Registered Accounts

Registered Accounts

If you’ve ever Googled “should I open an FHSA or TFSA or RRSP” and ended up more confused than when you started — you’re not alone.

These three accounts are all designed to help you build wealth. They all offer tax advantages. And they all have acronyms that blur together after about five minutes of reading.

But here’s the truth: they’re not competing with each other. They serve different purposes. And once you understand what each one is actually for, the decision gets a lot simpler.

This guide breaks it all down in plain language — with a real family example, a side-by-side comparison, and a clear decision guide so you know exactly where to put your money first.

This article contains affiliate links. We may earn a commission if you open an account — at no cost to you. We only recommend products we’ve researched and trust.

In This Article

The Quick Version (If You’re Short on Time)

- FHSA — Save for your first home. Tax-free going in, tax-free coming out. Use it if you plan to buy within the next 15 years.

- TFSA — The most flexible account. Save for anything. No tax on growth or withdrawals, ever.

- RRSP — Retirement savings. Big tax deduction now, taxed when you withdraw in retirement. Best when your income is high today and lower in retirement.

Most Canadian families should be using all three — just in a specific order depending on your situation.

What Is Each Account, Really?

FHSA (First Home Savings Account)

The FHSA launched in 2023 and it’s one of the best financial tools the federal government has ever introduced for young Canadians — and most people still don’t fully understand it.

Here’s why it’s so powerful: contributions are tax-deductible (like an RRSP), and qualifying withdrawals for your first home purchase are completely tax-free (like a TFSA). You get the best of both worlds.

- You can carry forward up to $8,000 in unused contribution room (one year only)

- Must be a Canadian resident and a first-time home buyer to open one

- Funds must be used to buy a qualifying first home, or transferred to an RRSP/RRIF

- Account can stay open for 15 years or until age 71, whichever comes first

For more on how it works in detail, see the CRA’s official FHSA page or our full FHSA Canada Guide.

TFSA (Tax-Free Savings Account)

The TFSA is the most flexible registered account available to Canadians — and the most misunderstood. Despite the name, it’s not just a savings account. You can hold stocks, ETFs, GICs, mutual funds, and more inside a TFSA.

The key feature: your money grows completely tax-free, and you can withdraw at any time for any reason with zero tax owing.

- Withdrawals add the contribution room back the following calendar year

- No impact on government benefits (OAS, GIS, etc.)

- Available to any Canadian resident 18 or older

For a full breakdown of how to use it, see our TFSA Canada Guide.

RRSP (Registered Retirement Savings Plan)

The RRSP is the classic retirement account. You get a tax deduction when you contribute, your money grows tax-deferred, and you pay tax when you withdraw — ideally in retirement when your income (and tax rate) is lower.

- Unused contribution room carries forward indefinitely

- Withdrawals are taxed as income in the year you take them

- Special exception: Home Buyers’ Plan (HBP) lets you withdraw up to $35,000 tax-free for a first home purchase — but you have to pay it back within 15 years

You can verify current RRSP and TFSA contribution room on the CRA’s official limits page. For a deeper look at how RRSPs work, see our RRSP Canada Guide.

Side-by-Side Comparison

| Feature | FHSA | TFSA | RRSP |

|---|---|---|---|

| Annual limit | $8,000 | $7,000 | 18% of income (max $31,560) |

| Lifetime limit | $40,000 | No limit (room accumulates) | No lifetime cap |

| Tax deduction on contributions? | ✓ Yes | ✗ No | ✓ Yes |

| Tax on growth? | ✗ None | ✗ None | ✗ None (deferred) |

| Tax on withdrawals? | ✗ None (qualifying) | ✗ None | ✓ Yes — taxed as income |

| Withdrawal flexibility | First home purchase only | Anytime, any reason | Anytime (tax applies) |

| Room restored after withdrawal? | ✗ No | ✓ Yes (next year) | ✗ No |

| Best for | Buying a first home | Anything flexible | Retirement savings |

| Age limit | Must close by 71 or 15 years | No age limit to contribute | Must convert by 71 |

A Real Family Example

Meet Sarah and Marcus. They live in Ontario, earn a combined $110,000/year, have two kids (ages 3 and 6), and are currently renting. They want to buy a home in the next 4 years and also start investing for retirement.

They have $1,500/month to put toward savings and investments. Here’s how they’d use the three accounts:

They each open an FHSA and contribute $8,000/year each ($667/month each). That’s $16,000/year combined going toward their down payment — fully tax-deductible, and it will come out tax-free when they buy. At their combined income, the tax deduction alone saves them roughly $4,000–$5,000 per year back at tax time.

The remaining $167/month goes into their TFSAs as a flexible emergency/opportunity fund. No tax, no rules, and if they need it for something unexpected, they can access it without penalty.

Right now, Sarah and Marcus’s priority is the home. Once they buy and their cash flow stabilizes, they’ll shift toward maxing their RRSPs — especially as their income grows and the tax deduction becomes more valuable.

Over 4 years, the FHSAs alone could accumulate roughly $64,000–$68,000 (contributions + modest investment growth), giving Sarah and Marcus a solid down payment foundation without touching their savings account.

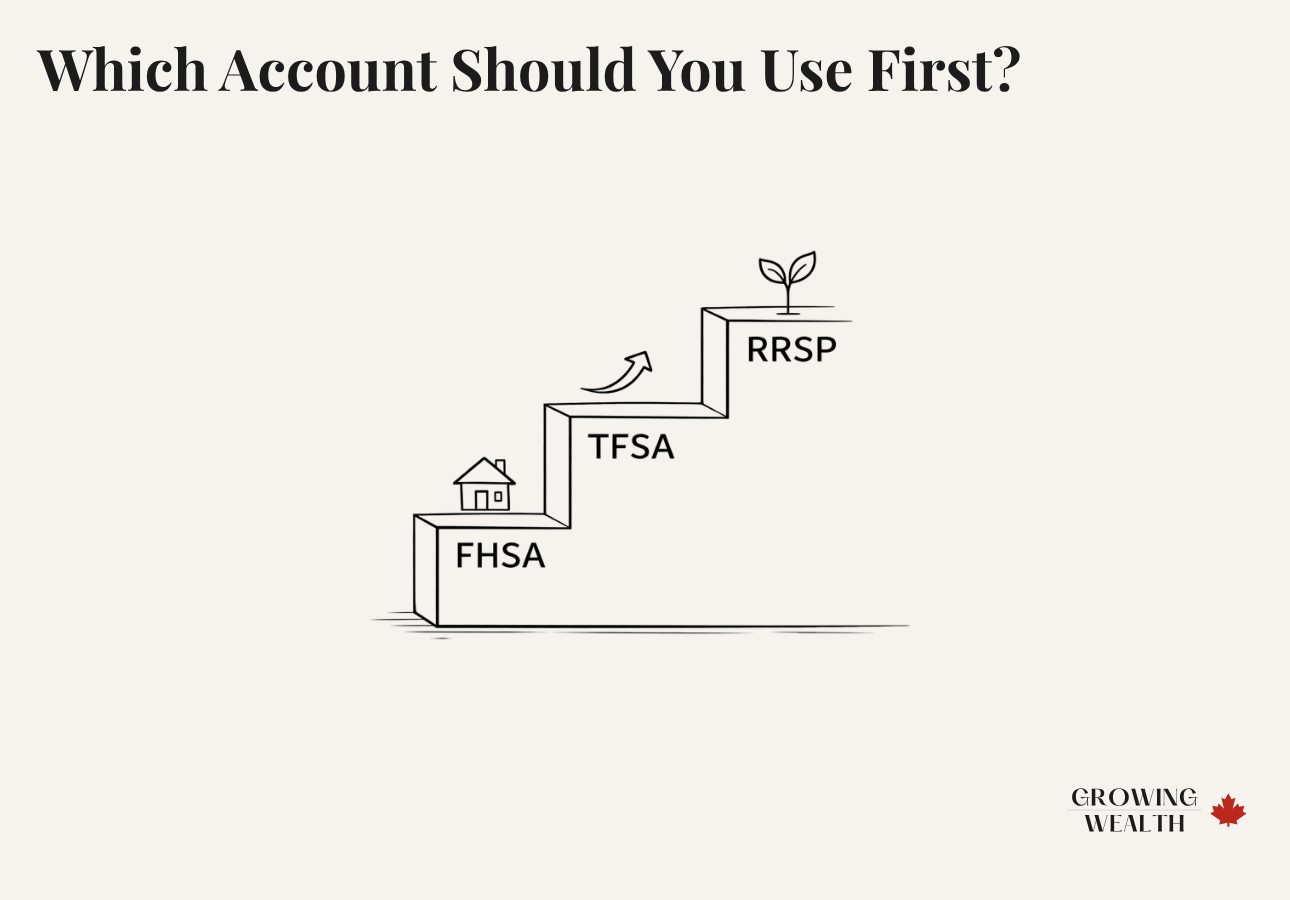

Which Account Should You Use First?

The right order depends on your situation. Here’s a simple framework:

Start with the FHSA. It’s the only account that gives you a tax deduction and tax-free withdrawals. If you qualify, there’s almost no reason not to open one immediately — even if you can only contribute a small amount each year. The contribution room doesn’t accumulate endlessly (only one year of carry-forward), so waiting costs you.

TFSA first. It’s the most flexible account and has no strings attached. Use it for short-term goals, an emergency fund, or long-term investing. You can’t go wrong here.

The tax deduction is most valuable when you’re in a higher bracket. Contributing $10,000 to an RRSP at a 43% marginal rate saves you $4,300 in taxes that year. That’s money working twice.

It often makes more sense to use the TFSA now and save your RRSP contribution room for when your tax rate is higher. The deduction is worth more at 40% than at 20%.

Use the FHSA if you’re eligible. Use the TFSA for flexibility. Use the RRSP when your income justifies the deduction. And don’t let perfect be the enemy of good — contributing anything to any of these accounts is better than leaving money in a regular bank account.

For a deeper comparison of TFSA and RRSP specifically, see RRSP vs TFSA: Which Is Better for You?

Can You Use All Three at the Same Time?

Yes — and most financial advisors would say you should, eventually.

There’s no rule against having all three open simultaneously. The question is just about prioritization when your cash flow is limited.

A common approach for growing families:

| Life Stage | Priority Account | Why |

|---|---|---|

| Renting, planning to buy | FHSA → TFSA | Maximize the home purchase advantage while keeping flexibility |

| Just bought your first home | TFSA → RRSP | FHSA funds used up; shift to long-term wealth building |

| Income growing in 30s/40s | RRSP → TFSA | RRSP deduction most valuable at peak earning years |

| Approaching retirement | RRSP → TFSA drawdown | Draw from RRSP strategically; TFSA stays tax-free |

For help thinking through how all of this fits into your family’s overall financial system, see our Family Finance System for Canadians.

What About the Home Buyers’ Plan (HBP)?

The Home Buyers’ Plan lets you withdraw up to $35,000 from your RRSP tax-free to buy your first home — but you have to repay it within 15 years.

So should you use the HBP or the FHSA?

| Situation | Better Option |

|---|---|

| Starting from scratch, first-time buyer | FHSA — no repayment required |

| Already have years of RRSP contributions built up | HBP may complement the FHSA |

| Need more than $40,000 for your down payment | Use both FHSA + HBP together |

| Concerned about repayment discipline | FHSA — no payback obligation |

FHSA withdrawals don’t need to be repaid. HBP withdrawals do — and if you miss payments, they’re added to your income that year. If you’re starting from scratch today, open the FHSA first.

How to Start Investing Inside These Accounts

Opening the account is step one. But these accounts are just containers — what you put inside them matters just as much.

| Time Horizon | Suggested Approach |

|---|---|

| Short-term (buying in 1–3 years) | GICs or high-interest savings inside the account — lower risk, predictable return |

| Medium-term (buying in 4–7 years) | Balanced ETF portfolio — some growth, some stability |

| Long-term (retirement, 10+ years) | Low-cost index ETFs — maximize growth over time |

See our beginner’s guide on How to Start Investing in Canada for a full breakdown of what to actually hold inside these accounts.

And don’t forget: before investing, make sure you have a solid Emergency Fund in place. No registered account should be your first stop in a financial crisis.

The Bottom Line

The FHSA, TFSA, and RRSP aren’t competing — they’re complementary. Each one does something the others don’t.

If you’re a Canadian family renting right now and planning to buy: open an FHSA today. Every month you wait is contribution room you can’t fully get back.

If you want flexibility and simplicity: the TFSA is your best friend.

And as your income grows and retirement becomes a real thing you think about: the RRSP will earn its place in your financial plan.

You don’t have to do everything at once. Start with one account, understand it, and build from there. The fact that you’re thinking about this at all puts you ahead of most people.Want to turn what you’ve just learned into lasting results? Read A Simple Family Finance System for Canadians — a practical framework that shows exactly where your money should go each month.

Frequently Asked Questions

Yes. There’s no rule preventing you from having an FHSA, TFSA, and RRSP open simultaneously. Most Canadians will benefit from all three at different stages of life.

You can transfer the funds to your RRSP or RRIF without affecting your RRSP contribution room. You won’t lose the money — you just lose the tax-free withdrawal benefit specifically for a home purchase.

No. FHSA contributions do not reduce your RRSP contribution room. They’re completely separate.

Yes — as long as both are first-time home buyers. A couple could each open an FHSA and contribute up to $8,000/year each, for a combined $16,000/year toward a tax-advantaged down payment.

A regular savings account is taxed — any interest you earn is reported as income. A TFSA is not taxed, ever. The name is misleading because you can hold investments (not just savings) inside a TFSA too.

No. To open an FHSA, you must be a first-time home buyer — meaning you haven’t owned a qualifying home that you lived in as your principal residence at any point during the current calendar year or the preceding four years.

Generally, TFSA first. If you’re in a low tax bracket today but expect to earn more in the future, it’s smarter to save your RRSP contribution room and use it when the deduction is worth more. The TFSA is always a safe bet.

There’s no universal answer — it depends on your income, goals, and expenses. A good starting point: contribute enough to your FHSA to maximize it ($8,000/year = $667/month), then direct whatever’s left to your TFSA. Once your income grows, layer in RRSP contributions.