BANKING

BANKING

This article contains affiliate links. We may earn a commission if you open an account — at no cost to you. We only recommend products we’ve researched and trust.

Most articles about joint bank accounts give you a ranked list and call it a day. That’s not actually useful, because the best joint account depends entirely on what you’re using it for. A joint account for paying the mortgage and groceries needs completely different features than one for building shared savings. Pick the wrong type and you’ll either leave interest on the table or end up with an account that can’t handle day-to-day transactions.

The good news: Canada’s digital banking options for joint accounts are genuinely strong in 2026 — no monthly fees, real interest rates, and full online setup. This guide gives you a clear framework for which account does which job, then covers the specific accounts worth opening.

In This Article

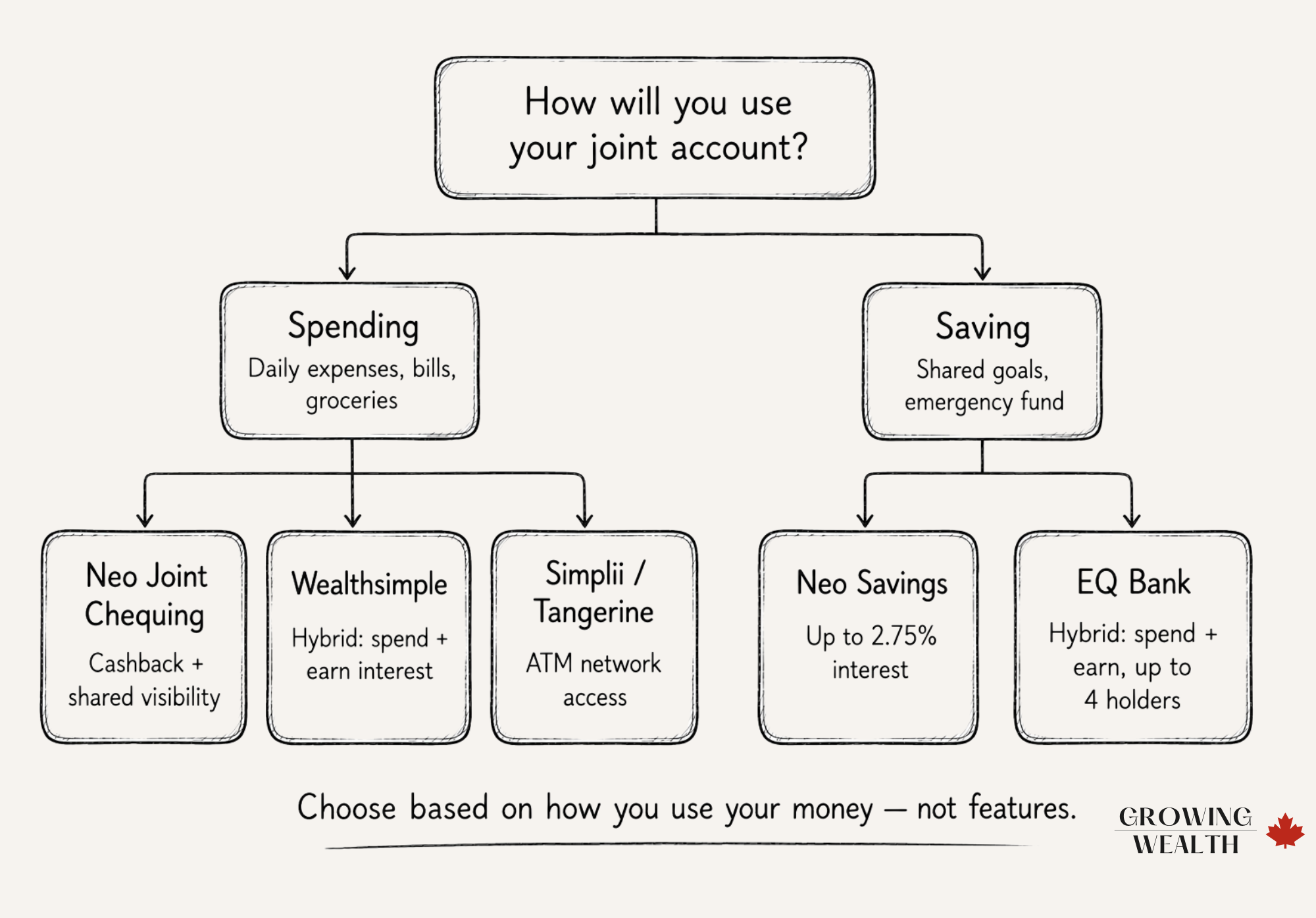

Start here: spending or saving?

Before comparing accounts, answer this question: what is this joint account actually for? The answer determines everything else.

| If you need to… | You need a… | Best option |

|---|---|---|

| Pay shared bills, groceries, mortgage, subscriptions | Joint chequing account — transactional, with debit card access | Neo Joint Chequing or Wealthsimple |

| Earn meaningful interest on shared savings (vacation fund, emergency fund, home reno) | Joint savings account — interest-focused, not for daily transactions | Neo Joint Savings or EQ Bank Joint |

| Do both — earn interest AND make transactions from one account | Joint hybrid account — earns interest like a savings, transacts like chequing | EQ Bank Joint or Wealthsimple |

| Need physical ATM access as a priority | Joint chequing with bank network | Simplii (CIBC ATMs) or Tangerine (Scotiabank ATMs) |

Most families benefit from two joint accounts: one for spending, one for saving — the same logic that applies to choosing any of the best bank accounts in Canada. Neo makes this easy — their joint chequing and joint savings accounts work as a pair. EQ Bank and Wealthsimple both offer a single hybrid account that handles both jobs, which is simpler to manage.

How joint accounts work in Canada

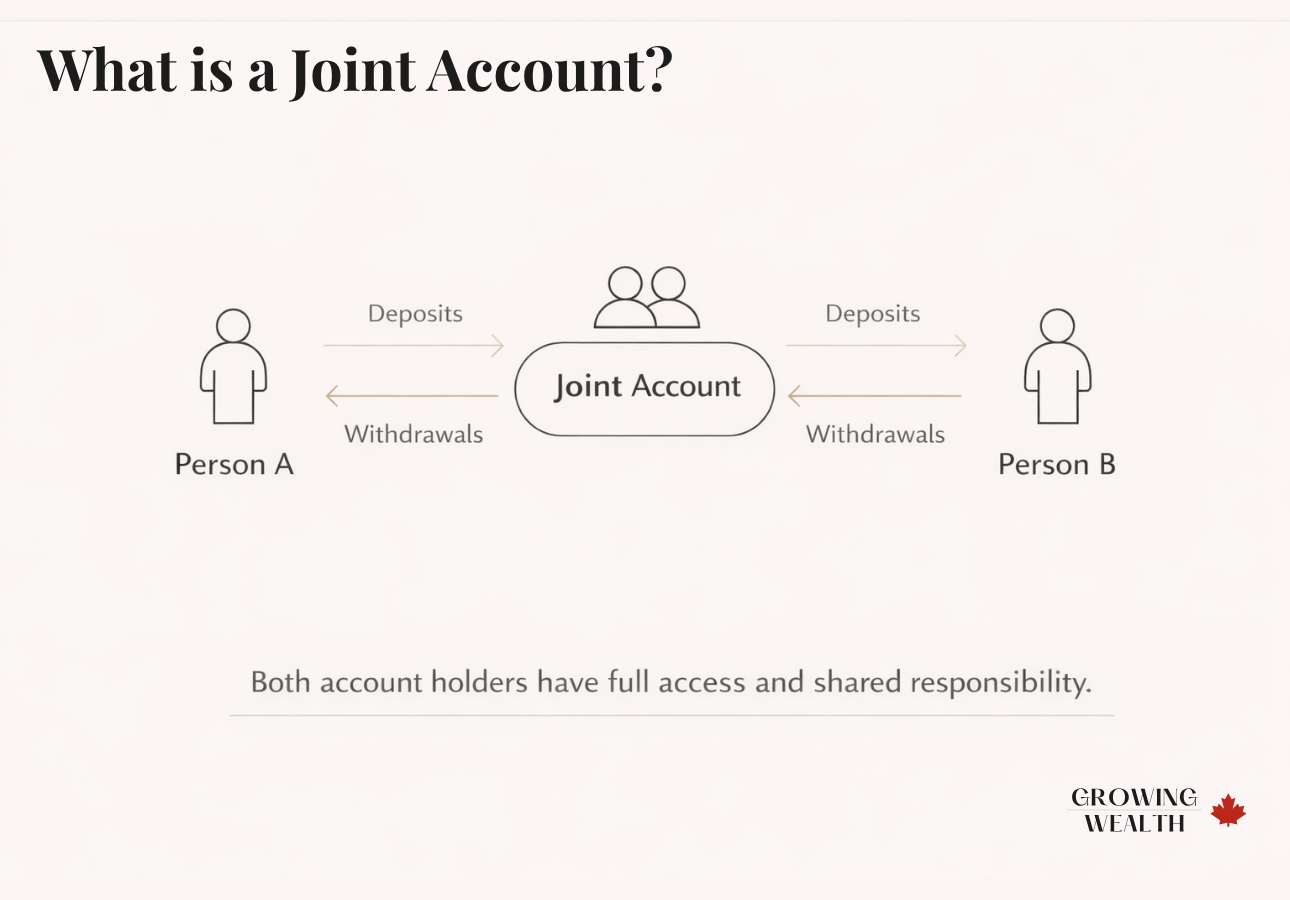

A joint bank account is held in two names, with both owners having equal access and equal responsibility. Either person can deposit, withdraw, pay bills, or send e-Transfers without the other’s approval. There is no internal safeguard — if one person empties the account, the other has no automatic recourse.

That equal access is both the strength and the risk. It works well when both people are financially aligned and trust each other completely. It creates friction when spending habits or priorities differ.

What you need to open one

For Neo, EQ Bank, and Wealthsimple, the entire process happens online: both applicants need government-issued photo ID, a Social Insurance Number, and a Canadian address. Most setups take 10–15 minutes. The primary holder opens the account and invites the co-holder via email — no branch visits required.

Tangerine is the exception: adding a joint holder to an existing account requires a phone call to 1-888-826-4374. Simplii can be opened online but adding a joint holder may require contacting them directly.

Opening a joint account does not affect either person’s credit score. Joint bank accounts are deposit accounts, not credit products. Joint credit products (lines of credit, credit cards) do affect credit — but a joint chequing or savings account does not.

The right of survivorship

In most Canadian provinces, joint accounts carry the right of survivorship: if one account holder dies, the funds automatically transfer to the surviving holder, bypassing the estate process. Quebec is the exception — joint accounts in Quebec are structured as Tenants in Common (TIC), meaning the deceased holder’s share goes to their estate rather than automatically to the survivor. If you’re in Quebec, confirm the account structure before opening.

The best joint accounts in Canada (2026)

Here’s how the main options compare across the features that actually matter for families:

| Account | Type | Interest rate | Cashback | Max holders | ATM access | Monthly fee |

|---|---|---|---|---|---|---|

| Neo Joint Chequing | Chequing | — | 1%–3%* | 2 | Yes — any ATM in Canada | $0 |

| Neo Joint Savings | Savings | 2%–2.75%** | — | 2 | No | $0 |

| EQ Bank Joint | Hybrid | 1.00% base / 2.75%*** | — | 4 | Yes — any ATM (fees reimbursed) | $0 |

| Wealthsimple Chequing (Joint) | Hybrid | 1.25%–2.25%**** | — | 2 | Yes — any ATM globally (fees reimbursed) | $0 |

| Simplii No-Fee Chequing | Chequing | Minimal | — | 2 | Yes — 3,400+ free CIBC ATMs | $0 |

| Tangerine Chequing | Chequing | ~0.01% | — | 2 | Yes — free Scotiabank network | $0 |

*Neo Chequing cashback on gas and groceries via the Neo Money™ Card increases with chequing balance: 1% at $0, 2% at $5,000+, 3% at $10,000+. Cashback is subject to monthly spend limits and resets each month. Members also earn an average of 5% (up to 15%) at thousands of Neo partner locations. **Neo Savings tiered: 2% on balances up to $4,999 / 2.50% up to $19,999 / 2.75% at $20,000+. ***EQ Bank’s 2.75% requires a qualifying direct deposit of $2,000/month; base rate without it is 1.00%. ****Wealthsimple rate depends on total assets held with Wealthsimple across all accounts: 1.25% (under $100K) / 1.75% ($100K+) / 2.25% ($500K+). An additional 0.5% boost applies for Core and Premium clients who direct deposit $2,000/month. All rates variable and subject to change. Rates as of June 2026.

Each account in detail

Neo Joint Chequing — best for shared daily spending

Neo’s joint chequing account is built for the daily transaction flow of a shared household — bills, groceries, subscriptions, direct payments — and it pays you back for using it. Both co-owners get their own Neo Money™ Card and earn cashback independently: 1% on gas and groceries at a $0 balance, rising automatically to 2% at $5,000 and 3% at $10,000, with no action required. On top of that, members earn an average of 5% (up to 15%) at thousands of Neo partner locations across Canada through the Neo app. Cashback is subject to monthly spend limits and resets each month.

Either person can see every transaction in real time, which removes the “did you pay that?” back-and-forth that plagues most couples managing shared expenses. You can open a new joint chequing account entirely online, or add a co-owner to an existing Neo Chequing account — whichever works for your situation.

Neo also layers in optional membership tiers tied to how much you keep with them. Build membership ($7.99/month, free once you hold $5,000+ across any Neo account) adds credit score monitoring and credit-building tools. Grow membership ($12.99/month, free once your combined Neo Chequing and Neo Savings balance hits $20,000+) adds no foreign transaction fees on Neo cards (rebated automatically, capped at $10,000/month in foreign spend) and unlocks the 2.75% top rate on Neo Savings. For a family already planning to pair Neo Chequing with Neo Savings, reaching the Grow threshold pays off on both accounts at once.

- $0 monthly fee, $0 NSF fees

- Cashback on gas and groceries rises with balance — up to 3%

- Average 5% (up to 15%) cashback at 10,000+ Neo partner locations

- Real-time shared transaction visibility

- ATM access anywhere in Canada

- Free Interac e-Transfers and bill payments

- 100% online setup

- 2 holders maximum

- Cashback is capped by monthly spend limits and resets each month

- Top cashback tier (3%) requires a $10,000+ chequing balance

- No physical branches

Neo Joint Savings — best rate for shared savings goals

The Neo Joint Savings account is purely a savings vehicle — no debit card, no transactions. You transfer money in, it earns interest, and you transfer it out when you need it. The joint structure means both partners can contribute and both can see the balance grow toward a shared goal, whether that’s a vacation fund or your emergency fund. Combining balances in a joint account also helps you reach the higher interest tiers faster than saving individually.

Neo is not itself a CDIC member institution. Funds in Neo accounts are held in trust at one or more CDIC member institutions, and eligible deposits may be protected by CDIC up to $100,000 per depositor per insured category.

- Competitive tiered interest — up to 2.75% at $20K+

- $0 fees, no minimum balance

- Combine balances to reach higher tiers faster

- Up to 10 named savings accounts for different goals

- CDIC eligible

- 2 holders maximum

- No debit card — savings only

- Top rate (2.75%) requires $20,000+ combined balance

EQ Bank Joint Account — best for families who want one account for everything

EQ Bank’s joint account is a hybrid: it earns meaningful interest on every dollar while also functioning as a full everyday banking account. Unlimited bill payments, Interac e-Transfers, and EFTs are all free. The EQ Bank Card gives you ATM access anywhere in Canada with fees reimbursed, plus no foreign exchange markup when you travel.

The standout feature for larger families: EQ Bank allows up to four co-holders on a single joint account. No other major digital bank matches this. If you’re managing shared household finances with multiple adults — multigenerational households, blended families, or shared accounts among siblings — EQ Bank is the only no-fee digital option that accommodates this.

- Up to 4 holders — unique among digital banks

- Hybrid: earn interest and transact from one account

- Free ATM withdrawals in Canada (fees reimbursed)

- No FX fees on the EQ Bank Card abroad

- CDIC insured (Equitable Bank, Schedule I)

- Available in Quebec (some feature limitations)

- 2.75% requires $2,000/month direct deposit — base rate is 1.00%

- No cash deposits, no cheques, no branches

- Some Quebec features unavailable (EQ-to-EQ transfers, RRSP/FHSA products)

Wealthsimple Chequing (Joint) — best hybrid for investors

Wealthsimple’s chequing account earns interest on every dollar while functioning as a full transactional account — the same hybrid model as EQ Bank, but with a rate structure tied to your total Wealthsimple relationship rather than direct deposit into the account itself. If you already invest with Wealthsimple and have a meaningful balance, the rate is competitive. If you’re starting fresh with only a chequing account, you’ll earn 1.25%.

One genuinely useful feature: a 0.5% rate boost is available for Core and Premium clients who direct deposit $2,000/month — bringing the base rate to 1.75% (Core) or 2.25% (Premium) if you set up your payroll. The higher rate between both account holders applies to a joint account automatically.

Wealthsimple also offers the highest CDIC-equivalent coverage available: funds are held in trust at multiple CDIC-member institutions, providing up to $1,000,000 in coverage when spread across at least 10 institutions — far exceeding the $100,000 per category cap at a single bank. For families with significant cash balances, this matters.

- Hybrid: earns interest AND transacts from one account

- No monthly fees, no FX fees, ATM fees reimbursed globally

- Up to $1M deposit coverage (trust structure across multiple CDIC members)

- Up to 8 joint chequing accounts

- Available in Quebec (Tenants in Common structure)

- Rate boost available with $2,000/month direct deposit

- Interest rate tied to total WS assets — new users start at 1.25%

- Best rates require $100K+ or $500K+ total Wealthsimple assets

- 2 holders per joint account

- Wealthsimple is not a bank (though deposit protection is strong)

Simplii No-Fee Chequing — best for CIBC ATM access

Simplii’s joint chequing account is straightforward: no monthly fees, unlimited transactions, and free access to 3,400+ CIBC ATMs across Canada. It’s the right choice for families who need reliable physical ATM infrastructure and want to stay within a major bank’s ecosystem without paying monthly fees.

The interest on the chequing balance is minimal — this is a spending account, not a savings vehicle. Use it for transactions and pair it with a dedicated savings account elsewhere. New Simplii clients can also earn $300 cash plus a $50 Skip gift card by opening a chequing account and setting up a direct deposit of $100/month for three consecutive months (offer ends September 30, 2026).

- $0 monthly fees, no minimum balance

- Free access to 3,400+ CIBC ATMs

- CDIC insured (division of CIBC)

- $300 + $50 Skip welcome bonus (new clients, ends Sept 30, 2026)

- Overdraft protection available

- Minimal interest — not a savings vehicle

- 2 holders maximum

- Customer service consistently rated below peers

Our recommendations

The right joint account depends on how your family uses money. Here’s our read on who each account is actually built for.

Neo’s joint chequing account pays you back for everyday spending: cashback on gas and groceries starts at 1% and rises automatically to 3% as your balance grows, plus an average of 5% (up to 15%) at thousands of Neo partner locations. Both holders earn independently, with real-time shared transaction visibility and free ATM access anywhere in Canada. Set up takes minutes online, with no monthly fees.

Open a Neo Chequing account →Pair Neo’s chequing account with their joint savings account for the other half of the system — up to 2.75% interest on balances of $20,000+, no fees, and named savings goals both partners can contribute toward and track.

Open a Neo Savings account →If you’d rather manage one account than two, EQ Bank’s joint account earns interest on every dollar while letting you pay bills, send e-Transfers, and use the EQ Bank Card at any Canadian ATM for free. The rate hits 2.75% if you direct deposit your pay — and EQ Bank is the only no-fee digital option that supports up to four co-holders. Multigenerational households, parents with adult children, or anyone managing finances for more than two people should look here first.

Open an EQ Bank account →If you already invest with Wealthsimple, adding a joint chequing account makes the most sense here — your combined Wealthsimple balance determines the interest rate, so an existing investment relationship improves the rate automatically. Families with significant assets with Wealthsimple will earn 1.75%–2.25% with no effort. The $1M deposit coverage ceiling is also the strongest available for high-balance households.

Open a Wealthsimple account →For families who regularly withdraw cash and want free access to a large ATM network, Simplii’s joint chequing account gives you the CIBC infrastructure at zero monthly cost. The $300 welcome bonus makes it worth opening for new clients. Pair it with a separate high-interest savings account for your savings goals.

Open a Simplii account →CDIC coverage and joint accounts

One thing worth understanding before you open a joint account: the deposit insurance works differently for joint accounts than individual ones, and in most cases it works in your favour.

At a CDIC member institution (EQ Bank, Simplii, Tangerine), joint deposits are insured separately from each individual’s personal deposits — up to $100,000 per set of co-holders. A couple with individual accounts and a joint account at EQ Bank could have up to $300,000 of CDIC coverage across three separate insured categories.

For the full picture on how CDIC categories work, the CDIC’s joint account coverage page lays it out clearly.

Wealthsimple is not itself a CDIC member — it holds your funds in trust at multiple CDIC-member institutions. This structure provides up to $1,000,000 in effective coverage when spread across at least 10 institutions. For families with joint balances well above $100,000, this is meaningfully stronger than a single-bank structure.

How joint account interest is taxed

Interest earned in a joint account is taxable income — but it isn’t automatically split 50/50. The CRA uses proportionate reporting: each account holder reports interest based on how much they contributed to the account.

In practice, most couples split contributions equally and each report half the interest on their individual tax returns. If one partner contributes more, they report proportionally more of the income. A simple record of contributions is all you need to back this up if the CRA ever asks.

One practical implication: if one partner is in a lower tax bracket, it may make sense to structure contributions so they hold the larger share of a joint savings account. The interest earned on their portion gets taxed at the lower rate, reducing the household’s overall tax bill. This is a straightforward, legal income-splitting approach available to any couple with different marginal rates.

For the authoritative guidance on this, the CRA’s resources on reporting interest income apply. If you’re unsure how to handle your specific situation, a tax professional can walk through the calculation.

The Bottom Line

For most Canadian families, the best setup is two accounts: a joint chequing account for shared spending and a joint savings account for shared goals. Neo makes this the simplest — their joint chequing and joint savings accounts work as a pair inside one app, both free, both online.

If you’d rather manage one account for both purposes, EQ Bank is the stronger choice: it earns real interest, handles everyday transactions, and uniquely supports up to four co-holders — something no other no-fee digital bank offers. Wealthsimple is the better hybrid option if you’re already invested there and your combined balance qualifies for the higher rate tier.

All interest rates are variable and change with the Bank of Canada’s overnight rate. Verify the current rate directly with each institution before opening an account.Once your joint accounts are set up, the next step is making sure money actually moves between them on its own. How to Automate Your Family Finances walks through setting up automatic transfers so your spending and savings accounts stay funded without manual effort every month.

Frequently Asked Questions

Any two Canadians who meet standard eligibility requirements can open a joint account together — couples, roommates, adult children with parents, siblings, business partners. There is no legal requirement that joint account holders be in a relationship. The only real requirement is that both parties trust each other completely, since either person can access and withdraw all funds independently.

No. Joint deposit accounts — chequing and savings — are not credit products and do not appear on your credit report. Opening or closing a joint chequing or savings account has no impact on either person’s credit score. Joint credit products, like a joint credit card or joint line of credit, are different — those do affect credit because they involve borrowing. But a joint bank account does not.

Either account holder can withdraw all funds at any time — the bank will not intervene in a dispute between account holders. If a relationship breaks down, the practical risk is that one person withdraws the balance before you can act. In provinces other than Quebec, the joint account may also be treated as a matrimonial asset in a divorce and subject to division. The safest approach when a joint account is no longer working is to transfer out your agreed share and close the account by mutual agreement as quickly as possible.

No. TFSAs and RRSPs are individual accounts by CRA definition — they can only be held in one person’s name. There is no such thing as a joint TFSA or joint RRSP in Canada. You and your partner can each have your own TFSA and RRSP, and you can name each other as beneficiaries, but the accounts themselves remain individual. Joint accounts are available only for non-registered deposit accounts.

There is no rule on how you split contributions — that’s entirely up to you. Many couples contribute equally; others contribute based on a percentage of each person’s income. What matters for tax purposes is keeping track of the proportion each person contributes, since each person reports interest income proportional to their contributions. If one partner is in a meaningfully lower tax bracket, having them contribute the larger share reduces the household’s overall tax bill on the interest earned.

Yes, but only with certain accounts. EQ Bank allows up to four co-holders on a single joint account — the only no-fee digital bank in Canada that does this. Tangerine allows up to four holders on savings accounts and GICs, though their chequing account is limited to two. Neo, Wealthsimple, and Simplii all cap joint accounts at two holders. If you need more than two people on one account, EQ Bank is the only no-fee digital option worth considering.

EQ Bank and Wealthsimple both support Quebec residents on joint accounts, though with structural differences. EQ Bank joint accounts are available in Quebec but with some feature limitations — EQ-to-EQ transfers are not available, and some registered account products are also unavailable. Wealthsimple joint chequing accounts are structured as Tenants in Common (TIC) in Quebec rather than Joint with Rights of Survivorship, which means a deceased holder’s share goes to their estate rather than automatically to the surviving holder. Tangerine (owned by Scotiabank) also accepts Quebec residents. Neo’s accounts do not state a Quebec restriction on their website. In all cases, verify directly with the institution before opening.

Want to put this into a complete financial system? Read A Simple Family Finance System for Canadians — a practical framework for organizing every account your family needs and automating the money flow between them.