|---|

| Land transfer tax (provincial) | 0.5%–2% of purchase price |

| Toronto land transfer tax (if applicable) | Additional 0.5%–2% |

| Legal fees | $1,500–$2,500 |

| Home inspection | $400–$600 |

| Title insurance | $200–$400 |

| Appraisal fee | $300–$500 |

| Home insurance (first year) | $1,200–$2,500 |

| Moving costs | $1,000–$5,000+ |

Real Example

On a $600,000 home in Ontario, land transfer tax alone is roughly $8,475. Add legal fees, inspection, and title insurance, and you’re looking at $12,000–$15,000 in closing costs on top of your down payment.

First-time buyers in Ontario, BC, and PEI may qualify for land transfer tax rebates — worth checking before you finalize your budget.

The Real Costs of Owning a Home

Property Tax

Property tax is calculated by your municipality based on the assessed value of your home and the local tax rate. In Ontario, effective property tax rates typically range from 0.5% to 1.5% of assessed value per year.

On a $600,000 home in a mid-sized Ontario city, expect to pay $4,000–$7,000/year — or $330–$580/month. In Toronto, the rate is lower but the assessed values are higher.

Many lenders will collect property tax monthly and pay it on your behalf — convenient, but check that they’re actually remitting it on time. Some homeowners prefer to manage it themselves and set aside the amount in a dedicated savings account.

Home Insurance

Mortgage lenders require home insurance as a condition of financing. Premiums vary based on the home’s size, age, location, construction type, and your coverage level. For a typical detached home in Ontario, expect $150–$250/month.

Don’t just auto-renew each year. Home insurance is a competitive market and switching providers — or simply calling to negotiate — often yields meaningful savings. Get quotes from at least two providers at each renewal.

Maintenance and Repairs

The standard rule of thumb is to budget 1%–2% of your home’s value per year for maintenance and repairs. On a $600,000 home, that’s $6,000–$12,000 annually, or $500–$1,000/month.

This sounds high until your furnace dies ($5,000–$10,000), your roof needs replacing ($8,000–$20,000), or your driveway cracks and needs repaving ($3,000–$8,000). These aren’t emergencies — they’re predictable expenses that every homeowner will face eventually. The question is whether you’ve saved for them.

Set up a separate home maintenance savings account and contribute to it monthly. An account with a strong interest rate — like EQ Bank — means your reserves are also earning while they sit.

Utilities

Depending on your home’s size, age, and heating type, utilities typically run:

| Utility | Monthly Estimate |

|---|---|

| Natural gas / heating | $100–$250 |

| Electricity | $80–$200 |

| Water | $40–$80 |

| Internet | $60–$100 |

| Total | $280–$630/month |

Older homes with poor insulation, inefficient windows, or older HVAC systems often run at the high end. This is worth investigating before you buy — ask for 12 months of utility bills and factor it into your total monthly housing cost.

Mortgage Life and Disability Insurance: What to Know Before You Sign

At or near closing, your lender will likely offer you mortgage life insurance and mortgage disability insurance. Most people sign without reading the fine print. Here’s what they don’t explain upfront.

⚠ Before You Sign

Mortgage life insurance pays off your balance if you die — but the coverage shrinks as your balance drops while premiums stay flat. You pay the same amount for less protection every year.

Term life insurance is almost always a better option. Fixed coverage, lower premiums, and the payout goes to your family — not the lender. A healthy 35-year-old can often get $500,000 in 25-year term coverage for less than lender-sold mortgage insurance on a $400,000 balance.

You don’t have to decide at closing. Get an independent quote first — you can add coverage after the fact.

Mortgage disability insurance covers your payments if you’re unable to work. The definitions of “disabled” vary significantly between providers and the exclusions can be extensive. If you have group disability coverage through work, you may already be covered.

Neither product is inherently bad — they’re just frequently oversold and overpriced compared to what’s available in the open market. Get an independent quote before you decide, and don’t let the pressure of closing day rush the decision.

The Full Monthly Picture

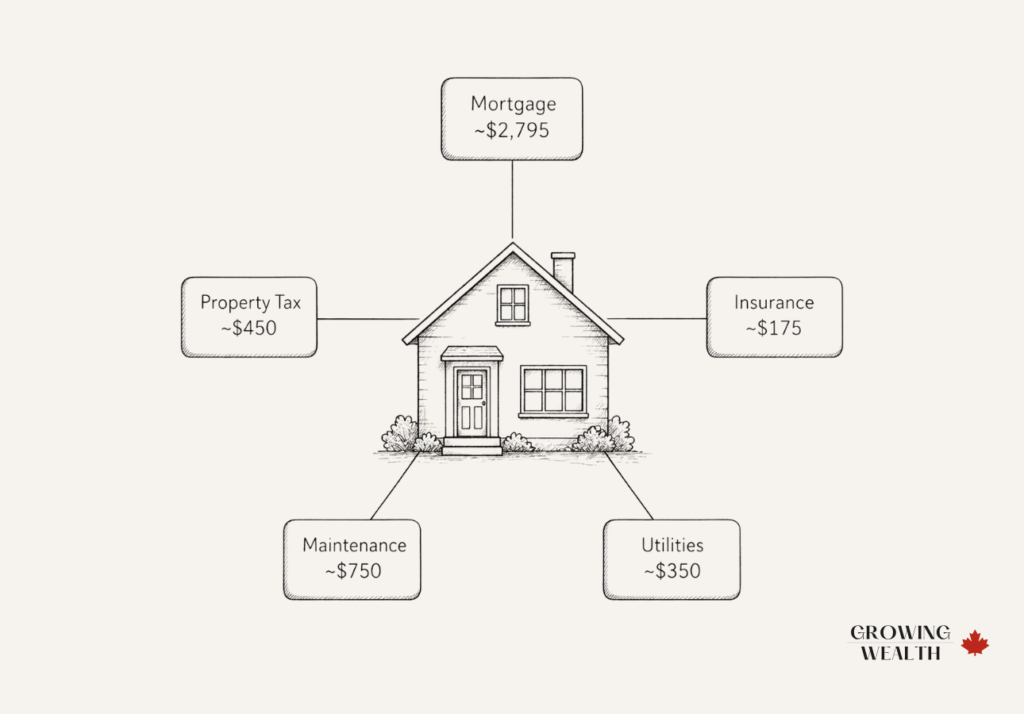

Here’s what ownership actually costs on our $600,000 example (20% down, $480,000 mortgage at 5%, 25-year amortization):

| Expense | Monthly Cost |

|---|---|

| Mortgage payment | ~$2,795 |

| Property tax | ~$450 |

| Home insurance | ~$175 |

| Maintenance reserve | ~$750 |

| Utilities | ~$350 |

| Condo fees (if applicable) | $400–$900 |

| Total (freehold) | ~$4,520/month |

The real number

~$4,520/month

The true monthly cost of owning a $600,000 home in Canada — mortgage, tax, insurance, maintenance, and utilities combined. The mortgage payment alone is $2,795.

Condo and townhouse buyers need to add monthly condo fees on top — typically $400–$900/month in most Canadian cities, and significantly higher in luxury buildings or those with aging infrastructure. Before buying a condo, review the status certificate and reserve fund study carefully. A building with a thin reserve fund is a red flag — special assessments can run $5,000–$30,000 or more.

That’s $1,700/month more than the mortgage payment alone for a freehold home — and it doesn’t include any lifestyle costs. Building this full picture before you buy is the difference between a home that stretches you and one that works within your financial life.

For a guide on building a system that makes all of this manageable, our emergency fund article is a good companion read — because owning a home doesn’t replace the need for one.

Your Mortgage Renewal

Most Canadians spend weeks shopping for their first mortgage and minutes renewing it. That’s a costly mistake — renewal is one of the highest-leverage financial moments in a homeowner’s life.

What Happens at Renewal

Your mortgage term (typically 5 years) ends before your amortization period does. At the end of each term, your lender sends a renewal offer — usually 30–45 days before the maturity date — and most borrowers simply sign it and move on.

That renewal offer is almost never the best rate your lender can offer. It’s their opening position, designed for customers who don’t negotiate.

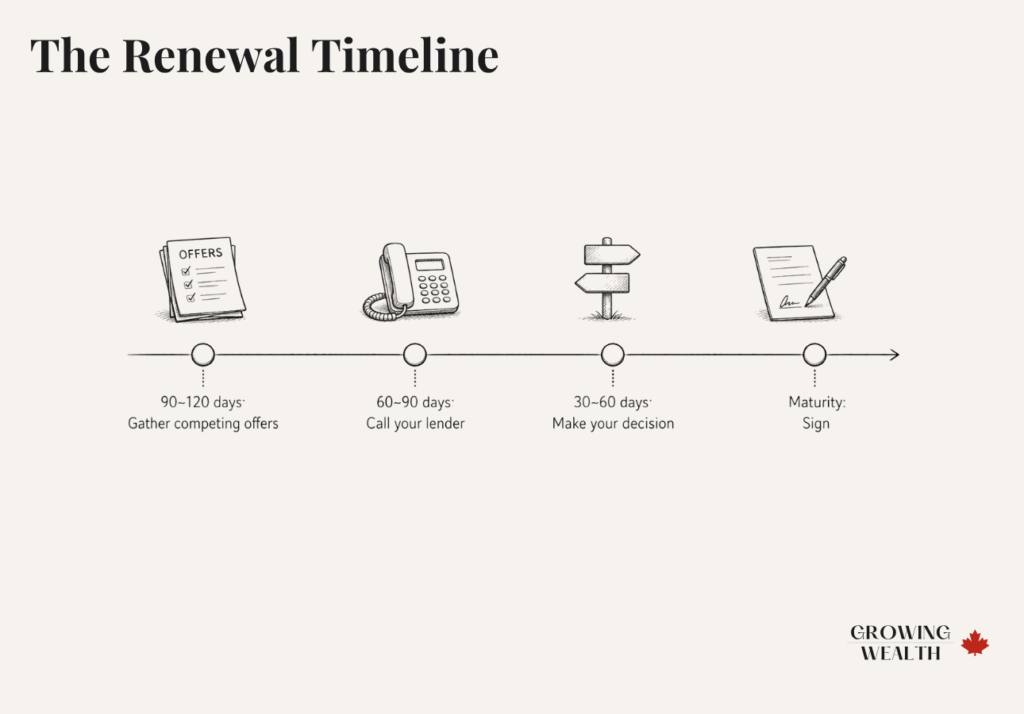

The Renewal Timeline: Start Earlier Than You Think

Most lenders allow you to begin the renewal process 120–180 days before your maturity date without penalty. Use that window.

- 90–120 days out: Start gathering competing offers. You don’t need to commit yet — you’re building leverage.

- 60–90 days out: Call your current lender and let them know you’re shopping. Ask for their best rate. Reference any competing offers you’ve received.

- 30–60 days out: Make your decision. If you’re switching lenders, a new lender will typically cover your legal and appraisal fees — removing the main friction of switching.

- At maturity: Sign and done.

Staying vs. Switching

Most Canadians renew with their existing lender. The path of least resistance is real, and switching does involve some paperwork — but it rarely requires a full re-qualification unless your financial situation has changed significantly.

Switching lenders at renewal requires a property appraisal and legal transfer, but most lenders offering competitive rates will cover these costs to earn your business.

What Negotiating Looks Like

Lender’s Opening Offer

5.44%

Competing Lender Quote

5.09%

On a $380,000 balance, that 0.35% difference saves approximately $6,650 in interest over 5 years — and drops your monthly payment by ~$75. The new lender covers appraisal and legal fees. The paperwork takes an afternoon.

That’s the renewal math most Canadians never do because they assume the process isn’t worth the effort. It almost always is.

How to Negotiate Your Renewal Rate

Lenders have more flexibility than they let on at renewal. A few things that help:

- Have competing offers in hand. Nothing moves a lender like a specific competing rate from a named competitor. Get quotes from at least two other lenders or a mortgage broker before calling.

- Ask specifically for the “loyalty rate” or “retention rate.” These are internal rates some lenders offer to customers at risk of leaving — they’re not advertised.

- Consider a mortgage broker. Brokers have access to rates from dozens of lenders and can shop your renewal on your behalf at no cost to you. They’re paid by the lender, not you.

- Don’t fixate on one term length. If you expect rates to fall, a shorter term (1–2 years) might serve you better than locking into 5 years, even if the 5-year rate looks appealing today.

Fixed vs. Variable at Renewal

At renewal, you’re making the fixed vs. variable decision again — but in a potentially different rate environment than when you first bought. Review your situation fresh:

Choose Fixed If…

- You’re at the top of your budget

- You have a single income

- A payment increase would cause real strain

- Predictability matters more than savings potential

Consider Variable If…

- You have income flexibility

- You have a solid emergency fund

- Rates are expected to fall

- You can absorb payment movement without stress

For a full breakdown of how to think through this decision, our guide on fixed vs. variable mortgages walks through both sides.

Prepayment: Accelerating Your Payoff

Renewal is also a good time to revisit your prepayment strategy. Most mortgages allow:

- Increased payment frequency (bi-weekly accelerated vs. monthly)

- Annual lump-sum payments (typically 10–20% of original principal)

- Increased regular payment amounts (typically up to 20% more)

Switching from monthly to accelerated bi-weekly payments alone can shave 2–3 years off a 25-year mortgage — without making a single extra payment in dollar terms. You’re simply paying slightly more each year by making 26 half-payments instead of 12 full ones.

If you’re weighing whether to put extra money toward the mortgage or invest it instead, we cover that decision in depth in our article on paying down your mortgage vs. investing.

Final Thoughts

Buying a home in Canada is a long game. The purchase is just the start — what comes after is decades of ownership costs, financial decisions, and eventually, renewal negotiations that most people treat as an afterthought.

The homeowners who come out ahead aren’t necessarily the ones who bought at the perfect time. They’re the ones who went in with realistic numbers, built reserves for what they couldn’t predict, and showed up to renewal ready to negotiate instead of just signing whatever landed in their inbox.

Take it one stage at a time. The rest follows.

Before you get pre-approved, make sure you understand exactly what you’re signing. Read How Mortgages Work in Canada — a plain-language breakdown of amortization, terms, payment types, and what to watch for in the fine print.

Frequently Asked Questions

At minimum, you need your down payment (5% on homes under $500,000, scaling up from there) plus closing costs (budget 1.5%–4% of the purchase price). For a $600,000 home, that means roughly $45,000–$60,000 minimum before you’re ready. Many buyers also keep 3–6 months of expenses in an emergency fund separate from these costs — homeownership comes with unpredictable expenses.

Most federally regulated lenders require a minimum credit score of 600–620 for an insured mortgage (under 20% down), but you’ll get significantly better rates with a score of 680 or higher. The higher your score, the more negotiating power you have. Check your score before you start the pre-approval process — if it needs work, even 6–12 months of focused improvement can make a meaningful difference.

Yes. These two programs can be combined for the same home purchase. A first-time buyer could withdraw from their FHSA (up to their available contribution room, lifetime max $40,000) and also withdraw up to $60,000 from their RRSP through the HBP. Two qualifying buyers purchasing together could combine up to $200,000 from both programs.

From accepted offer to closing, the typical timeline is 30–90 days. But realistically, the buying process — saving, getting pre-approved, actively searching, and making offers — takes most buyers 6–24 months. The more competitive the market, the longer the search phase tends to be.

CMHC mortgage default insurance is required when your down payment is less than 20% of the purchase price. It protects the lender (not you) if you default on the loan. The premium ranges from 2.8% to 4% of your insured mortgage amount and is added to your mortgage balance. The only way to avoid it is to put 20% or more down, or to purchase through a lender not subject to federal mortgage insurance rules (such as some credit unions).

Breaking your mortgage early — to sell the home, refinance, or lock in a lower rate — typically triggers a prepayment penalty. For fixed-rate mortgages, this is usually the greater of three months’ interest or the interest rate differential (IRD), which can run into the tens of thousands of dollars depending on how much rates have moved. Variable-rate mortgages typically charge only three months’ interest, which is lower and more predictable. Always calculate the penalty before deciding to break early.

Mortgage brokers have access to rates from multiple lenders — including some rates not available directly to consumers — and are paid by the lender, not you. They’re particularly valuable if you have a complex financial situation (self-employed, variable income, non-traditional credit history) or if you want someone to shop your renewal without doing it yourself. Going directly to a bank can work if you have a strong relationship and know you’re getting competitive rates — but always get at least one external quote for comparison.

More than most people budget for. Property tax, home insurance, utilities, and maintenance together often add $1,500–$2,500/month on top of the mortgage payment. Using our $600,000 example, the total monthly cost of ownership is closer to $4,500 than the $2,800 mortgage payment alone. Building this full picture before you buy — and maintaining a dedicated home maintenance reserve — is one of the most important financial habits a homeowner can develop.

Affiliate Disclosure: GrowingWealth.ca is supported by readers. Some links in this article are affiliate links — we may earn a small commission if you open an account, at no extra cost to you. We only recommend products we trust and believe provide genuine value to Canadians. Our reviews and comparisons are always independent and objective.