If you’ve built up a lump sum—whether from a tax refund, savings, or an inheritance—you’re faced with a common investing decision:

Should you invest everything at once, or spread it out over time?

In Canada, this comes down to lump sum vs dollar-cost averaging. While both approaches can work, they lead to different outcomes depending on how markets behave—and how you behave as an investor.

Lump Sum vs Dollar-Cost Averaging in Canada: Which Is Better?

In Canada, lump sum investing is usually the better strategy because markets tend to rise over time. However, dollar-cost averaging (DCA) can help reduce emotional risk if you’re concerned about short-term volatility.

For most long-term investors, the key is not choosing the perfect strategy—but making sure your money gets invested and stays invested.

Lump Sum vs Dollar-Cost Averaging Canada: Quick Comparison

| Strategy | Best For | Risk | Return Potential |

|---|---|---|---|

| Lump Sum | Long-term investors | Short-term volatility | Higher (most cases) |

| DCA | Hesitant investors | Lower timing risk | Slightly lower |

What Is Lump Sum Investing?

Lump sum investing means putting your entire amount into the market immediately.

If you have $10,000, you invest the full amount today. From that point on, your money is fully exposed to market growth and compounding.

The advantage is simple: your money starts working right away. Over time, this early exposure is what drives stronger long-term results.

What Is Dollar-Cost Averaging (DCA)?

Dollar-cost averaging means investing your money gradually over time instead of all at once.

For example, instead of investing $10,000 today, you might invest $1,000 per month over 10 months.

This reduces the risk of investing everything right before a short-term market drop and can make the process feel more manageable. However, while you’re spreading out your investments, part of your money remains uninvested—often sitting in low-return savings. If that’s the case, it’s worth understanding your options, including high-interest savings accounts in Canada.

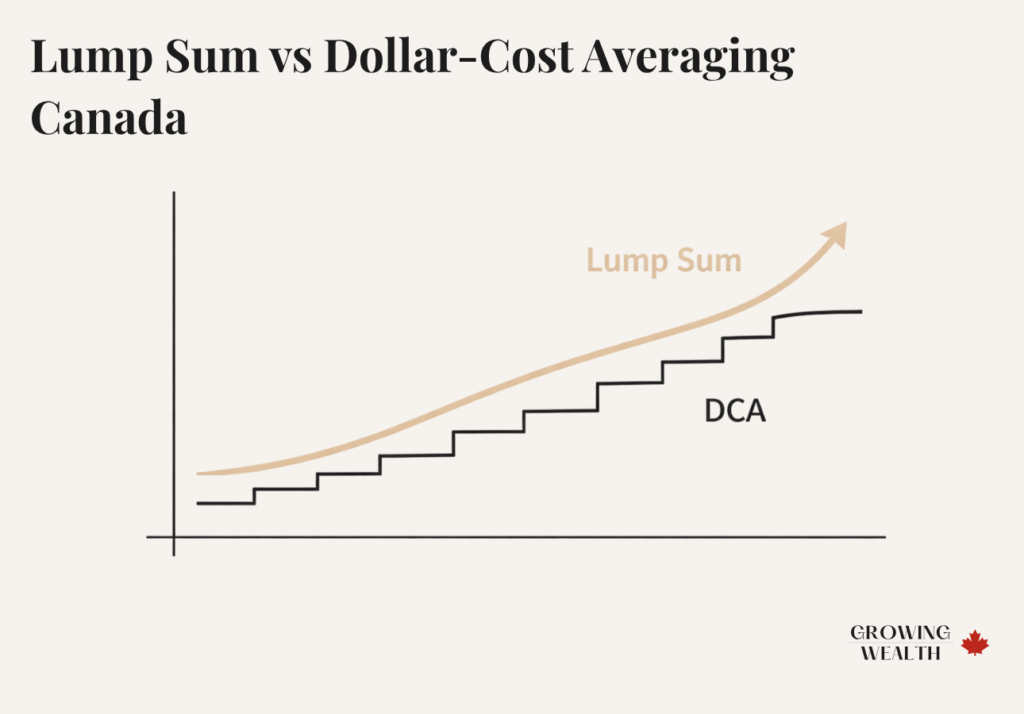

What the Data Says (Lump Sum vs DCA Performance)

This is one of the few investing decisions where the data is clear.

Research from Vanguard Group shows that lump sum investing outperforms dollar-cost averaging roughly 65–75% of the time.

The explanation is straightforward: markets rise more often than they fall, and investing earlier gives your money more time to grow.

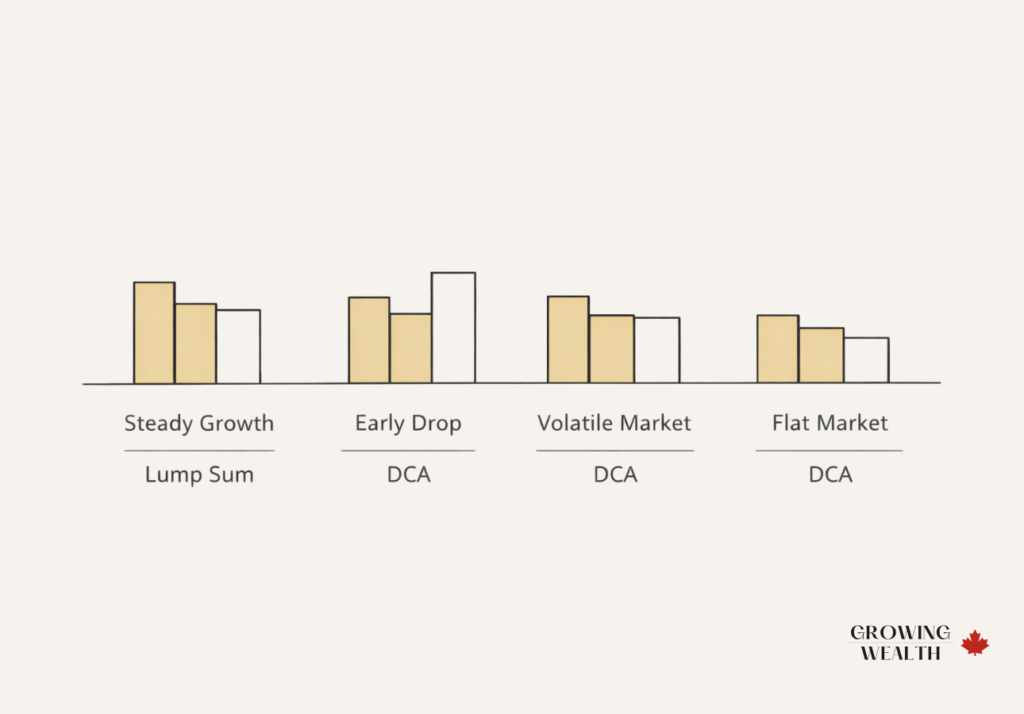

$10,000 Example: Lump Sum vs DCA Over 1 Year

To make this practical, consider investing $10,000 using two approaches:

- Lump sum: invested immediately

- DCA: invested evenly over 12 months

Both strategies are then left invested for three years.

| Market Scenario | Lump Sum Value (3 yrs) | DCA Value (3 yrs) | Outcome |

|---|---|---|---|

| Steady growth (+8% annually) | ~$12,600 | ~$11,900 | Lump sum ahead |

| Early drop (-15%, then recovery) | ~$11,300 | ~$11,700 | DCA ahead |

| Volatile market | ~$12,000 | ~$11,800 | Slight lump sum edge |

| Flat market | ~$10,300 | ~$10,200 | Minimal difference |

What matters here isn’t just which strategy wins, but how often lump sum comes out ahead when markets behave normally.

The Real Risk: Market Timing and Behaviour

Most investors don’t struggle with understanding these strategies—they struggle with acting on them.

The hesitation usually comes from trying to avoid regret. It’s the feeling that if you just wait a bit longer, you’ll make a better decision.

In reality, waiting rarely leads to clarity. It usually leads to more waiting.

This is why having a clear process matters. If you’re unsure where to begin, following a step-by-step approach in our guide on how to start investing in Canada (coming soon) can help you move forward with confidence.

Why Most People Choose the Wrong Strategy

The issue isn’t knowledge—it’s behaviour.

Investors tend to avoid losses more strongly than they pursue gains. They delay decisions to avoid being wrong and overanalyze short-term market movements.

The result is predictable: money sits in savings instead of being invested.

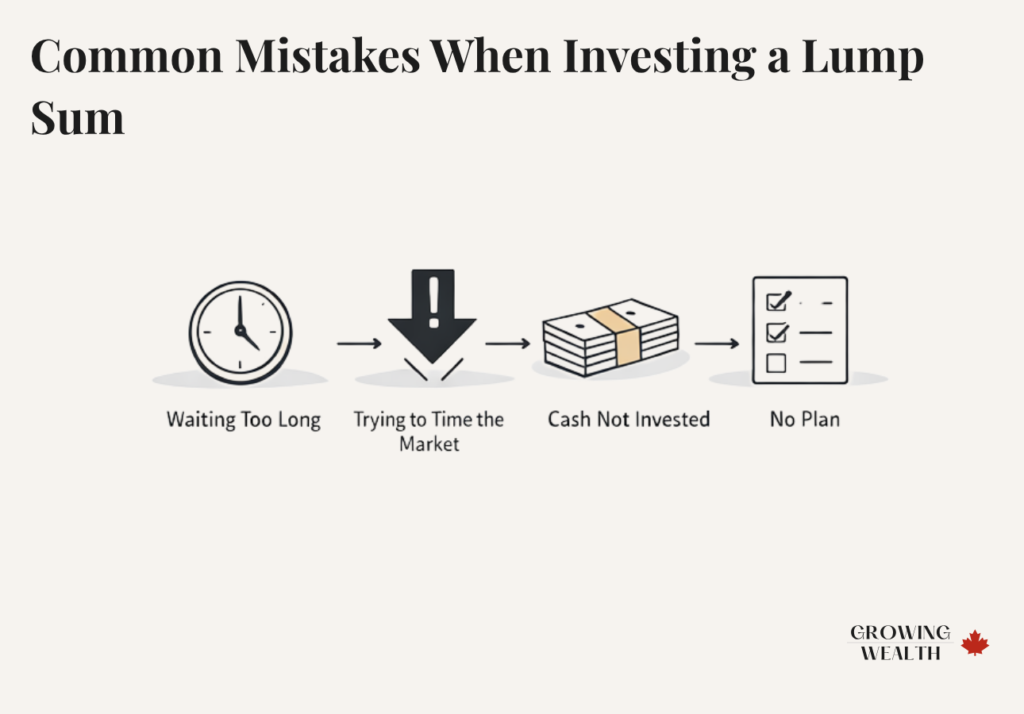

Common Mistakes When Investing a Lump Sum

Even when investors understand the strategies, they often make avoidable mistakes.

The most common ones include:

- Waiting too long to invest

- Spreading investments over 12–24 months

- Trying to predict market crashes

- Investing without a clear plan

- Leaving large amounts of cash idle

Each of these tends to reduce long-term returns more than choosing between lump sum and DCA.

Should You Wait for a Market Crash in Canada?

This is one of the most common questions—and one of the most damaging.

Markets are unpredictable in the short term. Waiting for a crash often leads to missed growth and delayed investing decisions.

For long-term investors, staying invested is far more important than trying to time entry points.

When Lump Sum Investing Makes Sense

Lump sum investing is generally the better choice when your financial base is already in place and your timeline is long.

This usually applies when you are investing for at least five years, have an emergency fund, and won’t need the money in the short term. Before investing, it’s important to confirm your foundation is solid by reviewing your emergency fund strategy in our Emergency Fund guide.

When Dollar-Cost Averaging Makes Sense

Dollar-cost averaging is most useful when it helps you move forward.

If investing all at once feels uncomfortable enough that you might delay or avoid investing, spreading your investments over a short period can be a practical compromise.

Used properly, it provides structure without significantly sacrificing long-term results.

The Strategy Most People Should Actually Use

This decision is often framed as lump sum versus DCA, but in practice, most investors benefit from using both.

A more effective approach is to invest your existing lump sum immediately, then continue investing regularly over time as new income becomes available.

This allows you to capture immediate market exposure while building a consistent investing habit.

Where Should You Invest a Lump Sum in Canada?

Once you’ve decided how to invest, the next step is choosing where and what to invest in.

For most Canadians, this starts with selecting the right account. Understanding the differences between a TFSA and RRSP is critical, since each has different tax implications depending on your income and long-term plans.

After choosing an account, the next step is selecting investments. Many investors begin with simple, diversified ETFs, which are explained in more detail in our guide on what you should actually invest in.

A widely used ETF strategy can also be found through Canadian Couch Potato’s model portfolios, which provide simple, low-cost portfolio examples.

Example Scenarios (Canadian Context)

Tax Refund

If you receive a tax refund and plan to invest it long-term, investing it sooner is usually the better choice. If you’re unsure how to prioritize it, reviewing how to allocate your tax refund effectively can help clarify your next step.

Savings or Inheritance

With larger amounts, hesitation tends to increase.

In these situations, a blended approach—investing most of the amount upfront and gradually investing the remainder—can reduce hesitation while still capturing most of the market exposure.

Ongoing Investing

If you invest regularly from your income, you are already using dollar-cost averaging. This is not a strategy decision—it is simply how consistent investing works over time.

Final Recommendation

For most Canadian investors, the conclusion is consistent.

Lump sum investing is more effective from a mathematical standpoint, while dollar-cost averaging can help manage behaviour.

The priority is not choosing perfectly. It is making sure your money is invested, stays invested, and continues to be invested over time.

Frequently Asked Questions

Is lump sum investing better than DCA in Canada?

In most cases, yes. Because markets tend to rise over time, investing earlier usually leads to better outcomes. DCA can still be useful if it helps you stay invested.

What if I invest and the market drops immediately?

This will happen at some point. The key is staying invested so your portfolio has time to recover.

How long should dollar-cost averaging last?

A short period—typically a few months—is usually sufficient. Longer periods often reduce returns without significantly lowering risk.

Should I wait for a better time to invest?

No. Waiting for the “right time” often leads to missed opportunities.

What should I invest in after deciding?

Simple, diversified ETF portfolios are widely recommended, such as those outlined in Canadian Couch Potato’s model portfolios.

Should I invest or pay off debt first?

High-interest debt should generally be paid off before investing. Lower-interest debt depends on your broader financial plan.

Affiliate Disclosure

💡 GrowingWealth.ca is supported by readers. Some of the links in this article are affiliate links, which means we may earn a small commission if you open an account or make a purchase — at no extra cost to you. We only recommend products and services we personally use, trust, or believe provide genuine value to Canadians. Our reviews and comparisons are always independent and objective.