By:

Growing Wealth

Published:

Most Canadians don’t struggle with how to invest.

They get stuck on one question:

How much should I actually be investing each month?

The advice you’ll usually find is either too vague (“invest what you can”) or unrealistic (“save 30% of your income”). Neither helps you make a real decision.

This guide gives you clear monthly targets, realistic starting points, and a system you can actually follow, based on income, financial stage, and real-life constraints.

How much should you invest each month in Canada?

Most Canadians should invest 10–20% of their income monthly, starting at 5–10% if cash flow is tight. A practical starting point is $250–$500 per month, increasing over time.

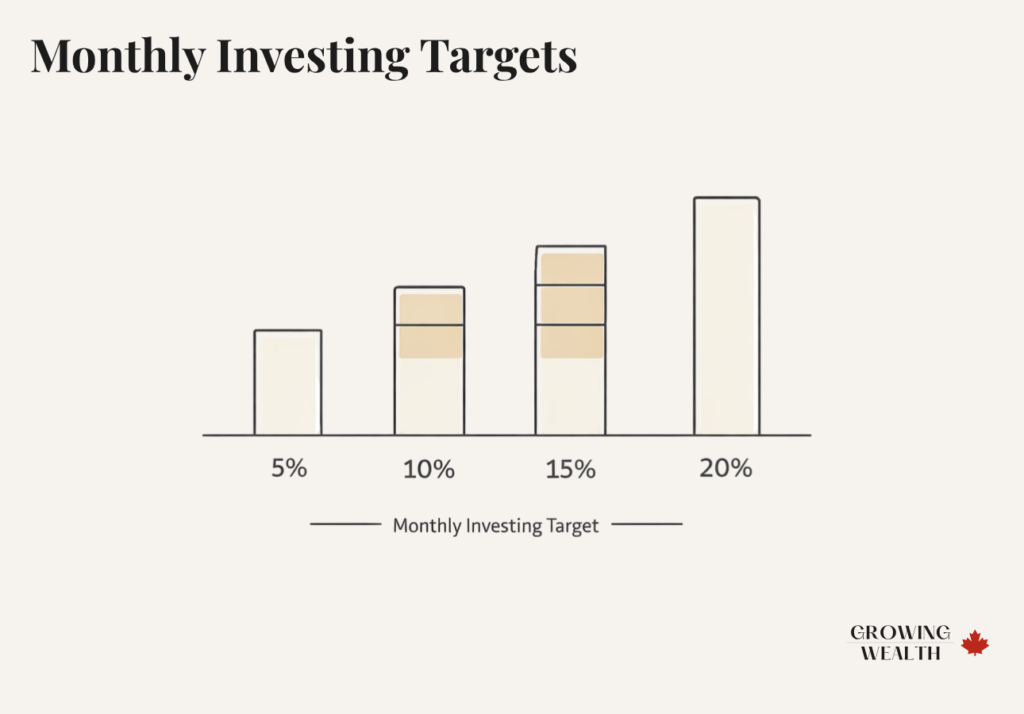

Monthly Investing Targets (Quick Reference)

- Starter: $100–$250/month

- Solid: $250–$500/month

- Strong: $500–$1,000/month

- Target: 10–20% of income

Monthly Investment Targets by Income

| Monthly Income | 5% | 10% | 15% | 20% |

|---|---|---|---|---|

| $4,000 | $200 | $400 | $600 | $800 |

| $6,000 | $300 | $600 | $900 | $1,200 |

| $8,000 | $400 | $800 | $1,200 | $1,600 |

These are long-term targets—not where most people should start.

Why Most People Get This Wrong

This isn’t an information problem. It’s an execution problem.

People tend to start too aggressively, avoid automating, or delay investing altogether because they feel unsure. In practice, a smaller amount you maintain consistently will outperform a higher amount you abandon after a few months.

Step 1: Build Your Financial Base First

Before increasing your investments, your foundation needs to be stable.

That includes having an emergency fund, controlling high-interest debt, and maintaining consistent monthly cash flow. If you’re unsure how much to keep in cash, this breakdown in Emergency Fund: How Much You Really Need walks through exact numbers.

Equally important is having a system that ensures your money is actually going where it should. If your finances feel disorganized, the structure outlined in A Simple Family Finance System for Canadians is a better starting point than increasing your investment rate.

Skipping this step is one of the main reasons people stop investing the first time something unexpected happens.

Step 2: Start Small and Make It Automatic

You don’t need to invest a large amount to begin—you need to make it consistent.

For most people, that looks like starting with $100, $250, or $500 per month depending on what your budget can support. The platform you choose matters less than getting started—this is where most people get stuck, not because it’s complex, but because they delay the decision.

Automation is what makes this work. Once your contributions are set up, investing continues without relying on motivation or timing.

If you haven’t set this up yet, this step-by-step guide on how to start investing in Canada walks you through opening your account and automating your first contribution.

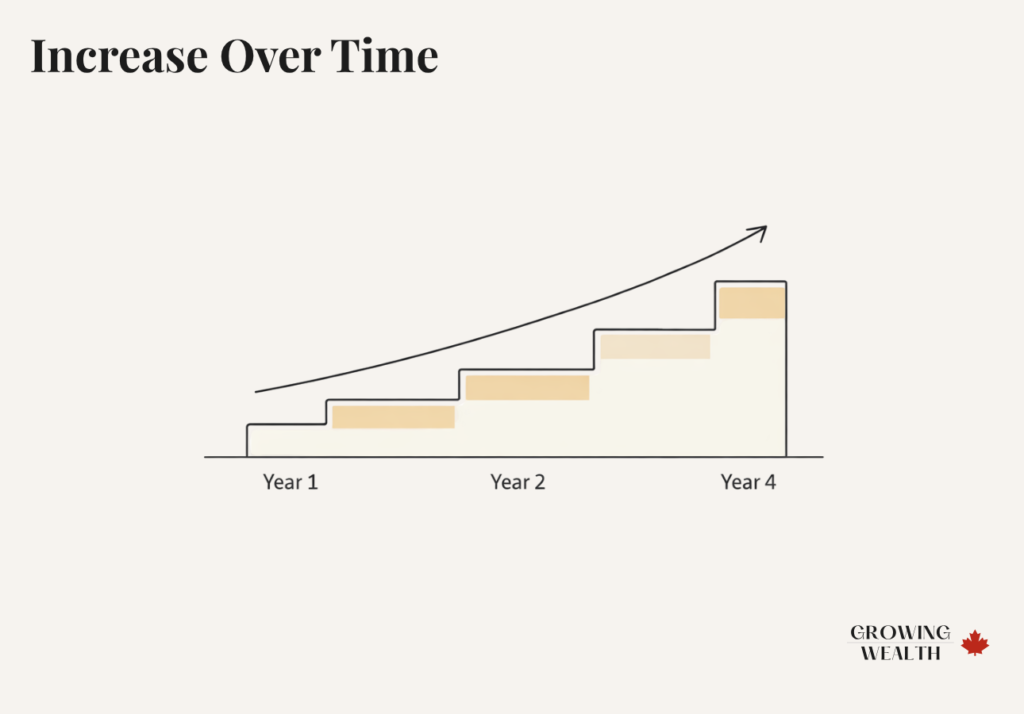

Step 3: Increase Over Time (This Is Where Results Come From)

Most people assume they need to start at 15% or higher. That’s not how it works in practice.

A more effective approach is to start lower and increase gradually as your income and financial stability improve.

Example Progression

| Year | Contribution Rate |

|---|---|

| Year 1 | 8% |

| Year 2 | 12% |

| Year 3 | 15% |

| Year 4 | 18% |

This aligns with how real life works. Your income increases, your expenses stabilize, and your ability to invest grows with it.

Once you’ve set your monthly amount, the next decision is what to invest in—this guide on what you should actually invest in breaks that down simply.

Real Scenarios: What You Should Invest

Tight Cash Flow

If you’re earning around $4,000/month and expenses are tight, pushing too hard will usually backfire. A realistic starting point is 5–8% ($200–$320/month).

Moderate / Stable Income

At $6,000/month with controlled expenses, a contribution rate of 10–15% ($600–$900/month) is both realistic and effective.

High Income, Strong Control

At $8,000+/month with low debt and structured finances, investing becomes your primary wealth-building tool. A contribution range of 15–25%+ ($1,200–$2,000+/month) is appropriate here.

Where Should You Invest This Money?

Once you know how much to invest, the next step is deciding where it should go.

At a high level, the TFSA vs RRSP decision comes down to flexibility versus tax reduction. A TFSA gives you tax-free growth and access to your money, while an RRSP reduces your taxable income and is designed for long-term retirement.

For a deeper understanding of how RRSPs work in Canada, this guide on RRSPs in Canada covers contribution rules and strategy.

If you’re also saving for a first home, the FHSA should be part of this decision — see our FHSA vs TFSA vs RRSP comparison to understand which account to prioritize.

If you want the official limits and rules, refer to the CRA TFSA page and the CRA RRSP page.

Why Most People Never Start Investing

Most people don’t avoid investing because it’s complicated.

They avoid it because they:

- Don’t want to choose the wrong platform

- Feel like they don’t have enough money

- Keep waiting for a better time

That hesitation is what delays progress—not a lack of information.

Choosing an Investing Platform (Where This Becomes Real)

This is where most people hesitate—not because it’s complicated, but because they don’t want to choose incorrectly.

In reality, you don’t need the perfect platform. You need one that is simple enough to use consistently. What matters is choosing one and getting your first contribution set up.

If you’re unsure which option fits your situation, this breakdown of Wealthsimple vs Questrade walks through the differences clearly and helps you decide.

Ready to Start Investing?

If you want the simplest way to start:

👉 Open a Wealthsimple account and set up automatic investing

👉 Or use Questrade if you prefer more control and lower fees

Start with one. You can optimize later.

Monthly vs Lump Sum Investing

If you’re investing monthly, you’re using dollar-cost averaging—investing consistently regardless of market conditions.

If you invest a larger amount at once, such as a bonus or tax refund, that’s lump sum investing.

Both approaches work, but consistency matters more than timing. This comparison of lump sum vs dollar-cost averaging explains when each approach makes sense.

The Biggest Mistake: Waiting Too Long

Most people delay investing because they think they need more income, a better plan, or better timing.

That delay costs years of compounding.

Investing $500 per month consistently can grow into a substantial portfolio over time—the key is starting early and increasing gradually.

A Simple Monthly Investing System

If you want something clear and actionable:

- Start with $250–$500/month

- Open a TFSA or RRSP

- Choose a platform and automate contributions

- Increase contributions every 3–6 months

- Work toward 15%+ long term

Still Not Sure Where to Start?

If you’re starting from scratch, follow this:

- Open a TFSA

- Set up $250/month automatic investing

- Use a simple platform

- Increase after a few months

If you want a full walkthrough, this guide on how to start investing in Canada shows exactly how to set everything up.

Final Take

There isn’t a perfect number.

There is a clear path:

- Start

- Stay consistent

- Increase over time

If you follow that, your investing will take care of itself.

Frequently Asked Questions

How much should I invest per month in Canada?

Most Canadians should aim for 10–20% of their income, but starting at 5–10% is realistic and effective.

Is $500 per month enough to invest?

Yes. $500/month is a strong starting point and builds meaningful long-term growth over time.

Should I invest monthly or wait?

Monthly investing is generally more effective because it builds consistency and reduces timing risk.

What if I can only invest $100 per month?

That’s enough to start. Building the habit matters more than the amount early on, and you can increase contributions later.

Should I invest before paying off debt?

If you have high-interest debt (like credit cards), focus on paying that off first. Once that’s under control, you can shift toward investing consistently.

Should I invest every month or save and invest later?

Investing monthly helps reduce timing risk and builds consistency. Waiting to invest later often leads to delays and missed opportunities.

What percentage of income should I invest long term?

A long-term target of 10–20% of your income is realistic for most Canadians, with higher percentages accelerating wealth building if your budget allows.

Affiliate Disclosure

💡 GrowingWealth.ca is supported by readers. Some of the links in this article are affiliate links, which means we may earn a small commission if you open an account or make a purchase — at no extra cost to you. We only recommend products and services we personally use, trust, or believe provide genuine value to Canadians. Our reviews and comparisons are always independent and objective.