Budgeting sounds simple in theory. Track what comes in, track what goes out, spend less than you earn. But if it were that simple, most Canadian families wouldn’t feel like they’re always one unexpected bill away from stress.

The reality is that budgeting isn’t just a math problem — it’s a system. And the right system for a family of four in Winnipeg looks very different from a spreadsheet tip you found on an American finance blog.

This guide walks you through exactly how to build a budget that actually works for your family in Canada — including the most popular budgeting methods, a real dollar breakdown using a Canadian household income, and the best free tools to help you stick with it.

This article contains affiliate links. We may earn a commission if you sign up — at no cost to you. We only recommend products we’ve researched and trust.

Budgeting

Budgeting

In This Article

- Why Most Budgets Fail (And How to Avoid It)

- Step 1: Know Your Real Monthly Income

- Step 2: Track Every Dollar You’re Currently Spending

- Step 3: Choose a Budgeting Method That Fits Your Family

- Step 4: Build Your Budget — A Real Canadian Example

- Step 5: Set Up Your Savings Buckets

- Step 6: Automate What You Can

- Step 7: Review and Adjust Monthly

- Best Free Budgeting Tools for Canadians

- Common Budgeting Mistakes Canadian Families Make

- How to Track Your Budget Progress

- Budgeting as a Family

- When to Adjust Your Budget

- Frequently Asked Questions

Why Most Budgets Fail (And How to Avoid It)

Before diving into the how-to, it’s worth understanding why budgets fall apart. Most people fail at budgeting not because they lack discipline, but because they’re trying to use willpower to override a system that isn’t set up to support them.

James Clear, author of Atomic Habits, makes a point that applies directly to personal finance: you don’t rise to the level of your goals, you fall to the level of your systems. A budget that depends on you making 30 correct decisions every month will eventually fail. A budget built into your environment — automatic transfers, clear categories, a simple weekly check-in — will outlast any amount of motivation.

A zero-based budget requires detailed tracking every single day. That works brilliantly for someone with a variable income or a tendency to overspend — but it’s exhausting for a busy parent who just needs a simple framework that runs in the background.

Conversely, someone who thinks the 50/30/20 rule is enough might find they’ve blown through their “wants” category by the 10th of the month without realizing it.

The goal of this guide is to help you find the method that fits your family — and then build the environment around it so it runs with as little friction as possible.

Step 1: Know Your Real Monthly Income

Your budget starts with your take-home pay — not your salary. Canadians often confuse gross income with what actually lands in their bank account.

Your take-home pay is your gross income minus:

- Federal and provincial income tax

- CPP contributions (Canada Pension Plan)

- EI premiums (Employment Insurance)

- Any workplace deductions (benefits, RRSP contributions, union dues)

If you have a variable income (freelance, commission, seasonal work), use your lowest average month from the past 12 months as your baseline. It’s always better to budget conservatively and have extra than to overshoot and come up short.

Pull up your last three pay stubs and calculate your actual average monthly take-home. Write that number down — it’s your starting point for everything that follows.

Step 2: Track Every Dollar You’re Currently Spending

Before you build a new budget, you need to know where your money is actually going — not where you think it’s going.

Most families are surprised by this step. The $6 coffees, the subscription services you forgot you signed up for, the grocery runs that somehow hit $300 — it adds up quickly.

Download your last two to three months of bank and credit card statements.

Housing, groceries, transportation, subscriptions, dining out, kids’ activities — sort every line item into a bucket.

Add up each category across all three months, then divide by three. That’s your real baseline — not your ideal, your actual.

You don’t need to do this manually forever — this is a one-time diagnostic. Once you see where your money goes, you can build a realistic budget around your actual life rather than an idealized version of it.

Step 3: Choose a Budgeting Method That Fits Your Family

There’s no single best budgeting method. The best one is the one you’ll actually use. Here’s an honest breakdown of the most popular options for Canadian families.

Divide after-tax income into three buckets: 50% needs, 30% wants, 20% savings and debt. Simple and flexible — no tracking every dollar.

Canadian reality check: In Toronto or Vancouver, housing alone can eat 40–50% of take-home. Adjust to 60/20/20 if needed.

Best for: Simple, low-maintenance budgetingEvery dollar is assigned a job. Income minus all allocations equals zero — not because you’ve spent everything, but because every dollar has a purpose.

Best for: Families paying off debt or who tend to overspend without a hard structure.

Best for: Total control over every dollarBefore you pay any bill or spend anything, automatically move a set amount to savings. Then live on whatever remains.

How to implement: Set up an automatic transfer to your TFSA or savings account on payday — treat it like a non-negotiable bill.

Best for: Families who struggle to saveCash (or digital equivalents) is divided into envelopes for each spending category. When the envelope is empty, spending stops.

Modern version: Apps like YNAB or GoodBudget replicate this digitally — no need to carry cash.

Best for: Hard stops on overspendingWhich Method Should You Choose?

| You want… | Best method |

|---|---|

| Simple and low-maintenance | 50/30/20 |

| Total control over every dollar | Zero-based budgeting |

| To automate savings without thinking | Pay-yourself-first |

| A hard stop on overspending | Envelope budgeting |

| A combination approach | Pay-yourself-first + 50/30/20 |

Many families end up combining methods — automating savings first, then using a loose 50/30/20 framework for everything else. Start simple. You can always add complexity later.

The method matters less than the identity you build around it. Families who stick to a budget long-term aren’t those with the most willpower — they’re the ones who’ve started to think of themselves as people who manage money intentionally. The method is just the vehicle. The habit is what drives.

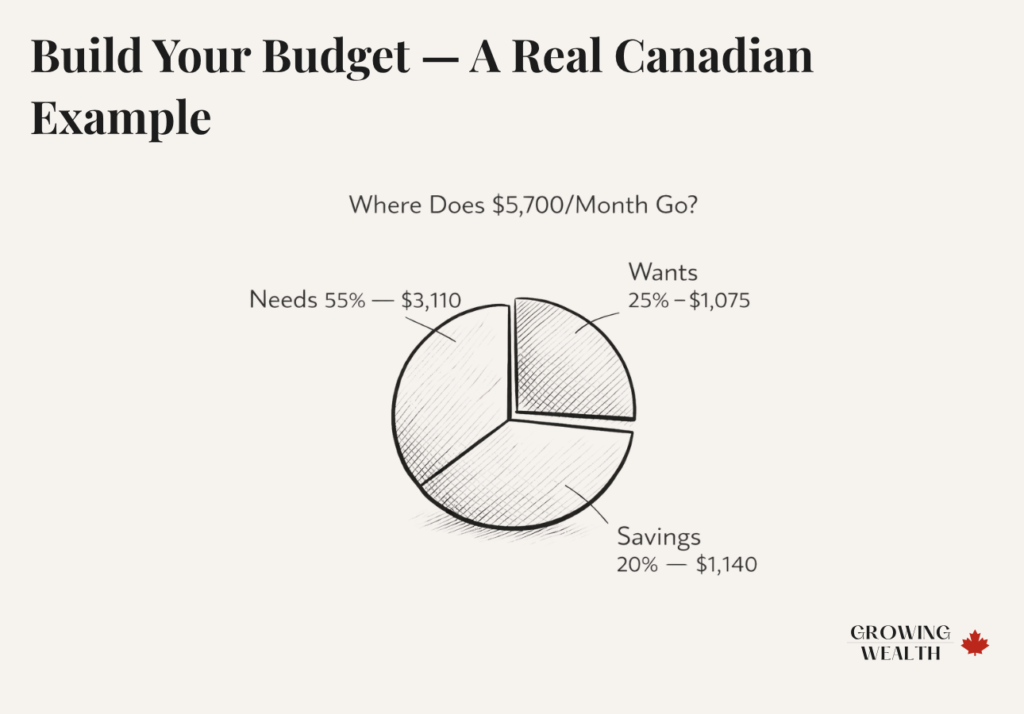

Step 4: Build Your Budget — A Real Canadian Example

Let’s put this into practice with a real-life scenario: two adults, two kids, household income of $90,000/year gross, living in a mid-sized Canadian city (not Toronto or Vancouver). Take-home pay: approximately $5,700/month. They’re using a modified 50/30/20 approach.

Fixed Needs (~55% / ~$3,110)

| Expense | Monthly Amount |

|---|---|

| Rent / mortgage | $1,650 |

| Car payment + insurance | $480 |

| Groceries (family of 4) | $700 |

| Utilities (hydro, gas, internet) | $280 |

| Total | $3,110 |

Their needs land at 55% rather than 50% — common for families. They’ve adjusted their wants category accordingly.

Flexible Wants (~19% / ~$1,075)

| Expense | Monthly Amount |

|---|---|

| Dining out / takeout | $250 |

| Kids’ activities (one sport each) | $300 |

| Subscriptions (streaming, apps) | $75 |

| Personal spending / clothing | $200 |

| Date nights / entertainment | $150 |

| Miscellaneous | $100 |

| Total | $1,075 |

Savings + Debt Repayment (~20% / $1,140)

| Destination | Monthly Amount |

|---|---|

| TFSA (emergency fund top-up) | $300 |

| RRSP contributions | $400 |

| RESP (kids’ education) | $200 |

| Extra mortgage payment | $240 |

| Total | $1,140 |

Monthly total: $5,325 — leaving ~$375 as a buffer for unexpected expenses. Rather than spending that buffer, this family sweeps it into their emergency fund at month-end.

This isn’t a perfect budget. It’s a realistic one. And realistic beats perfect every time.

Step 5: Set Up Your Savings Buckets

A budget isn’t just about controlling spending — it’s about building the financial foundation your family needs. That means having the right accounts in place.

Before anything else, build three to six months of essential expenses in a separate, accessible account. For the family in our example, that’s roughly $15,000–$18,000. Start with a goal of $1,000, then build from there. A high-interest savings account is the right home for this money — it earns interest while staying accessible. Our emergency fund guide walks through exactly how much you need.

Once your emergency fund is in place, your Tax-Free Savings Account is one of the most flexible tools available to Canadian families. Growth and withdrawals are tax-free, and unused contribution room carries forward each year. It can hold everything from a savings account to ETFs.

Contributions reduce your taxable income in the year you make them — which means a real tax refund for most families. Ideal if your income is above $50,000 and you expect to be in a lower tax bracket in retirement. Learn more in our RRSP guide.

If you have kids, the Registered Education Savings Plan comes with a 20% government grant on the first $2,500 contributed per year — up to $500/year in free money per child. One of the best financial moves a Canadian family can make.

For a deeper look at how to structure your money across all of these accounts, our family finance system guide walks through how to prioritize each bucket based on your family’s situation.

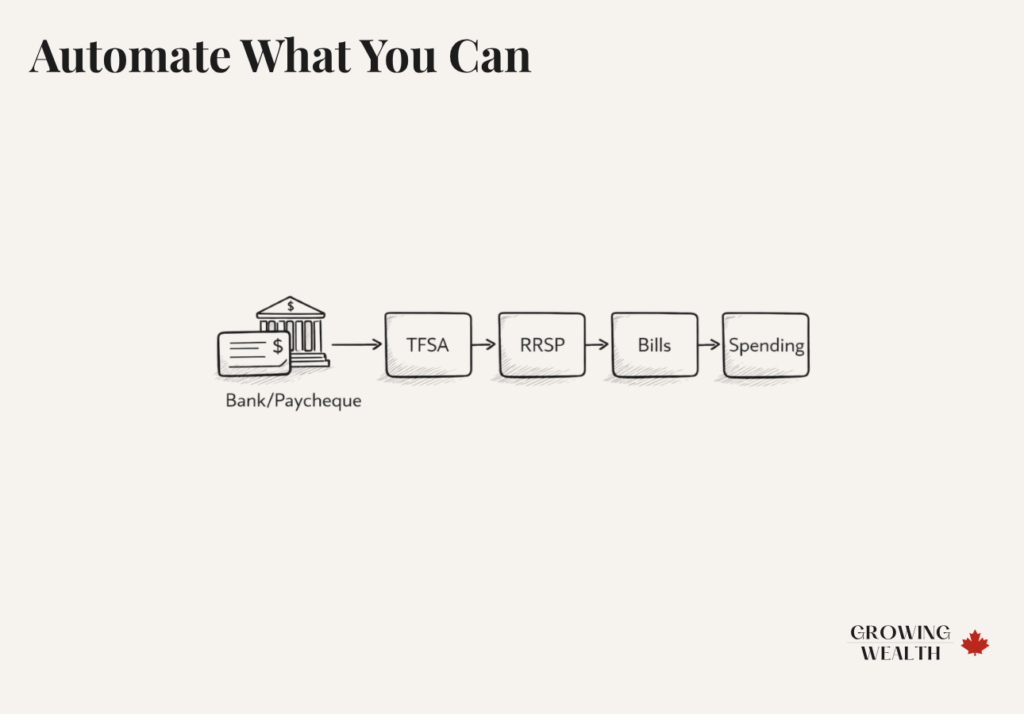

Step 6: Automate What You Can

The single biggest predictor of budgeting success isn’t willpower — it’s automation. This is environment design in practice: when you remove the decision, you remove the opportunity to make the wrong one.

Every transfer you have to make manually is a transfer that might not happen. Set up automatic transfers for:

Move money to your TFSA, RRSP, or emergency fund the same day your paycheque arrives — before you have a chance to spend it.

Set minimum payments (and ideally more) to auto-pay each month. Never miss a payment, never pay a late fee.

Hydro, insurance, phone, and internet should all be on auto-pay. These numbers don’t change much — there’s no reason to spend mental energy on them every month.

When savings move automatically, you’re not relying on discipline — you’re relying on a system. Systems beat motivation every time. Once your savings and fixed expenses are automated, you only need to actively manage your discretionary spending.

Our guide to automating your family finances covers exactly how to set this up step by step, including which accounts to link and in what order.

Step 7: Review and Adjust Monthly

A budget is not a set-it-and-forget-it document. Life changes — kids switch activities, insurance goes up, you get a raise, or a car breaks down. Your budget needs to reflect your real life, not a snapshot from three months ago.

Build a monthly budget date into your routine. Even 20–30 minutes once a month is enough. Review:

- Did you stay within each category?

- Were there any surprises you need to plan for next month?

- Did anything change — income, expenses, goals?

Make adjustments as needed. Don’t treat a category overage as a failure — treat it as data. The goal is a budget that gets more accurate and effortless over time, not one that makes you feel guilty.

You’re not trying to nail it perfectly in month one. You’re trying to get 1% better each month — slightly more accurate categories, slightly fewer surprises, slightly more saved. Small improvements compound. A budget you’ve been refining for six months will feel almost effortless compared to the first version you built.

For a deeper look at how small financial habits build into lasting wealth — and the psychology behind why they stick — our article on the power of financial habits is worth reading alongside this one.

Best Free Budgeting Tools for Canadians

You don’t need to spend money to budget effectively. Here are the best free and low-cost options available to Canadian families.

| Tool | Cost | Best For |

|---|---|---|

| YNAB | ~$109 CAD/year (34-day free trial) | Zero-based budgeters who want a powerful, dedicated tool |

| Monarch Money | ~$99 CAD/year | Couples and families who want shared finances, net worth tracking, and goal-setting in one place |

| Credit Karma | Free | Basic transaction tracking and net worth monitoring (replaced Mint in Canada) |

| FCAC Budget Planner | Free | Families who want a no-frills, government-backed tool with no account required |

| Google Sheets / Excel | Free | Families who want complete control without connecting bank accounts to a third party |

| Your Bank’s App | Free | Zero setup — TD MySpend, RBC NOMI, Scotiabank’s budget feature are built right in |

The Financial Consumer Agency of Canada’s free budget planner is straightforward, private, and Canadian-specific — a solid starting point if you want to avoid connecting your banking to a third-party app.

The best budgeting app for Canadian couples and families — shared financial dashboards, reliable Canadian bank connections, net worth tracking, and goal-setting in one clean interface. 50% off your first year with our link.

Try Monarch Money — 50% off →Common Budgeting Mistakes Canadian Families Make

Even with the best intentions, these are the most common places budgets break down.

Property tax, car registration, back-to-school shopping, holiday gifts — these aren’t monthly, but they’re predictable. Add them up annually, divide by 12, and set that amount aside each month so you’re never caught off guard.

Grocery inflation in Canada has been significant. A realistic grocery budget for a family of four in 2025 is $800–$1,000/month depending on your city and dietary needs. Budget conservatively here.

Budgets that have no room for enjoyment don’t last. Give each adult a small personal spending allowance — no questions asked, no guilt. This is the pressure valve that keeps the system sustainable.

A budget isn’t a restriction — it’s a plan. The money you don’t spend on things you don’t care about becomes money you can spend on things you do.

Everybody blows their budget sometimes. The families who build real financial health are the ones who reset on the 1st and try again — not the ones who had a perfect record.

Budgeting Checklist for Canadians

A printable, fillable 7-step guide you can use every single month. No spreadsheet required.

Download it free →The Bottom Line

Budgeting isn’t about being perfect. It’s about being intentional — knowing where your money goes and making sure it’s going toward the things that matter most to your family.

Start simple. Pick one method. Track your spending for one month. Then adjust. The families who build real financial security aren’t the ones with the fanciest spreadsheets — they’re the ones who built a system, stuck with it through the messy months, and kept going.

Ready to take the next step? Our family finance system guide shows you how to structure your entire financial life — not just your budget — into a clear, manageable system that runs in the background of your busy life.How to Track Your Budget Progress

Knowing your budget is one thing — staying accountable to it is another. Building a simple tracking rhythm is what separates families who budget successfully for years from those who try it for three weeks and quietly give up.

- Open your banking app or budgeting tool

- Review transactions from the past seven days

- Flag anything that feels off or that you want to revisit

- Check your remaining balance in discretionary categories

Friday evening or Sunday morning works well. The goal isn’t a deep review — it’s staying connected so nothing surprises you at month-end.

- Celebrate a win — savings goal hit, balance paid off? Acknowledge it

- Review last month — what did you spend? Where did you go over or under?

- Make one or two adjustments — groceries always $100 over? Fix the category, not yourself

- Set next month’s priorities — birthday coming? Car service due? Plan now, not then

Treat it as a date, not a chore. Short, structured, and forward-focused.

- Is your net worth growing?

- Are savings on track toward your annual goals?

- Do your categories still reflect your actual life?

- Are there subscriptions or recurring costs worth cutting?

- Are TFSA and RRSP contributions on pace for the year?

This is where you catch drift before it becomes damage. Four times a year is enough.

Budgeting as a Family: Getting Everyone Involved

A budget works best when everyone in the household is aligned — not just aware of it, but genuinely bought in. That looks different for couples than it does for kids.

For Couples

Have the money conversation before you need to. The worst time to discuss financial priorities is when you’re already stressed about a specific bill. Regular, low-stakes check-ins prevent blow-ups.

- Weekly spending check-ins

- Categorizing transactions

- Monitoring discretionary categories

- Flagging budget overages

- RRSP and TFSA contributions

- Monthly savings transfers

- Annual tax planning

- Net worth tracking

For Kids

Involving children in age-appropriate money conversations is one of the most valuable things you can do for their financial future. You don’t need to share every stressful detail — but normalizing money talks early creates financially confident adults.

Introduce the idea that money is finite and choices have to be made. “We have a set amount for treats this week — once it’s gone, it’s gone.” A small coin jar for their own money teaches cause and effect without any lectures.

Give them a small weekly or monthly amount and let them manage it. Include them in decisions about family activities — “we have $80 budgeted for fun this weekend, what should we do?” This builds real decision-making, not just observation.

Involve them in saving toward something they actually want — a trip, a phone, a car. Show them how to set a goal, track progress, and make trade-offs. If they’re working, help them open a TFSA. The habits they build now are the ones they’ll carry into adulthood.

When to Adjust Your Budget

Your budget should be a living document. Here are the most common triggers for a budget update:

| Trigger | What to Do |

|---|---|

| Income change | Full budget reset — a raise, job loss, or return from parental leave all change your baseline. |

| New major expense | Recalculate fixed costs — a new mortgage, baby, or car purchase changes your landscape significantly. |

| Debt paid off | Redirect that payment immediately to savings, another debt, or a goal — don’t let it disappear into lifestyle. |

| Goals achieved | Move the allocation — a fully funded emergency fund should redirect to RRSP or RESP, not sit idle. |

| Life stage shift | Plan ahead — kids leaving for university, approaching retirement, or buying a home all require a budget overhaul. |

If a home purchase is on your horizon, our guide to buying a home in Canada shows the full monthly cost picture — mortgage, property tax, insurance, maintenance — so you can plan your budget around reality, not just the mortgage payment.

Want to turn what you’ve just learned into lasting results? Read A Simple Family Finance System for Canadians — a complete framework for structuring your savings, bills, and investments so your whole financial life runs on autopilot.

Frequently Asked Questions

A realistic grocery budget for a family of four in Canada ranges from $800–$1,100/month depending on your city, dietary needs, and how much you cook from scratch. Statistics Canada’s most recent food price data shows grocery costs rose significantly in 2022–2024, so older benchmarks may be too low. Budget conservatively and adjust based on your actual spending.

The 50/30/20 rule is the easiest starting point because it requires minimal tracking and gives you a clear framework immediately. Once you’re comfortable with that, you can layer in more detail if needed. Don’t try to implement a zero-based budget on day one — the friction will kill the habit.

Monthly budgeting aligns with most Canadian bills and pay cycles. If you’re paid bi-weekly, some families find it easier to budget per paycheque instead. Choose whatever feels most natural to your income rhythm. The weekly check-in is separate — that’s just five minutes to stay connected to your numbers, not a full reset.

Base your budget on your lowest average monthly income from the past 12 months. In higher-income months, direct the extra to savings or debt repayment rather than lifestyle inflation. This approach keeps your baseline conservative and turns good months into progress rather than increased spending.

Build a small emergency fund (at least $1,000) first, then focus on high-interest debt — credit cards and high-rate personal loans. Once high-interest debt is gone, balance saving and lower-interest debt repayment based on interest rates and your financial goals. The $1,000 buffer prevents you from going back into debt the moment something unexpected happens.

Frame it as a shared plan for your goals — a vacation, a home, less financial stress — rather than a set of restrictions. Budget meetings work better when they’re short, regular, and focused on progress rather than what went wrong. Starting with a simple method like 50/30/20 also lowers resistance because it doesn’t feel punishing.

Not always. In Toronto or Vancouver, housing alone can consume 40–50% of take-home pay. In those cases, adjusting to a 60/20/20 or even 65/15/20 split is more realistic. The percentages are a starting point, not a rigid rule — what matters is that you’re saving intentionally and not spending more than you earn.

Most families notice a meaningful difference — more savings, less financial anxiety — within two to three months of consistently following a budget. The first month is usually the hardest because you’re still calibrating your categories. By month three, the system starts to feel automatic rather than effortful.