By:

Growing Wealth

Published:

Most Canadians misunderstand the TFSA.

They treat it like a savings account. A place to park cash. Something “safe.”

That’s not what it’s for.

A Tax-Free Savings Account is one of the most powerful tools available to Canadian families—not because it’s safe, but because everything that grows inside it is never taxed again.

The Canadian government makes it clear that a TFSA allows your investments to grow completely tax-free—including interest, dividends, and capital gains. According to the official guidance from the Government of Canada, any income earned inside a TFSA is not taxed, even when withdrawn.

Used properly, your TFSA can compound into a six-figure (or higher) tax-free portfolio.

Used poorly, it barely keeps up with inflation.

If you’re still building your foundation, start with how to start investing in Canada.

Quick Answer: What Should You Hold in a TFSA?

The best investments to hold in a TFSA in Canada are high-growth assets like ETFs and global stocks, not low-return options like savings accounts or GICs. Your TFSA should be used for long-term tax-free growth, not short-term cash.

The Core Rule: Use Your TFSA for Growth

Don’t waste your TFSA room on low-return investments.

Your TFSA eliminates tax on capital gains, dividends, and withdrawals. That’s what makes it so powerful—especially when paired with long-term growth.

Historically, equity markets have returned roughly 7–10% annually over the long term, while savings accounts typically sit closer to 2–4%. That gap compounds over time—and the TFSA lets you keep all of it.

That’s why your TFSA should be your growth engine, not your safety bucket.

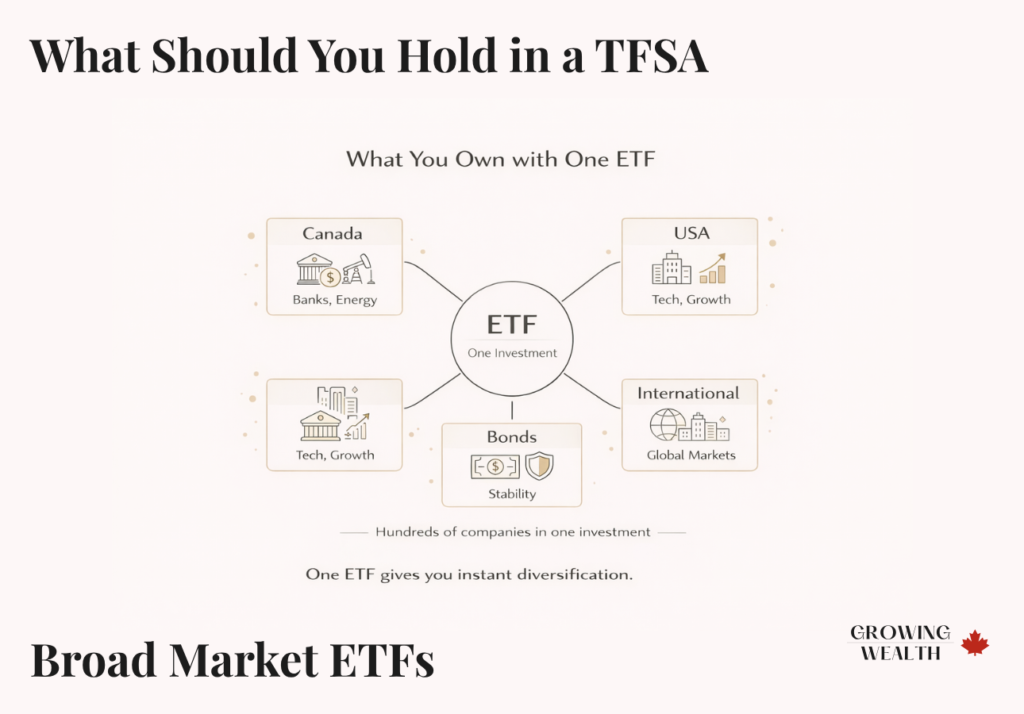

Broad Market ETFs (Your Default Choice)

If you’re asking what should I put in my TFSA, this is your answer.

Broad market ETFs give you diversification, low fees, and long-term growth—all in a single investment. Instead of trying to pick individual winners, you own the market.

For most Canadian families, this is the simplest and most effective TFSA strategy.

If you want a straightforward way to get started:

👉 Open an account with Wealthsimple

This allows you to invest in diversified ETF portfolios with minimal setup and ongoing management.

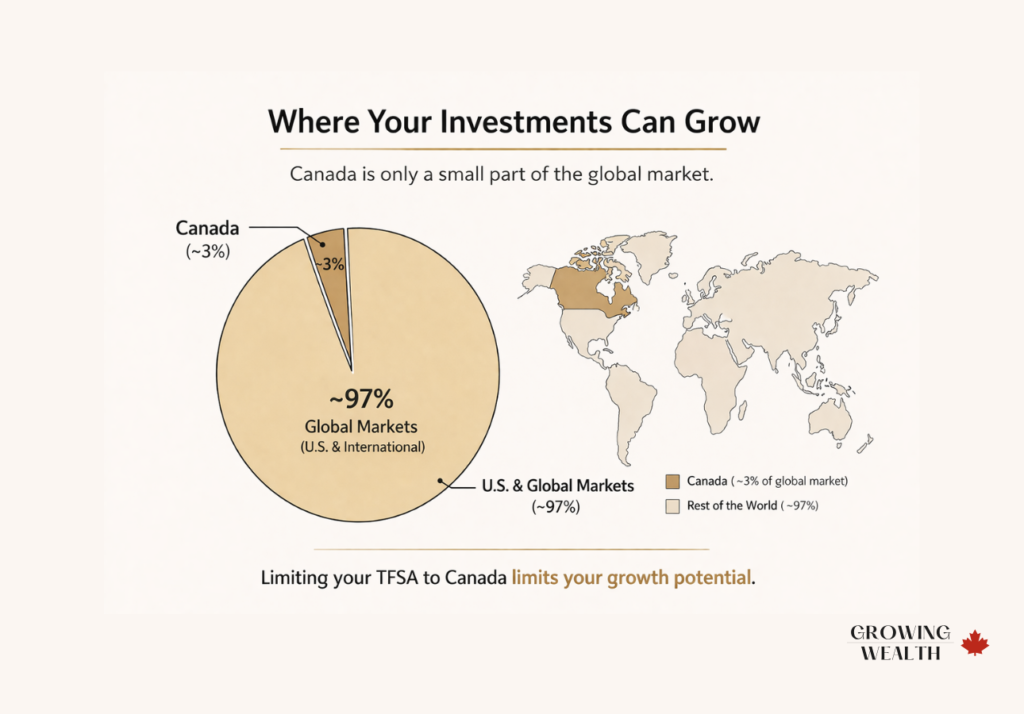

U.S. and Global Equity Exposure

Canada makes up a small portion of the global market.

If your TFSA is heavily concentrated in Canada, you’re limiting your long-term potential.

A stronger approach includes exposure to:

- U.S. markets

- International developed markets

- Some emerging markets

This gives you access to global growth, innovation, and a broader range of industries.

You may hear about U.S. dividend withholding tax inside a TFSA. It exists—but it’s relatively small and shouldn’t override your investment strategy.

Growth matters more.

Individual Stocks (Use Carefully)

Holding individual stocks in a TFSA can be powerful—but it’s not where most people should focus.

If a stock performs well, all gains are tax-free. That’s the upside.

The downside is often ignored.

If your investment drops significantly, that loss permanently reduces your TFSA contribution room. You don’t get it back.

For that reason, individual stocks should be used carefully and kept as a smaller portion of your overall TFSA.

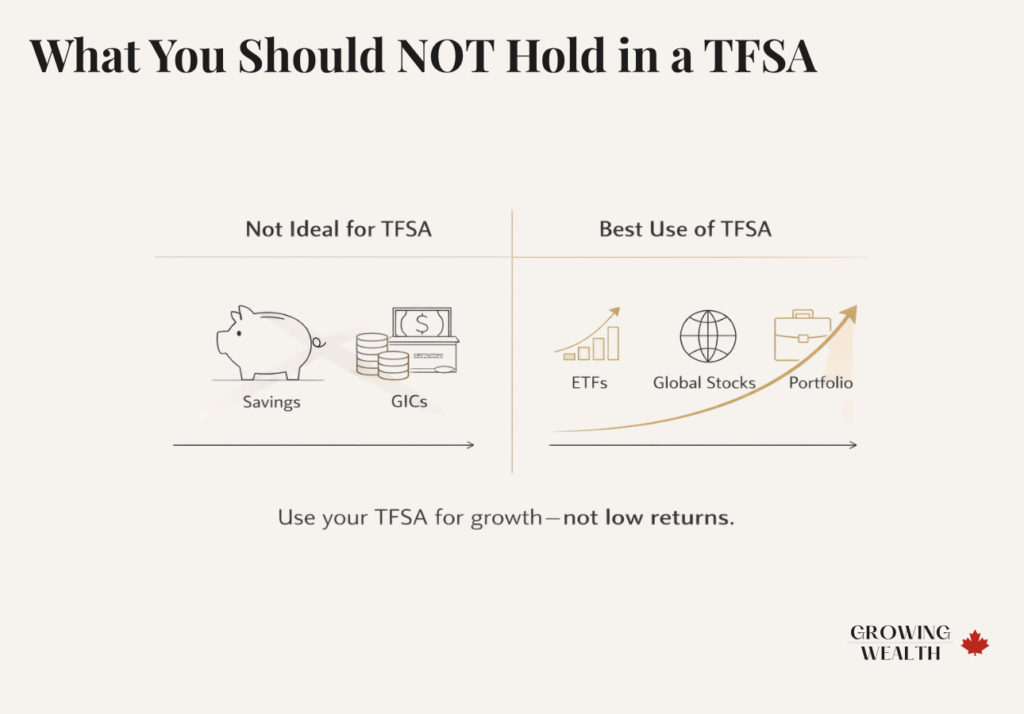

What You Should NOT Hold in a TFSA

High-Interest Savings Accounts

This is the most common mistake.

Using your TFSA as a savings account feels safe—but it limits what the account can actually do for you.

Savings accounts generate relatively low returns, which means you’re using tax-free space for minimal growth.

If your goal is to earn interest on short-term cash, it’s better to keep that outside your TFSA.

If you’re comparing options, see high-interest savings accounts in Canada.:

Or use a dedicated account like:

👉 Open an EQ Bank account

This keeps your TFSA available for higher-growth investments.

There are exceptions. A TFSA can still make sense for:

- Emergency funds (see emergency fund Canada guide)

- Short-term savings goals (1–2 years)

But beyond that, it’s not the best use.

GICs

GICs offer fixed returns and capital protection—but they also limit your upside.

Inside a TFSA, that creates opportunity cost. You’re using valuable tax-free space for investments that don’t grow much over time.

GICs can still serve a purpose for short-term needs, but they shouldn’t be the core of your TFSA.

Overly Conservative Portfolios

If your TFSA is heavily weighted toward bonds, cash, or low-risk funds, you’re underusing it.

The TFSA works best when paired with time and growth.

That doesn’t mean taking unnecessary risk—it means aligning your investments with a long-term horizon.

Why Using Your TFSA for Savings Feels Right (But Isn’t)

Part of the confusion comes from the name.

“Tax-Free Savings Account” makes it sound like a place for cash.

It’s not.

Banks also reinforce this by promoting TFSAs as savings products, which leads many people to default to low-return options.

Psychologically, it feels safer.

But financially, it’s inefficient.

The TFSA isn’t about protecting money—it’s about growing it efficiently.

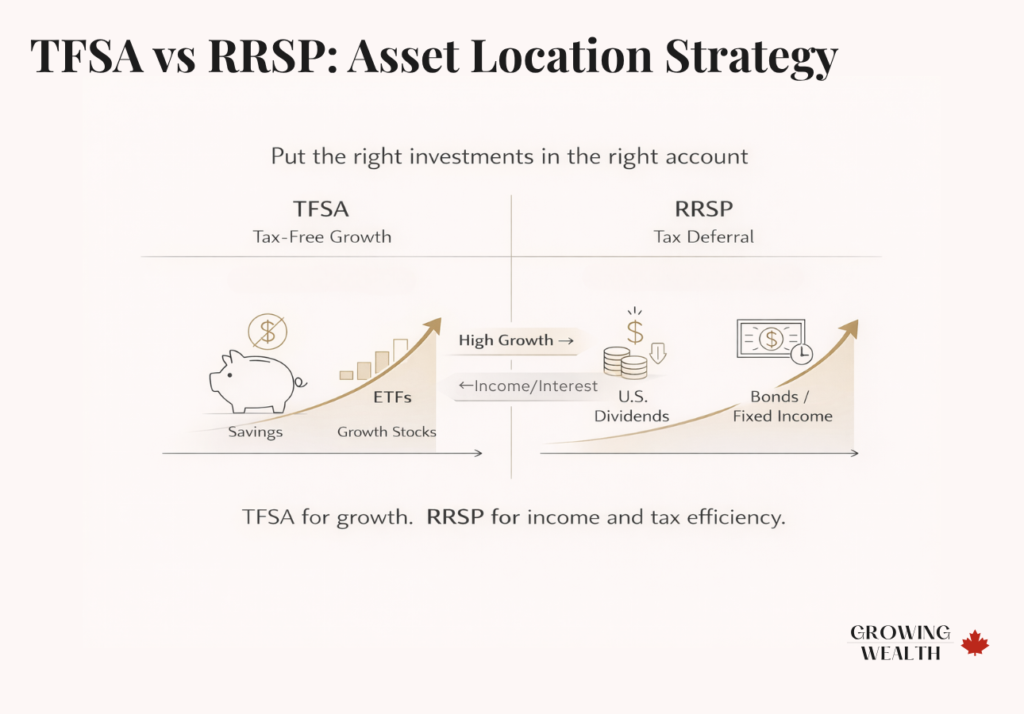

TFSA vs RRSP: Asset Location Strategy

Not all investments belong in the same account.

| Investment Type | Best Account |

|---|---|

| High-growth ETFs | TFSA |

| U.S. dividend stocks | RRSP |

| Bonds / fixed income | RRSP |

| Short-term savings | TFSA or HISA |

The TFSA is best used for tax-free growth, while the RRSP is better suited for tax-deferred income and specific tax efficiencies.

For a full breakdown of which investments work best on the RRSP side of that equation, see our guide on what to hold in your RRSP.

If you’re deciding how to balance both, read RRSP vs TFSA in Canada.

If you’re also eligible for an FHSA, it changes the equation — our FHSA vs TFSA vs RRSP comparison shows where it fits alongside both accounts.

Where Your TFSA Fits in a Family Finance System

Your TFSA doesn’t exist in isolation.

It’s one part of a broader system.

A strong setup typically includes:

- An emergency fund for unexpected expenses

- A high-interest savings account for short-term goals

- A TFSA for long-term investing

- An RRSP for retirement optimization

The mistake most families make is mixing these roles.

They use their TFSA for short-term savings and conservative investments, which weakens its effectiveness.

Each account should have a clear purpose.

To see how this fits together, revisit A Simple Family Finance System for Canadians.

TFSA Growth vs Savings: Real 10-Year Comparison

Here’s what happens when you use your TFSA differently.

Assumptions:

- Starting amount: $10,000

- Time horizon: 10 years

- Tax rate: 30%

| Scenario | Annual Return | Final Value (TFSA) | Tax Owed Outside TFSA | After-Tax Value (Non-TFSA) |

|---|---|---|---|---|

| Savings Account | 3% | $13,439 | ~$1,031 | ~$12,408 |

| Growth Investment | 8% | $21,589 | ~$1,738 | ~$19,851 |

What This Shows

Using your TFSA for savings saves some tax—but produces limited growth.

Using it for growth:

- Saves more tax

- Produces significantly higher returns

The difference is over $8,000 on just $10,000 in 10 years.

Over longer periods, that gap becomes much larger.

A Simple TFSA Portfolio (That Actually Works)

You don’t need complexity.

You need consistency.

A simple structure is often enough: a global equity ETF as your core holding, optionally paired with a small allocation to bonds if you need stability.

This gives you diversification, growth, and simplicity without constant management.

Where Lump Sum vs DCA Fits In

Once you know what to hold, the next decision is how to invest your contributions.

You can invest all at once or spread it out over time.

If you’re unsure which approach fits your situation, compare both strategies in lump sum vs dollar-cost averaging in Canada.

The best approach is the one you can stick with consistently.

Common TFSA Mistakes

The biggest issues aren’t complicated—they’re behavioural.

Using the TFSA as a savings account limits growth. Being too conservative reduces compounding. Overtrading increases risk and often leads to worse outcomes. Thinking short-term prevents the account from doing what it’s designed to do.

All of these mistakes reduce long-term results.

Final Take

The TFSA is not just another account.

It’s one of the few places in Canada where your investments can grow completely tax-free.

Most people underuse it by focusing on safety instead of growth.

That decision has long-term consequences.

Put your best long-term investments in your TFSA—not your safest ones.

Frequently Asked Questions

What should I hold in a TFSA in Canada?

High-growth investments like ETFs and global equities are typically the best choice because they benefit most from tax-free compounding.

Are savings accounts good for a TFSA?

They can be useful for short-term savings or emergency funds, but they are not ideal for long-term investing.

Should I invest in U.S. stocks in a TFSA?

Yes. While there is a small withholding tax on dividends, the growth potential generally outweighs the cost.

Can I lose money in a TFSA?

Yes. Losses are possible, and they permanently reduce your contribution room, which is why investment choices matter.

Is TFSA better than RRSP?

It depends on your income and goals. TFSAs offer flexibility and tax-free growth, while RRSPs provide tax deferral and are often more beneficial at higher income levels.

How should I start investing in a TFSA?

Start with a diversified ETF portfolio and contribute consistently. If you need guidance, review how to start investing in Canada.

Affiliate Disclosure

💡 GrowingWealth.ca is supported by readers. Some of the links in this article are affiliate links, which means we may earn a small commission if you open an account or make a purchase — at no extra cost to you. We only recommend products and services we personally use, trust, or believe provide genuine value to Canadians. Our reviews and comparisons are always independent and objective.