If you’re raising a family in Canada, income tax is not just something you deal with once a year. It quietly shapes how much money you keep, what benefits you receive, and how efficiently you can build wealth over time.

Most families focus on earning more or cutting expenses, but very few take the time to understand how the tax system actually works. That gap leads to missed deductions, inefficient decisions, and money left on the table year after year.

This guide explains how Canadian income tax works, what families actually pay once benefits and credits are factored in, and how tax decisions fit into your broader financial system.

This article contains affiliate links. We may earn a commission if you open an account — at no cost to you. We only recommend products we’ve researched and trust.

TAXES

TAXES

In This Article

- What Is Income Tax in Canada?

- Canadian Tax Brackets (2026)

- How Tax Actually Works in Practice

- Total Income vs Taxable Income

- Tax Credits vs Deductions

- How Families Are Taxed in Canada

- Government Benefits and Why They Matter

- What Families Actually Pay

- Types of Income and Tax Efficiency

- Registered Accounts and Long-Term Tax Strategy

- Tax Planning Throughout the Year

- Filing Your Taxes

- How Taxes Fit Into Your Financial System

What Is Income Tax in Canada?

Income tax in Canada is progressive, which means your income is taxed in layers rather than at a single flat rate. As your income increases, higher tax rates apply—but only to the portion of income within each bracket, not your entire income.

Every working Canadian pays both federal tax and provincial tax, which are combined into a single system and administered by the Canada Revenue Agency when you file your return. If you want to see how the system is structured at a high level, you can review the CRA’s overview of income taxes in Canada.

This layered system is the reason tax planning works at all. Because taxes are not flat, even small reductions in taxable income can reduce how much of your income is exposed to higher rates.

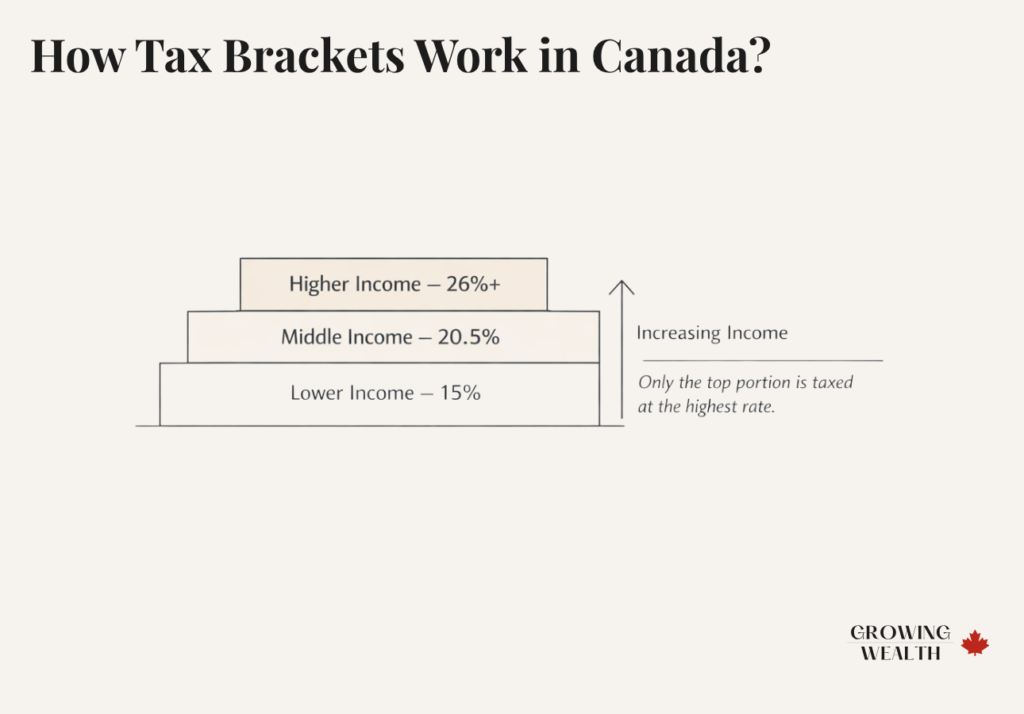

Canadian Tax Brackets (2026)

Canada’s tax system is built on tax brackets, and misunderstanding this is where most confusion begins. Many people assume that moving into a higher bracket means all of their income is taxed at that higher rate. It does not.

Here are the federal brackets for 2026:

| Taxable Income | Federal Rate |

|---|---|

| $0 – $58,523 | 14% |

| $58,523 – $117,045 | 20.5% |

| $117,045 – $181,440 | 26% |

| $181,440 – $258,482 | 29% |

| Over $258,482 | 33% |

Federal rates only — provincial tax applies on top of these. Source: CRA, 2026. These thresholds are indexed to inflation and adjust every January.

You can view the current Canadian income tax rates (federal brackets) on the CRA website.

These rates apply nationally, while provinces apply their own additional tax rates. Your total tax burden depends on both your income and where you live.

If you want to understand exactly how income flows through each bracket and how each portion is taxed, a deeper explanation is covered in How Tax Brackets Work in Canada.

How Tax Actually Works in Practice

When people say they are “in a tax bracket,” they are simplifying something more precise.

If you earn $100,000, your income is divided across multiple brackets. The first portion is taxed at the lowest rate, the next portion at a higher rate, and only the top portion is taxed at your highest marginal rate. This means earning more money will always result in more after-tax income.

This structure is what makes deductions effective. When you reduce taxable income, you are often reducing income that would have been taxed at your highest rate. This is especially relevant when deciding whether to contribute to an RRSP, which is explained more clearly in How RRSP Contributions Reduce Your Taxes.

Total Income vs Taxable Income

Your total income includes everything you earn during the year—employment income, side income, rental income, and investment income. Your taxable income is what remains after deductions are applied.

This is the number that determines how much tax you actually pay. Deductions such as RRSP contributions, childcare expenses, and certain employment-related costs reduce taxable income and can significantly lower your tax bill.

In practice, this is where attention to detail matters. Taking the time to organize your documents and review what applies to you can make a meaningful difference. Using a Tax Filing Checklist for Canadians helps ensure that nothing important is missed.

Tax Credits vs Deductions

Understanding the difference between tax deductions and tax credits is essential.

Tax deductions reduce your taxable income before tax is calculated. Tax credits reduce the amount of tax you owe after it has been calculated.

Both are valuable, but they work in different ways. Some strategies reduce how much of your income is taxed, while others reduce your final tax bill directly.

How Families Are Taxed in Canada

Canada taxes individuals rather than households, but many benefits are based on combined family income.

This means your financial decisions affect both your tax bill and what your household receives in benefits. For families, understanding this connection is critical when evaluating income changes, deductions, and long-term planning.

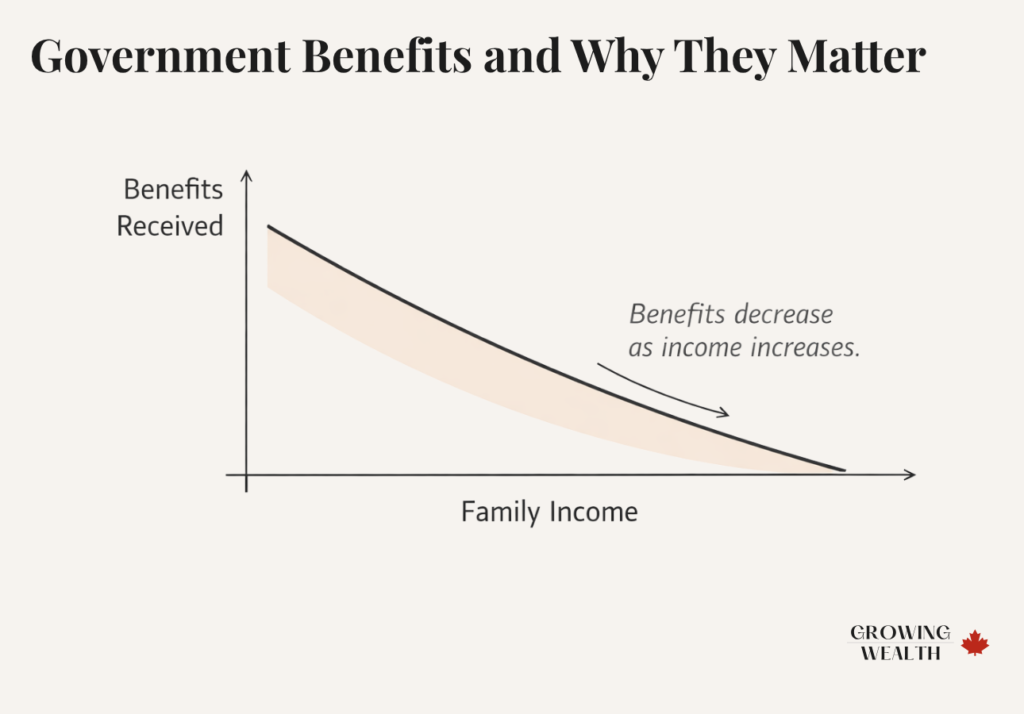

Government Benefits and Why They Matter

Government benefits are closely tied to your tax return and can significantly affect your household finances.

The Canada Child Benefit (CCB) is a tax-free monthly payment available to families with children under 18, and the amount is based on adjusted family net income. As income rises, the benefit is gradually reduced. You can review how the Canada Child Benefit works.

If you want to estimate your payments, you can use the Canada Child Benefit calculator.

The GST/HST credit provides quarterly tax-free payments based on income. You can review how the GST/HST credit works.

Because these benefits are income-tested, income increases can reduce what you receive. This is one reason many families look at ways to reduce their overall tax burden, which is explored further in tips to reduce your Canadian tax bill.

What Families Actually Pay

Tax brackets alone do not reflect what families actually pay once deductions, credits, and benefits are considered.

A family earning $90,000 with children may pay less tax than expected once benefits are included. At higher income levels, taxes increase while benefits are reduced or eliminated.

If a refund is generated, the next step matters. Deciding how to use that money can affect your long-term financial progress, which is why it helps to have a clear plan for what to do with your tax refund.

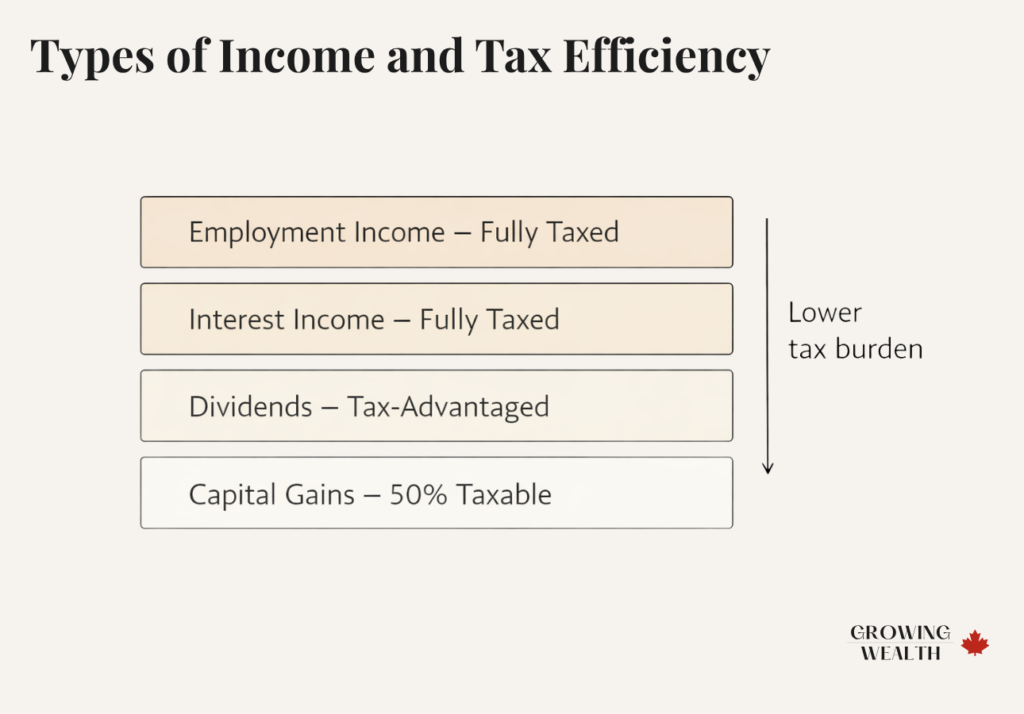

Types of Income and Tax Efficiency

Not all income is treated equally under the tax system.

Employment income and interest income are fully taxable, while dividends receive more favourable treatment and capital gains are only partially taxed. This means that how you earn income matters just as much as how much you earn.

For families building long-term wealth, understanding how income is structured becomes increasingly important, especially when paired with a broader investing approach such as how to start investing in Canada.

Registered Accounts and Long-Term Tax Strategy

Registered accounts are one of the most effective tools for managing taxes over time.

An RRSP reduces taxable income today, while a TFSA allows investments to grow and be withdrawn tax-free. TFSA withdrawals also do not affect income-tested benefits, which can make them particularly useful for families.

Choosing between these accounts depends on your situation, and a more detailed comparison is covered in TFSA vs RRSP strategy in Canada.

If you’re saving for a first home, the FHSA adds a third option — our FHSA vs TFSA vs RRSP comparison explains how all three work together as part of a tax strategy.

Tax Planning Throughout the Year

Tax planning is not something that should only happen at filing time. It is shaped by decisions made throughout the year.

This includes when you earn income, how you use registered accounts, and which deductions you claim. Even small adjustments can lead to meaningful improvements over time.

Filing Your Taxes

Filing your taxes involves reporting income, applying deductions, calculating tax, and determining whether you owe money or receive a refund.

For many households, tax software is sufficient. For more complex situations, professional advice may be helpful.

Having a clear structure simplifies the process and reduces the chance of errors, especially when you take the time to prepare properly before filing.

How Taxes Fit Into Your Financial System

Taxes influence your savings, your investments, and your overall financial progress.

When taxes are considered alongside saving and investing decisions, outcomes tend to be more efficient. A structured approach, such as a simple family finance system for Canadians, helps bring these elements together into a single system.

Consistency is equally important. Strong financial habits make it easier to follow through on decisions and maintain progress over time, which is explored further in the power of financial habits.

The Bottom Line

The Canadian tax system can feel complicated at first, but it follows consistent rules. Once you understand how tax brackets apply, how taxable income is calculated, and how benefits are affected by income, the system becomes easier to navigate.

Most families do not need advanced strategies. They need clarity—understanding how their income interacts with the system and how to make better decisions throughout the year.

When taxes are treated as part of a broader financial system rather than a once-a-year task, the results build steadily over time.

Frequently Asked Questions

The exact amount depends on your province, deductions, and credits. Most individuals fall within a 20–30% effective tax range, even though their marginal rate may be higher. Benefits and credits can further reduce what a family actually pays.

The basic personal amount is a federal tax credit that allows you to earn a portion of income before tax applies. It reduces your final tax bill rather than your taxable income. Most Canadians automatically receive this when filing their return.

No, the Canada Child Benefit is completely tax-free. It is not included as income on your tax return. However, your household income determines how much you receive.

The GST/HST credit is based on your family income reported on your tax return. The CRA calculates eligibility automatically, so no separate application is required. Payments are issued quarterly if you qualify.

Common methods include RRSP contributions, childcare expense deductions, and claiming eligible expenses. Reducing taxable income lowers the portion of income exposed to higher tax rates. Over time, this can significantly reduce total taxes paid.

Tax planning should happen throughout the year, not just during tax season. Many of the most effective strategies require decisions in advance. Waiting until you file limits your ability to optimize your outcome.

Want to turn what you’ve just learned into a concrete plan? Read FHSA vs TFSA vs RRSP: Which Should You Use? — the natural next decision once you understand how your tax picture works.