By:

Growing Wealth

Published:

Most people don’t struggle with investing because it’s complicated—they struggle because they feel like they need to get it exactly right before they start.

There are too many options, and most of them sound important. ETFs, stocks, funds, strategies—it creates the impression that investing is complex. It isn’t.

At its core, investing in Canada comes down to a few things: diversification, low costs, and consistency. And those principles don’t exist in isolation—they’re part of a broader system. If you don’t already have structure in place, building one through A Simple Family Finance System for Canadians makes investing easier to stick with long-term.

If you’re still setting up your process, start with How to Start Investing in Canada. This guide focuses on what comes next—what you should actually invest in.

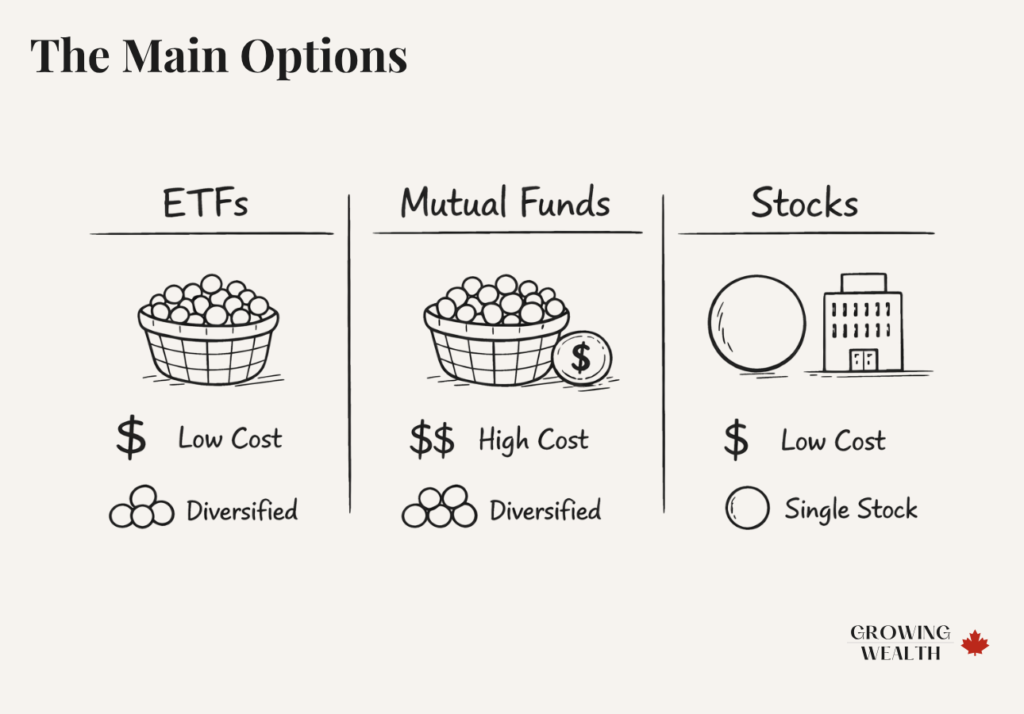

The Main Options (ETFs, Mutual Funds, Individual Stocks)

When you invest, you’re typically choosing between three structures. They all give you market exposure, but they behave very differently.

Here’s how they compare at a high level:

| Investment Type | Cost | Diversification | Effort Required | Best For |

|---|---|---|---|---|

| ETFs | Low | High | Low | Most investors |

| Mutual Funds | High | High | Low | Convenience (but costly) |

| Individual Stocks | Low | Low | High | Experienced investors |

ETFs (Exchange-Traded Funds)

ETFs are the simplest way to invest today. Instead of choosing individual companies, you buy a fund that holds hundreds or thousands of them.

They offer:

- Instant diversification

- Low fees

- Minimal maintenance

This combination is what makes them the default choice for most investors.

Mutual Funds

Mutual funds look similar on the surface but operate differently behind the scenes. They are actively managed, meaning someone is trying to outperform the market.

The trade-off is cost.

Most Canadian mutual funds charge 1.5%–2.5% annually, and over time, that compounds against you. When you compare performance using tools like Morningstar Canada, the higher fees rarely result in better long-term outcomes.

Individual Stocks

Buying individual companies introduces a different level of involvement.

You gain more control—but also more responsibility. You need to monitor performance, stay informed, and accept that a few poor choices can significantly impact your results.

For most beginners, this adds complexity without improving returns.

Why Most Investors Should Start With ETFs

ETFs remove the biggest obstacles before they become problems.

Instead of building diversification manually, it’s already built in. Instead of worrying about fees, they’re kept low by design. And instead of constantly deciding what to buy, you follow a consistent approach.

If you look at the model portfolios from Canadian Couch Potato, you’ll see they rely heavily on ETFs. That’s not a trend—it’s a reflection of what actually works over time.

More importantly, ETFs support behaviour. Investing success is less about picking the perfect asset and more about what you consistently do over time—which is exactly what’s reinforced in The Power of Financial Habits.

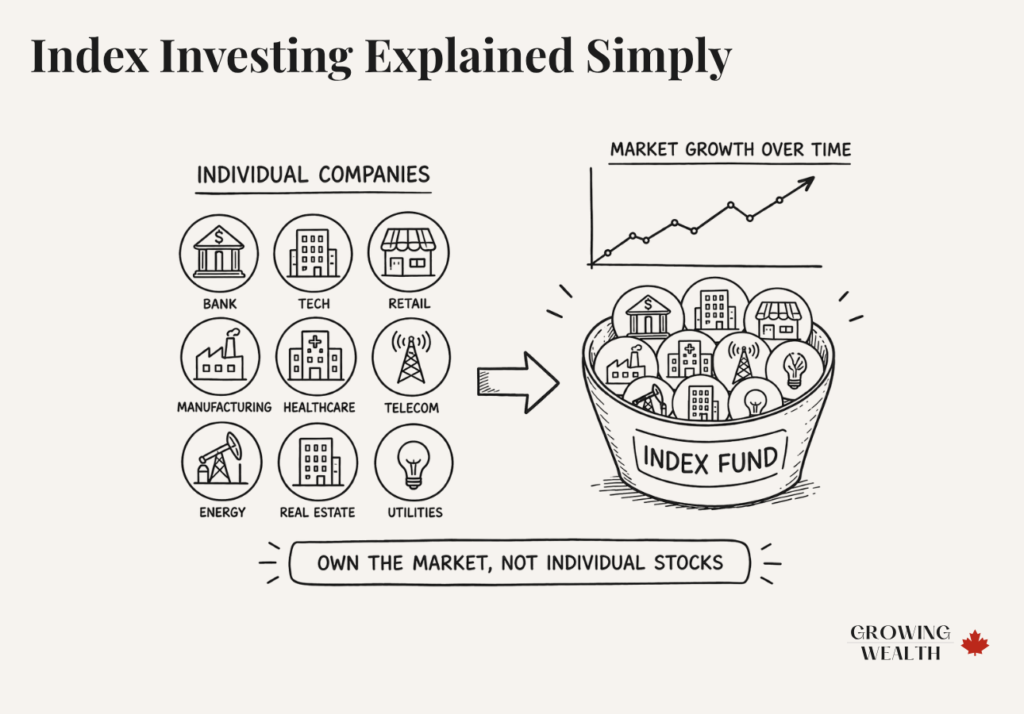

Index Investing Explained Simply

Index investing is the foundation behind most ETFs.

Rather than trying to pick individual winners, you invest in a broad market index. That could be Canadian companies, U.S. companies, or the global market as a whole.

Over time:

- The market overall trends upward

- Some companies fail

- Some grow significantly

By owning the index, you participate in that growth without needing to predict outcomes.

This approach is widely supported by firms like Vanguard Canada and backed by decades of performance data. It’s simple, but that’s exactly why it works.

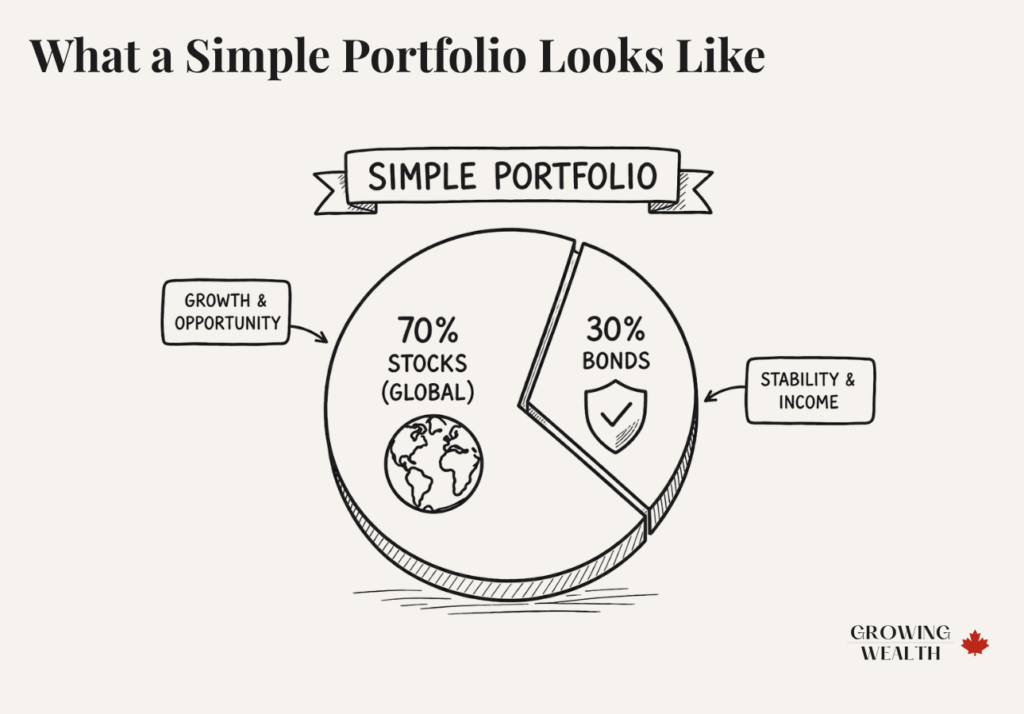

What a Simple Portfolio Looks Like

A common mistake is assuming that a good portfolio needs to be complex. In reality, most effective portfolios are surprisingly simple.

For many investors, a single all-in-one ETF is enough. It already includes global stocks—and sometimes bonds—so you’re diversified across regions and sectors in one investment.

If you want slightly more control, you might separate things into two or three funds. For example:

- A global stock ETF

- A bond ETF

- Separate Canadian, U.S., and international exposure

But more funds don’t automatically improve results—they just introduce more decisions. For most people, simplicity leads to better consistency.

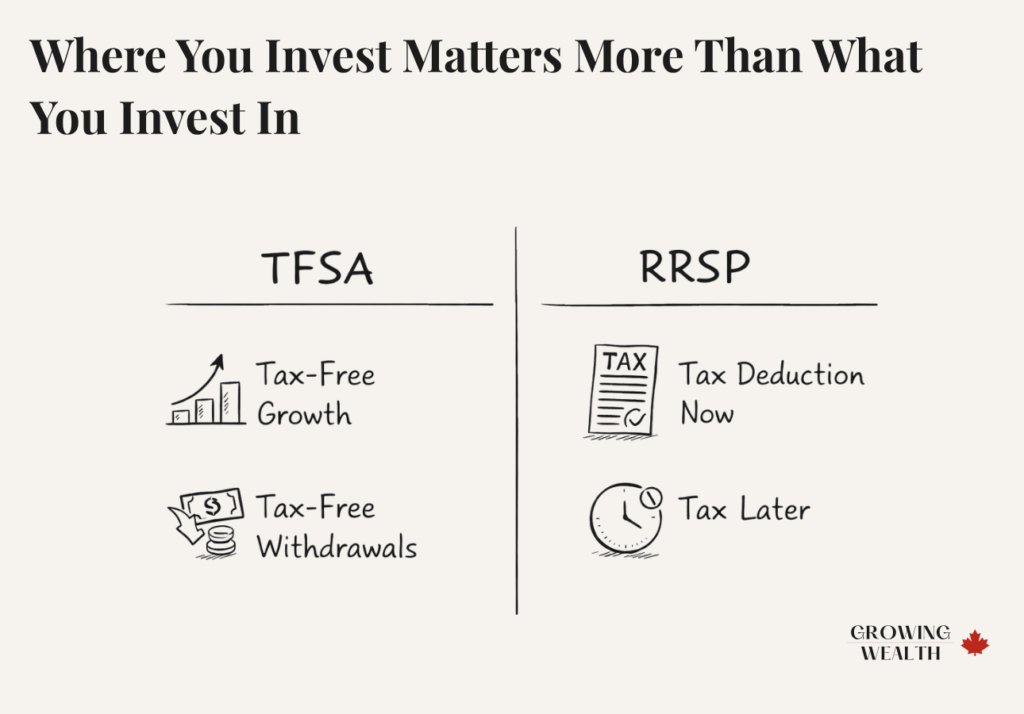

Where You Invest Matters More Than What You Invest In

Before choosing investments, you need to choose the right account. In Canada, this directly affects your long-term returns.

A TFSA allows your investments to grow and be withdrawn tax-free, making it the most flexible starting point for most people.

An RRSP provides a tax deduction upfront and defers taxes until withdrawal, which can be more beneficial at higher income levels.

Choosing between them depends on your situation, and the differences are important. The breakdown in TFSA vs RRSP: Which Should You Use First? walks through when each one makes sense.

If you’re a first-time home buyer, the FHSA is a third account worth understanding — our FHSA vs TFSA vs RRSP comparison shows how all three fit together.

If you continue investing beyond these accounts, taxable accounts become the next step—but they are less efficient due to ongoing taxes.

It’s also worth being intentional about which investments belong in your RRSP specifically — bonds and U.S. dividend ETFs benefit most from tax deferral, while growth assets are usually better placed in a TFSA.

Common Mistakes (Stock Picking, Overcomplication)

Most investing mistakes aren’t about picking the wrong ETF—they’re about behaviour.

A few patterns show up repeatedly:

- Starting with individual stocks too early

- Building overly complex portfolios

- Waiting for the “right time” to invest

- Chasing trends after they’ve already risen

- Overlooking fees and their long-term impact

Most of these come down to inconsistency, not knowledge. That’s why having a structured system—and reinforcing it through habits—is more impactful than trying to optimize every decision.

When You Should NOT Be Investing Yet

Investing isn’t always the immediate next step.

If you don’t have an emergency fund, you may be forced to sell investments at the worst possible time. Building a cash buffer first is a more stable foundation, and Emergency Fund: How Much You Really Need explains how to structure that.

Short-term money is another issue. If you need funds within one to three years, market volatility becomes a risk rather than an advantage. In those cases, a high-interest savings account is more appropriate, which is covered in High Interest Savings Accounts in Canada.

High-interest debt also changes the equation. Paying off expensive debt often provides a more reliable return than investing.

Example Beginner Portfolio

A beginner portfolio doesn’t need to be complicated.

Start with a TFSA (see TFSA vs RRSP), choose a broadly diversified ETF, and invest consistently. That could be monthly or aligned with your paycheque.

From there, the most important step is to stay consistent—and that’s easier when investing is part of a broader system like A Simple Family Finance System for Canadians.

If you’re deciding where to invest, the platform you choose matters. The comparison in Wealthsimple vs Questrade helps clarify whether you prefer a more automated experience or more control.

Should You Invest All at Once or Over Time?

One of the most common questions is whether you should invest a lump sum immediately or spread it out over time.

If you have cash ready to invest, the instinct is often to wait or ease in slowly. That usually comes from a fear of investing at the “wrong time.”

There are two main approaches:

- Lump sum investing: You invest all your money at once

- Dollar-cost averaging (DCA): You invest gradually over weeks or months

Historically, investing a lump sum has produced better long-term results because your money is in the market sooner. But that doesn’t mean it’s always the right choice.

Dollar-cost averaging can make it easier to stay consistent, especially if you’re worried about short-term market swings. It reduces the emotional pressure of timing the market—even if it slightly reduces expected returns.

The better strategy is the one you can actually follow.

If you’re unsure which approach fits your situation, this breakdown of Lump Sum vs Dollar-Cost Averaging in Canada walks through when each strategy makes sense.

Conclusion

You don’t need a complex strategy to succeed.

What matters is having a structure that is diversified, low-cost, and easy to maintain. Most long-term results come from consistency, not from trying to optimize every decision.

And ultimately, success in investing isn’t about one perfect choice—it’s about repeating the right actions over time, which is exactly what strong financial habits reinforce.

Frequently Asked Questions

What is the best investment for beginners in Canada?

A low-cost ETF that provides broad market exposure is the most practical starting point. It offers diversification and requires minimal management.

Should I invest in stocks or ETFs?

ETFs are generally better for beginners because they spread risk across many companies, while individual stocks rely on the performance of a few.

How many ETFs do I need?

In most cases, one well-diversified ETF is enough. Adding more doesn’t necessarily improve results.

Is it safe to invest in ETFs?

They are not risk-free, but they reduce risk through diversification. The main risk comes from overall market movements.

What is the safest place to keep money in Canada?

For short-term savings, a high-interest savings account is safer than investing. See High Interest Savings Accounts in Canada for options.

Can I lose money investing in ETFs?

Yes, especially in the short term. Long-term investing reduces this risk as markets recover and grow.

How much should I invest each month?

The amount matters less than consistency. A structured approach is outlined in How Much Should You Invest Each Month.

Affiliate Disclosure

💡 GrowingWealth.ca is supported by readers. Some of the links in this article are affiliate links, which means we may earn a small commission if you open an account or make a purchase — at no extra cost to you. We only recommend products and services we personally use, trust, or believe provide genuine value to Canadians. Our reviews and comparisons are always independent and objective.