Banking

Banking

Most people manage their money with one chequing account and a vague sense of how much is “safe” to spend. Bills, groceries, savings, and whatever’s left over all sit in the same pool, which means every purchase is really a guess about what you haven’t paid yet. Knowing how to structure your bank accounts fixes that guesswork before it starts. The fix isn’t a better budgeting app or more willpower. It’s separating your money by job, then automating the transfers so the separation happens without you.

This article contains affiliate links. We may earn a commission if you open an account — at no cost to you. We only recommend products we’ve researched and trust.

In This Article

| Account | Job | Type | Automation |

|---|---|---|---|

| Primary chequing | Receives income, pays bills | Chequing | Direct deposit lands here |

| Spending account | Groceries, gas, everyday debit | Chequing | Auto-transfer, payday +1 day |

| Savings / goals | Vacation, home, car, sinking funds | High-interest savings | Auto-transfer, payday +1 day |

| Emergency fund | 3–6 months expenses, untouched | High-interest savings | Auto-transfer, smaller fixed amount |

Why One Account Keeps Failing You

A single chequing account can’t tell you what’s actually free to spend. Your balance includes rent that’s due in eight days, the hydro bill that hasn’t cleared yet, and the $200 you meant to put toward your emergency fund. Every time you check your balance and it looks “fine,” you’re making a spending decision based on money that’s already spoken for.

This isn’t a discipline problem. It’s a visibility problem. You can’t budget well against a number that doesn’t mean anything, which is the same reason our guide to budgeting in Canada pushes automation over willpower as the foundation of a budget that actually holds.

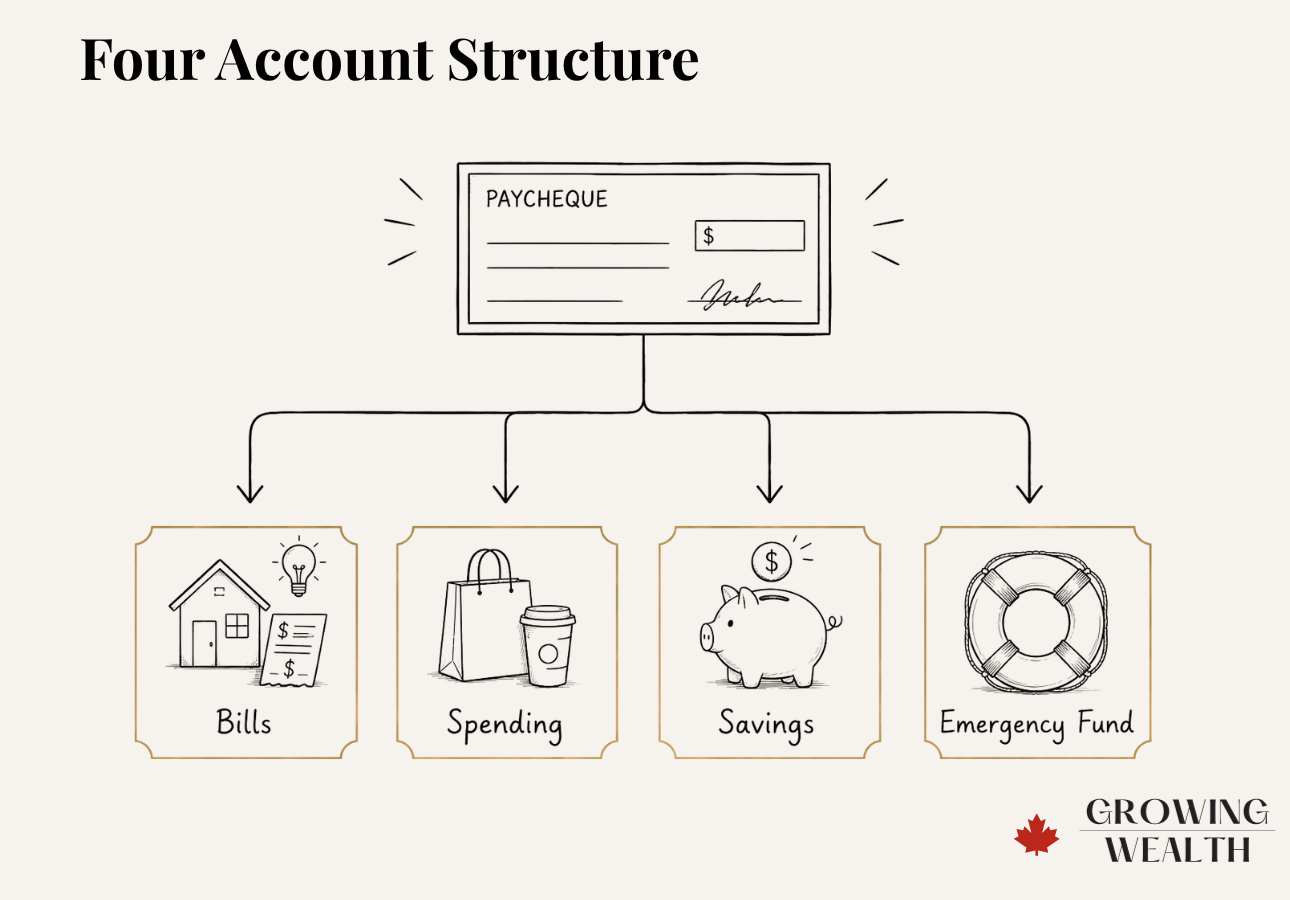

How to Structure Your Bank Accounts: The Four-Account System

You don’t need eight accounts and a spreadsheet to fix this. Four accounts, each with one job, covers almost every household.

Your paycheque lands here and nowhere else. This account exists to receive income and pay fixed bills: rent or mortgage, utilities, insurance, loan payments, subscriptions. Nothing else touches it.

A second chequing account funded by an automatic transfer right after payday. This is groceries, gas, dining out, and everyday debit purchases. The balance here is genuinely spendable, because bills already left it out of the equation.

A high-interest savings account for the things you’re actively saving toward: a vacation, a car, a home down payment, holiday spending. If you’re saving for more than one goal, most digital banks let you create named sub-accounts or “spaces” inside this one account, so you’re not opening five separate ones.

Kept completely separate from your goals savings so a vacation fund never quietly becomes your emergency fund when the car breaks down. This one is meant to sit untouched, growing at the best interest rate you can get, until you actually need it. Our emergency fund guide covers exactly how much to target and where to keep it.

Four accounts, two institutions at most, and every dollar has exactly one job. This is really all there is to how to structure your bank accounts well: fewer accounts than people assume, each with a single clear purpose.

How to Time the Automation

The structure only works if the transfers happen without you. Here’s the sequence:

Same as always, on payday.

Automatic transfers move a fixed amount to your spending account and your savings/goals account. Waiting a day or two lets any pending deposits clear first, so you’re not transferring money that bounces.

Set to their due dates, after the transfers above have already moved money out, so the bill money never gets treated as spendable.

A smaller automatic transfer, timed the same way, so it’s never competing with your active savings goals for the same leftover dollars.

Most Canadian banks let you set up recurring automatic transfers through online banking with no need to involve your employer. If your workplace does offer split direct deposit, that’s a bonus, but check with your payroll or HR department first. Not every Canadian employer supports it, and the automatic-transfer method above works just as well without it.

Worked Example: Priya and Daniel’s $95,000 Household

Priya and Daniel bring home a combined $95,000 after tax. Their fixed bills total $3,100 a month: mortgage, property tax, utilities, insurance, and a car loan. Here’s how the structure runs each payday.

Their full paycheque lands in primary chequing, which pays the $3,100 in fixed bills. One day later, the rest moves out automatically.

Nothing here requires Priya or Daniel to move money manually. The system runs itself every two weeks, and their spending account balance is always an honest number. This account structure is really just one piece of a simple family finance system — the same logic extends to debt payoff, investing contributions, and long-term goals.

Is Your Money Safe Across Multiple Accounts?

Splitting your money across accounts doesn’t reduce your protection, if anything, it can increase it. The Canada Deposit Insurance Corporation (CDIC) insures eligible deposits up to $100,000 per depositor, per separate deposit category, per member institution. Chequing and savings accounts fall into different insured categories than TFSAs or RRSPs, so spreading money across account types at a CDIC member institution doesn’t put you at risk. For the amounts most households keep in day-to-day chequing and savings accounts, this isn’t something to worry about, but it’s worth knowing the coverage is there.

Where to Open Each Account

You don’t need four accounts at four different banks. Most households do well with one digital bank for chequing plus spending, and a separate high-interest account for savings and the emergency fund, so the “spendable” and “untouchable” money live in genuinely different places. Our full breakdown of the best bank accounts in Canada covers the wider field if you want to compare beyond the three below.

Pairs a no-fee chequing-style account with a high-interest savings account under one login, which makes setting up the automatic transfers above simple to manage in one place.

Open an EQ Bank account →A solid no-fee choice if you want your primary chequing and spending accounts backed by a major bank’s infrastructure, without monthly fees.

Open a Simplii account →Worth considering for the spending or goals side of this structure. Neo is not a bank; funds are held in trust at one or more CDIC member institutions, and cashback on gas and groceries is earned through the Neo Money™ Card, which is powered by the Neo Chequing account.

Open a Neo Chequing account →If none of these three feel right, our best digital banks in Canada guide ranks the rest of the field by interest rate, fees, and budgeting tools.

Mistakes That Break the System

If you’re eyeballing your primary chequing balance to decide what’s safe to spend, the system hasn’t actually taken effect yet. Check the spending account instead.

The two need different rules. Goals savings gets spent on purpose. Emergency funds don’t get touched until there’s an actual emergency.

Six or eight hyper-specific accounts sounds organized but usually collapses within months. Start with four. Add a fifth only if there’s a clear, recurring need.

Automated transfers run on autopilot, which is the point, but they don’t adjust themselves. Revisit the amounts every six months.

Pros and Cons

- Removes the guesswork from “can I afford this”

- Protects bill money from accidental spending

- Builds savings and emergency funds without relying on willpower

- Works with any Canadian bank that offers online transfers, no employer cooperation required

- Takes an hour or two to set up correctly the first time

- Multiple accounts mean multiple logins, unless you consolidate at one or two institutions

- Fixed transfer amounts need manual adjustment when income or bills change

- Not useful if you don’t already know your actual fixed bill total

The Bottom Line

If you’re currently checking one account balance and hoping it covers everything, this structure fixes that in a weekend. Once you know how to structure your bank accounts, the rest is just letting automation do the work. Set up primary chequing, a spending account, a goals savings account, and a separate emergency fund, then automate the transfers to run one to two days after each paycheque.

For most dual-income households, EQ Bank or Simplii covers the chequing and savings side cleanly under one login, with Neo Chequing as an option for the spending or goals piece. The system does the discipline for you. You just have to build it once.

Frequently Asked Questions

Four covers almost every household: primary chequing, a spending account, a savings/goals account, and a separate emergency fund. More than that usually becomes hard to maintain.

No. Many households keep everything at one or two institutions and use named sub-accounts or savings “spaces” for individual goals instead of opening a new account for each one.

No. Chequing and savings accounts aren’t reported to the credit bureaus the way credit products are, so opening several doesn’t affect your credit score.

You don’t need it. Set your full paycheque to land in your primary chequing account, then use your bank’s automatic transfer feature to move money to your other accounts one to two days later.

Yes, and it can actually help. Keeping your emergency fund somewhere slightly less convenient to access makes it less tempting to dip into for non-emergencies.

That depends on your target (most households aim for three to six months of expenses) and your timeline. A fixed amount that gets you there in twelve to eighteen months is a reasonable starting point.

This is why the transfers are timed one to two business days after payday rather than the same day. It gives your deposit time to clear before money moves back out.

Yes, but instead of automating a fixed amount every payday, automate a percentage-based transfer each time you deposit income, so the split adjusts with what you actually earn that month.

Want to turn this account structure into a full system? Read How to Automate Your Family Finances — the complete framework for bill scheduling, savings automation, and the review rhythm that keeps it all running.