By:

Growing Wealth

Published:

Buying a home is one of the biggest financial decisions most Canadian families will ever make. For most households, a mortgage will be the largest debt they carry — and also the foundation of their long-term financial stability.

But many buyers sign mortgage contracts without fully understanding how mortgages actually work in Canada — from down payments and amortization to interest rates, the mortgage stress test, and renewal risk.

This guide explains how Canadian mortgages work step-by-step, including how lenders evaluate borrowers, how payments are structured, and what families should understand before committing to a mortgage.

Whether you’re buying your first home or upgrading for a growing family, understanding the mortgage system can help you make better financial decisions and avoid costly mistakes.

What Is a Mortgage?

A mortgage is a loan used to purchase real estate.

In Canada, the lender provides funds to buy the property, and the borrower repays the loan over time with interest. The home itself serves as collateral, meaning the lender can take possession of the property if the borrower fails to repay the loan.

A typical mortgage includes several key components:

- Down payment

- Loan amount (principal)

- Interest rate

- Payment schedule

- Amortization period

The principal is the amount borrowed after the down payment. Each mortgage payment gradually reduces the principal while also covering interest charged by the lender.

For the full home buying journey — from pre-approval through to mortgage renewal — see our complete guide to Canadian home ownership.

How Mortgages Work in Canada (Simple Explanation)

A mortgage in Canada is a loan used to purchase property where the lender provides the funds and the borrower repays the loan with interest over time. The mortgage is secured by the property itself, meaning the lender can take ownership if the borrower fails to repay the loan.

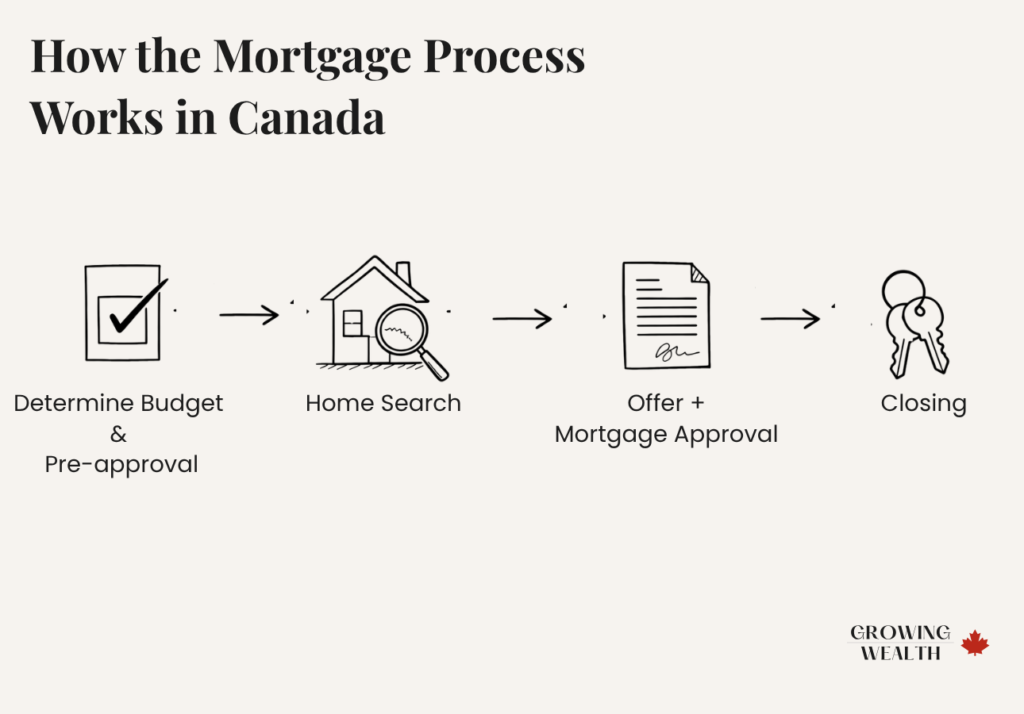

How the Mortgage Process Works in Canada

Buying a home with a mortgage generally follows five steps.

1. Determine Your Budget

Before applying for a mortgage, buyers should estimate how much home they can realistically afford.

Our full guide explains this in detail:

How Much House Can I Afford in Canada?

Lenders will evaluate:

- Income

- Existing debt

- Credit score

- Down payment

- Monthly obligations

Credit score plays a major role in mortgage approval. If you’re unsure about your score, see:

What Is a Good Credit Score in Canada?

If you’re still building your down payment, see our guide on how to save for a down payment using the FHSA and Home Buyers’ Plan — it covers how much first-time buyers can realistically set aside and in which accounts.

2. Get Pre-Approved

A mortgage pre-approval provides an estimate of how much a lender may be willing to lend.

The lender reviews:

- income documents

- employment status

- credit report

- debt levels

Pre-approvals also typically lock in an interest rate for 90–120 days, protecting buyers if rates rise while they search for a home.

For a full walkthrough of the process — including the stress test calculation and what documents to prepare — see our mortgage pre-approval guide.

3. Make an Offer on a Home

Once you find a property, you may submit an offer that includes a financing condition. This allows time for the lender to finalize mortgage approval.

4. Final Mortgage Approval

The lender will verify:

- income documents

- down payment source

- property appraisal

- employment stability

If everything meets the lender’s requirements, the mortgage is approved.

5. Closing

On closing day:

- the mortgage funds are transferred

- the property title is registered

- ownership transfers to the buyer

Mortgage payments begin shortly afterward.

Key Mortgage Terms Every Canadian Family Should Understand

Understanding mortgage terminology helps prevent confusion during the home-buying process.

Down Payment

The down payment is the portion of the home’s purchase price paid up front.

Minimum down payments in Canada:

| Home Price | Minimum Down Payment |

|---|---|

| Under $500,000 | 5% |

| $500,000–$999,999 | 5% on first $500k + 10% on remainder |

| $1 million+ | 20% minimum |

Down payments under 20% require mortgage default insurance.

Mortgage Insurance (CMHC)

If your down payment is less than 20%, you must obtain mortgage insurance from one of the following:

- Canada Mortgage and Housing Corporation (CMHC)

- Sagen

- Canada Guaranty

Mortgage insurance protects the lender, not the borrower.

Learn more from the Financial Consumer Agency of Canada.

Amortization Period

The amortization period is the total length of time required to fully repay the mortgage.

Most Canadian mortgages use a 25-year amortization, although some lenders offer 30-year amortizations when the down payment is large enough.

A longer amortization lowers monthly payments but increases total interest paid.

Mortgage Term

The term is the length of the contract with the lender.

Common mortgage terms include:

- 3 years

- 5 years

- 7 years

- 10 years

At the end of the term, the mortgage must be renewed at the current interest rate.

Types of Mortgages in Canada

Several types of mortgages are available depending on the borrower’s needs.

Closed Mortgages

Most Canadian mortgages are closed mortgages.

They typically offer lower interest rates but restrict early repayment. Breaking the mortgage early may result in penalties.

Open Mortgages

Open mortgages allow borrowers to repay the loan early without penalty.

However, interest rates are usually higher. They are often used when someone plans to sell the home within a short period.

High-Ratio Mortgages

A high-ratio mortgage is a mortgage with less than a 20% down payment.

These mortgages require mortgage insurance.

Conventional Mortgages

A conventional mortgage has a down payment of at least 20% and does not require mortgage insurance.

Fixed vs Variable Mortgages

One of the biggest mortgage decisions is choosing between fixed and variable interest rates.

See our detailed comparison here:

Fixed-Rate Mortgages

With a fixed mortgage:

- the interest rate remains the same for the entire term

- payments remain predictable

- borrowers are protected from rising interest rates

However, fixed mortgages often have higher penalties if broken early.

Variable-Rate Mortgages

Variable mortgages fluctuate with the Bank of Canada policy rate.

Advantages:

- historically lower average rates

- lower prepayment penalties

Risks:

- payments or interest costs can increase when rates rise

You can see the current interest rate policy on the Bank of Canada website.

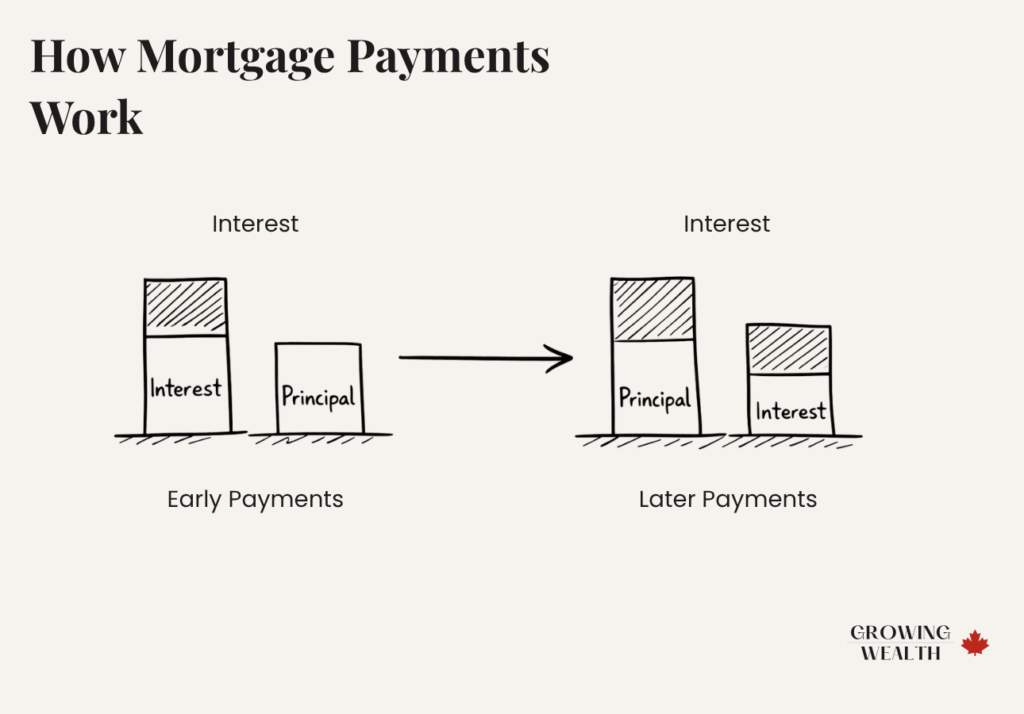

How Mortgage Payments Work

Mortgage payments typically include two components:

- Principal – repayment of the borrowed amount

- Interest – cost of borrowing from the lender

Early in the mortgage, a large portion of the payment goes toward interest. Over time, more of the payment reduces the principal balance.

For example, a $500,000 mortgage at 5% interest with a 25-year amortization results in a monthly payment of roughly $2,900. In the early years, most of that payment goes toward interest rather than reducing the loan balance.

Borrowers can also choose different payment schedules:

- monthly

- bi-weekly

- accelerated bi-weekly

Accelerated payments help reduce the amortization and save interest over time.

How Lenders Decide How Much You Can Borrow

Lenders use several factors to determine mortgage approval.

This means qualifying at the higher of:

- the contract rate + 2%

- the minimum qualifying rate set by regulators

The stress test ensures borrowers could still afford payments if interest rates rise.

More details are available from the Office of the Superintendent of Financial Institutions.

How Lenders Decide How Much You Can Borrow

Lenders use several factors to determine mortgage approval.

Income

Stable income helps demonstrate the ability to repay the mortgage.

Gross Debt Service (GDS)

GDS measures the percentage of income spent on housing costs.

Housing costs include:

- mortgage payments

- property taxes

- heating costs

Total Debt Service (TDS)

TDS measures the percentage of income spent on all debts.

This includes:

- mortgage payments

- credit cards

- car loans

- student loans

Borrowers with high debt levels may qualify for smaller mortgages.

Mortgage Renewal Risk

Many Canadian mortgages use 5-year terms but 25-year amortizations, meaning borrowers renew their mortgage multiple times. If interest rates rise between renewals, payments can increase significantly.

This renewal risk became very real for many Canadians when interest rates rose sharply after the pandemic. Planning for possible rate changes — and knowing how to negotiate your renewal — helps avoid financial stress later.

Hidden Costs of Owning a Home

Mortgage payments are only one part of the cost of home ownership.

Families should also budget for:

- property taxes

- home insurance

- maintenance and repairs

- utilities

- closing costs

- land transfer tax

The Canada Mortgage and Housing Corporation provides resources on home ownership costs.

Government Programs for Home Buyers

Several programs help Canadians save for a home.

First Home Savings Account (FHSA)

The FHSA allows Canadians to save for a first home with tax advantages similar to RRSPs and TFSAs.

Learn more in our guide:

Home Buyers’ Plan (HBP)

The Home Buyers’ Plan allows buyers to withdraw up to $35,000 from an RRSP for a home purchase.

Read further on the CRA website.

Should You Pay Down Your Mortgage or Invest?

Many homeowners face the question of whether extra money should go toward the mortgage or investments.

We explore this in detail here:

Should You Pay Down Your Mortgage or Invest?

The right choice depends on:

- mortgage interest rates

- expected investment returns

- risk tolerance

- financial goals

Common Mortgage Mistakes

Buying Too Much House

Just because a lender approves a certain amount doesn’t mean it’s the right financial decision.

Housing costs should still leave room for savings and unexpected expenses.

Ignoring Renewal Risk

Interest rates change over time. Planning for future rate increases can help avoid payment shock at renewal.

Not Understanding Mortgage Penalties

Breaking a mortgage early can result in significant penalties, especially with fixed-rate mortgages.

This is important for families who may move within a few years.

Final Thoughts

A mortgage is both a financial tool and a long-term commitment.

Understanding how mortgages work in Canada helps families make better housing decisions, avoid common mistakes, and manage long-term financial risk.

For many households, a home will represent both a place to live and a major component of their net worth. Approaching the mortgage process thoughtfully can help families build stability and long-term financial security.

Frequently Asked Questions

What credit score do you need for a mortgage in Canada?

Most lenders prefer a credit score of at least 680, although approval may still be possible with lower scores depending on income, down payment, and debt levels.

See our guide: What Is a Good Credit Score in Canada?

How much down payment do you need to buy a house in Canada?

Minimum down payments depend on the purchase price:

- 5% for homes under $500,000

- 5% on the first $500,000 and 10% on the remainder up to $999,999

- 20% for homes $1 million or more

What is the mortgage stress test?

The mortgage stress test ensures borrowers can still afford payments if interest rates rise.

Borrowers must qualify at the higher of:

- the contract rate + 2%

- the minimum qualifying rate set by regulators.

How long does it take to pay off a mortgage in Canada?

Most mortgages use a 25-year amortization, although some borrowers choose shorter or longer amortizations depending on their situation.

Can you pay off a mortgage early in Canada?

Yes. Many mortgages allow prepayment privileges, which allow borrowers to reduce the principal faster without penalties.

However, breaking the mortgage contract before the term ends may result in penalties.

Affiliate Disclosure

💡 GrowingWealth.ca is supported by readers. Some of the links in this article are affiliate links, which means we may earn a small commission if you open an account or make a purchase — at no extra cost to you. We only recommend products and services we personally use, trust, or believe provide genuine value to Canadians. Our reviews and comparisons are always independent and objective.