This article contains affiliate links. We may earn a commission if you open an account — at no cost to you. We only recommend products we’ve researched and trust.

HOME BUYING

HOME BUYING

Most first-time buyers think they’ve saved a down payment. What they’ve actually saved is a down payment plus closing costs — and until they understand the difference, they’re planning with the wrong number. On a $500,000 home in Ontario with 5% down, you could easily have $8,000–$10,000 in closing costs due on or before possession day. That’s money that cannot come from your mortgage. It has to be there in cash.

This article breaks down every closing cost you’ll encounter in Canada, shows you what they look like in real dollar terms on a $500,000 purchase, and explains how to calculate what you can actually put toward your down payment once all of it is accounted for.

In This Article

- What closing costs actually are

- How much closing costs are in Canada

- Cost-by-cost breakdown

- Land transfer tax by province

- CMHC insurance: the hidden cost that doesn’t close

- Real numbers: $500,000 home, Ontario, 5% down

- Where to keep your closing cost savings

- The bottom line

- Frequently asked questions

What Closing Costs Actually Are

Closing costs are the one-time fees required to legally complete a real estate purchase in Canada. They’re separate from your down payment and separate from your ongoing mortgage payments. They’re due at or before closing — the date the property legally transfers into your name and you receive the keys.

The critical detail: closing costs cannot be rolled into your mortgage. Unlike your down payment, which determines your mortgage amount, closing costs must be paid from savings you have set aside specifically for this purpose. A lender will often ask for proof that you have enough cash to cover them.

The largest single closing cost for most Ontario buyers is land transfer tax. Outside Ontario, it varies significantly — buyers in Alberta pay almost nothing here, while buyers in Toronto pay double. The rest of the costs (legal fees, title insurance, home inspection, adjustments) are more consistent across the country.

How Much Closing Costs Are in Canada

The 1.5–4% range is a useful rule of thumb, but the actual figure depends heavily on where you’re buying. Ontario buyers — especially in Toronto — land at the higher end of this range because land transfer tax alone can exceed $6,000 on a $500,000 purchase. Alberta buyers, who pay no provincial land transfer tax, can land well under 2%.

Budget 3–4% of your purchase price for closing costs and consider anything left over a bonus. On a $500,000 purchase, that means having $15,000–$20,000 set aside for costs — separate from your down payment. This buffer protects you from the adjustments and surprise line items that appear on almost every Statement of Adjustments.

Cost-by-Cost Breakdown

Here’s what you can expect to pay, with typical ranges for a resale home purchase in Canada.

| Closing Cost | Typical Range | Notes |

|---|---|---|

| Land transfer tax | $0–$12,950+ | Varies dramatically by province; Ontario + Toronto buyers pay most |

| Legal fees | $1,200–$2,000 | Mandatory in Ontario and Alberta; covers title transfer, mortgage registration |

| Title insurance | $250–$800 | Usually bundled into legal fees; protects against title defects |

| Home inspection | $400–$600 | Optional but strongly recommended on resale homes |

| Property tax adjustment | $500–$2,500 | You reimburse the seller for taxes prepaid beyond closing date |

| Utility/condo fee adjustments | $200–$800 | Depends on condo vs. freehold and local utility prepayment |

| Moving costs | $1,000–$5,000 | Local vs. long-distance; time of year affects price significantly |

| Mortgage appraisal | $300–$500 | Sometimes covered by lender; ask upfront |

| Home insurance (first year) | $1,000–$2,000 | Lender requires proof of coverage before closing |

Legal Fees and Title Insurance

A real estate lawyer is mandatory in Ontario and Alberta, and strongly recommended everywhere else. Your lawyer handles the title search, registers the transfer, coordinates mortgage funds, and reviews the Statement of Adjustments — the final breakdown of every dollar owed at closing. Legal fees typically run $1,200–$2,000 and usually include title insurance, which protects you against issues like survey errors, title fraud, and zoning violations that weren’t caught in the title search.

Property Tax Adjustments

Property taxes are paid in advance in most of Canada. If the seller has already paid taxes for a period extending beyond the closing date, you reimburse them for that portion on closing. The amount depends on the property’s assessed value and how far into the tax year the closing falls. Your lawyer calculates this and it appears as a line item on your Statement of Adjustments — one of the costs that catches buyers off guard because it’s easy to forget.

Home Inspection

At $400–$600, a home inspection is one of the cheaper items on this list and one of the highest-value. It happens before the offer goes firm, not at closing, so it’s a cost you pay regardless of whether the deal proceeds. In competitive markets, some buyers waive inspection conditions to strengthen offers — a risk that occasionally results in expensive surprises post-closing. Budget for it regardless.

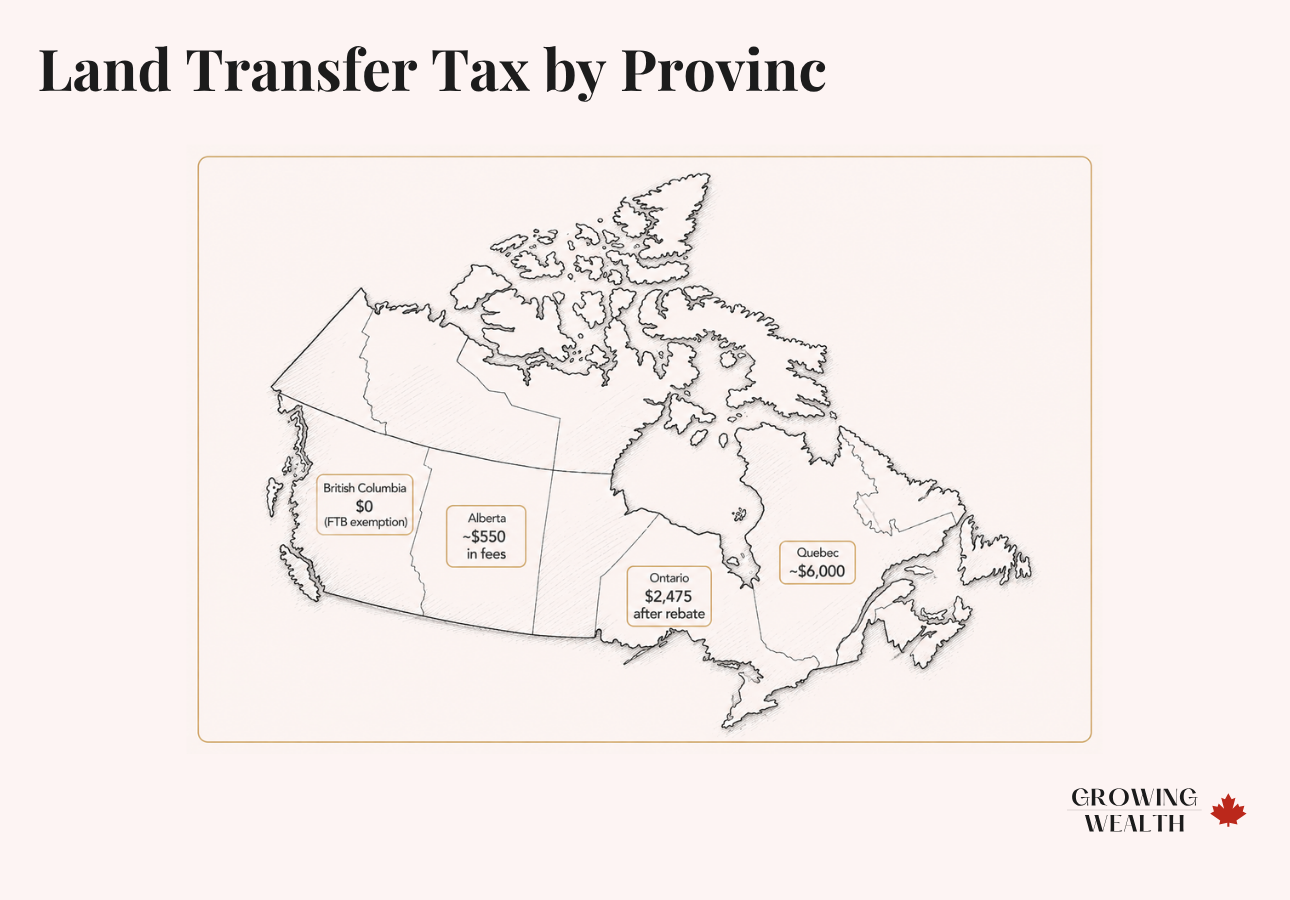

Land Transfer Tax by Province

Land transfer tax is the most variable closing cost in Canada. Where you buy matters as much as what you buy. Here’s what buyers in major provinces actually pay on a $500,000 purchase.

| Province | LTT on $500K | First-Time Buyer Rebate | Net Cost (FTB) |

|---|---|---|---|

| Ontario (outside Toronto) | $6,475 | Up to $4,000 | $2,475 |

| Toronto (Ontario + Municipal) | $12,950 | Up to $8,475 | $4,475 |

| British Columbia | $8,000 | Full exemption (homes ≤$500K) | $0 |

| Alberta | ~$500–$600 | None (land title fees only) | ~$500–$600 |

| Quebec | ~$5,500–$6,500 | None at provincial level | ~$5,500–$6,500 |

| Manitoba | ~$6,500 | Up to $4,500 | ~$2,000 |

Ontario First-Time Buyer LTT Rebate

Ontario’s provincial land transfer tax is calculated on a marginal bracket system. On a $500,000 purchase outside Toronto, the calculation works out to $6,475. First-time buyers qualify for a rebate of up to $4,000, which applies directly at closing — you don’t write a cheque and wait for a refund. The net cost for a first-time buyer in Ontario outside Toronto: $2,475.

Toronto buyers pay both the provincial land transfer tax and a city municipal land transfer tax, which mirrors provincial rates up to $2 million. On a $500,000 Toronto purchase, that’s $6,475 provincial plus $6,475 municipal, totalling $12,950 before rebates. First-time buyers in Toronto can claim up to $4,000 in provincial rebate and up to $4,475 in municipal rebate — a combined $8,475 — bringing the net cost to $4,475. Buying just outside the Toronto boundary (Mississauga, Brampton, Vaughan, Markham) means the municipal tax disappears entirely.

British Columbia

BC’s property transfer tax on a $500,000 home is $8,000. First-time buyers purchasing homes at $500,000 or under qualify for a full exemption — meaning zero property transfer tax. Homes between $500,001 and $835,000 qualify for a partial exemption. Above $835,000, no first-time buyer exemption applies. Given BC’s home prices, many buyers in the Lower Mainland won’t qualify for any rebate, making this a significant closing cost in that market.

Alberta

Alberta has no provincial land transfer tax. Buyers pay land title transfer fees instead, which are much lower — typically $500–$600 on a $500,000 purchase. This is a genuine financial advantage for Alberta buyers compared to Ontario or BC.

CMHC Insurance: The Hidden Cost That Doesn’t Close

CMHC mortgage default insurance deserves its own explanation because it’s commonly misunderstood. It is not a closing cost in the traditional sense — you don’t pay it as cash on possession day. Instead, the premium is added to your mortgage balance and paid down over your amortization period. But it is a real cost, and it significantly affects how much you end up borrowing.

CMHC insurance is mandatory if your down payment is less than 20%. The premium is calculated as a percentage of your mortgage amount, based on your loan-to-value ratio:

| Down Payment | Loan-to-Value | CMHC Premium | Premium on $500K Home |

|---|---|---|---|

| 5% | 95% | 4.00% | ~$19,000 |

| 10% | 90% | 3.10% | ~$13,950 |

| 15% | 85% | 2.80% | ~$11,900 |

| 20%+ | 80% or less | None | $0 |

On a $500,000 home with 5% down ($25,000), your mortgage is $475,000. The CMHC premium is 4.00% of $475,000, which equals approximately $19,000. That $19,000 is added to your mortgage balance — so you’re actually financing $494,000, not $475,000. The interest compounds over your entire amortization. It’s not a cash cost at closing, but it’s a real cost of buying with a small down payment.

In Ontario, Manitoba, and Quebec, provincial sales tax applies to the CMHC premium and must be paid at closing — in cash, not added to the mortgage. In Ontario the PST rate is 8%. On a $19,000 premium, that’s $1,520 due on closing day. Add this to your closing cost budget.

Real Numbers: $500,000 Home, Ontario, 5% Down

Here is what a first-time buyer’s closing costs actually look like on a $500,000 purchase in Ontario outside Toronto, with a 5% down payment ($25,000).

They’ve saved $33,000. They plan to put $25,000 toward the down payment (5%) and assumed the rest was safety margin. But closing costs will consume most of it.

| Cost Item | Estimated Amount |

|---|---|

| Down payment (5%) | $25,000 |

| Land transfer tax (after $4,000 FTB rebate) | $2,475 |

| Legal fees + title insurance | $1,600 |

| Home inspection | $500 |

| Property tax adjustment | $1,200 |

| PST on CMHC premium | $1,520 |

| Moving costs | $2,000 |

| Home insurance (first year) | $1,200 |

| Total cash needed | $35,495 |

Priya and Amir need $35,495 in total — but they only have $33,000 saved. They’re $2,495 short before even considering an emergency buffer. This is the scenario no one warns you about until you’re sitting with a real estate lawyer reviewing your Statement of Adjustments.

The actual down payment is not the issue here. The issue is that closing costs consumed their safety margin entirely. To put a clean 5% down and cover closing costs with a reasonable buffer, they needed closer to $38,000–$40,000 saved — not $33,000.

Decide on your down payment first. Then estimate your closing costs (use 3–4% of the purchase price as a conservative budget). Add them together — that is your total savings target. On a $500,000 purchase with 5% down: $25,000 (down payment) + $15,000–$20,000 (closing costs) = $40,000–$45,000 total savings needed before you’re ready to close.

There’s one more layer most buyers overlook: your emergency fund. Closing day is not the finish line for your savings — it’s actually when you need a financial cushion most.

A home comes with costs that don’t appear on any Statement of Adjustments. A furnace that needs replacing six months in. A roof repair. A hot water heater. These aren’t hypotheticals — they’re the reality of owning an older resale home, and they tend to arrive before you’ve had time to rebuild your savings after closing.

The standard advice is three to six months of living expenses kept in an accessible account at all times. Buying a home is no reason to drain it. If your plan requires zeroing out your savings to close, you’re not ready to close yet. Build the emergency fund into your total savings target alongside the down payment and closing costs — not as an afterthought. For a detailed breakdown of how much you actually need, read our guide to emergency funds in Canada.

Where to Keep Your Closing Cost Savings

Closing cost savings have one job: be there, in full, on possession day. That means you want an account that earns a competitive return without putting the money at risk, and that lets you access it without notice periods or penalties when the time comes.

A high-interest savings account (HISA) is the right tool here. It keeps your money liquid, earns interest on every dollar while you save, and is protected by CDIC insurance up to $100,000.

EQ Bank pays up to 2.75% on its Personal Account (as of May 2026) with no monthly fees, no minimum balance, and full CDIC protection. Your savings earn interest daily while you wait to close, and you can access them immediately when you need them — no lock-in, no withdrawal penalties. It works as a full chequing-savings hybrid, so you can set up direct deposit and automate transfers from your regular bank.

Open an EQ Bank account →One important note: once you have an accepted offer and a firm closing date, do not move your closing cost savings into a GIC or any account with a lock-in period. Keep the funds liquid and accessible. The timeline between accepted offer and closing is typically 30–90 days, but complications can arise, and you don’t want your cash tied up when your lawyer calls for funds.

For more on how to structure your savings accounts during the home buying process, read our guide to saving for a down payment using the FHSA and HBP.

The Bottom Line

Closing costs in Canada typically run 1.5–4% of your purchase price, and on a $500,000 home in Ontario, a first-time buyer should budget $8,000–$12,000 in addition to their down payment. Land transfer tax is the biggest variable — Ontario buyers pay $2,475 net after the first-time buyer rebate, while Toronto buyers pay $4,475, and Alberta buyers pay almost nothing. The rest of the costs (legal fees, title insurance, adjustments, moving) are fairly consistent across the country at $5,000–$7,000.

The planning mistake to avoid is treating every dollar you’ve saved as your down payment. Figure out your closing cost budget first, set it aside as untouchable, and only then count what remains as your actual down payment. And don’t close with your emergency fund at zero — a home comes with unexpected costs that don’t appear on any Statement of Adjustments. If you’re targeting 5% down on a $500,000 purchase in Ontario, a realistic total savings target is $45,000–$55,000 once you account for the down payment, closing costs, and a three-to-six-month emergency fund.

Keep your closing cost savings in a no-fee HISA that earns interest while you wait to close. You want that money liquid, growing, and accessible the moment your lawyer needs it.Ready to start building your home buying savings? Read How to Save for a Down Payment in Canada — a complete strategy using the FHSA and Home Buyers’ Plan to maximize every dollar you save toward your first home.

Frequently Asked Questions

Budget 3–4% of your purchase price as a conservative closing cost estimate. On a $500,000 home, that’s $15,000–$20,000 in cash that needs to be available on or before possession day, separate from your down payment. The actual amount will depend on your province (land transfer tax varies significantly), whether you qualify for first-time buyer rebates, and specific costs like moving and property tax adjustments.

No. Closing costs must be paid in cash. They cannot be rolled into your mortgage. Your lender will often ask for proof that you have sufficient funds to cover both the down payment and closing costs before approving your mortgage. The only exception is the CMHC insurance premium, which is added to your mortgage balance — but the provincial sales tax on that premium (in Ontario, Manitoba, and Quebec) must still be paid in cash at closing.

Land transfer tax is a provincial tax paid by the buyer when a property changes hands. It’s calculated as a percentage of the purchase price using a marginal bracket system — meaning different portions of the price are taxed at different rates. In Ontario, the tax on a $500,000 purchase works out to $6,475. Toronto buyers pay an additional municipal tax of the same amount, totalling $12,950. Alberta and Saskatchewan have no provincial land transfer tax, making them significantly cheaper to close in than Ontario or BC.

Yes, in several ways. Ontario first-time buyers receive up to $4,000 off their provincial land transfer tax, and Toronto first-time buyers get an additional $4,475 off the municipal tax. BC first-time buyers purchasing a home at $500,000 or under pay zero property transfer tax. Federally, first-time buyers are also eligible for the Home Buyers’ Amount, a $10,000 non-refundable tax credit that provides up to $1,500 in federal tax relief on your next return — not cash at closing, but real savings nonetheless.

Not in the traditional sense. The CMHC premium itself is added to your mortgage balance, not paid in cash at closing. However, if you’re buying in Ontario, Manitoba, or Quebec, the provincial sales tax on the premium is due at closing in cash. In Ontario, that’s 8% of the premium. On a $500,000 purchase with 5% down, the CMHC premium is approximately $19,000, and the Ontario PST on that is $1,520 — cash due on possession day.

A Statement of Adjustments is the final financial summary your lawyer prepares before closing. It shows every amount owed and every credit you’re receiving, including the purchase price, your deposit, the mortgage funds coming from your lender, and all the adjustments for property taxes, utility deposits, condo fees, and other items prepaid by the seller. The bottom line tells you exactly how much cash you need to bring to your lawyer’s office. Review it carefully — errors can and do occur.

A home inspection is not a closing cost in the technical sense — it’s paid before your offer goes firm, typically during the conditional period. It typically costs $400–$600. You pay it regardless of whether the deal proceeds (if the inspection reveals problems and you walk away, you’ve still paid). In competitive markets where buyers waive conditions, many skip the inspection to strengthen their offer. This is a risk decision, but budgeting for an inspection is always wise even if you ultimately don’t use one.

For a $500,000 home in Ontario with 5% down, a realistic total savings target is $45,000–$55,000. That breaks down as: $25,000 for the down payment, $8,000–$12,000 for closing costs (land transfer tax after rebate, legal fees, adjustments, moving, insurance), and a separate emergency fund of three to six months of living expenses — typically $12,000–$18,000 for most Ontario households. Closing with your emergency fund drained means the first unexpected home repair becomes a financial crisis.