Most Canadians don’t avoid investing because they don’t care about their future. They avoid it because it feels unclear.

There are too many choices—TFSA or RRSP, robo-advisor or brokerage, ETFs or stocks—and no obvious starting point. Add in the fear of losing money, and it’s easy to delay.

That delay is what actually costs you.

Investing is not complicated when you follow a structured approach. You don’t need to predict markets or pick winning stocks. You need a system.

This guide gives you that system—step by step.

If you want to start investing in Canada, the simplest approach is:

- Open a TFSA or RRSP

- Choose a low-cost platform like Wealthsimple or Questrade

- Invest in a diversified ETF

- Contribute consistently over time

How to Start Investing in Canada (Quick Answer)

To start investing in Canada:

- Build a 3–6 month emergency fund

- Pay off high-interest debt

- Open a TFSA or RRSP

- Choose a platform like Wealthsimple or Questrade

- Invest in a low-cost ETF

- Contribute monthly and automate

Step 1 – Make Sure You’re Ready to Invest

Before you invest anything, you need to remove the risks that can force you to undo your progress.

Investing without a financial base usually leads to selling at the worst possible time.

You should start by building a proper emergency buffer. If you don’t yet have 3–6 months of essential expenses saved, focus there first. This protects you from unexpected expenses and prevents you from pulling money out of investments when markets are down.

If you need a structured approach, follow this complete emergency fund strategy for Canadian.

At the same time, eliminate high-interest debt—especially credit cards. A guaranteed return from paying off debt will outperform most investments.

Finally, separate short-term money from long-term investing. If you’ll need money within the next few months for travel, kids’ activities, or home expenses, it shouldn’t be invested.

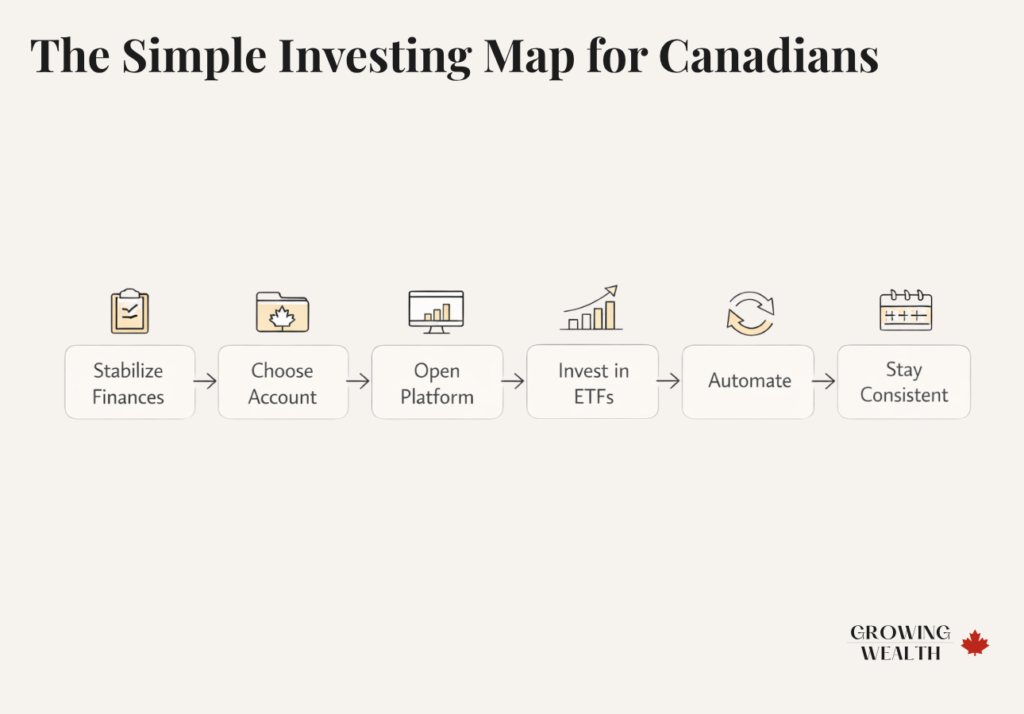

The Simple Investing Map for Canadians

If you zoom out, investing follows a predictable structure:

- Stabilize your finances

- Choose the right account

- Open a platform

- Invest in diversified ETFs

- Automate contributions

- Stay consistent

Most people struggle because they skip steps or try to optimize too early.

Step 2 – Choose the Right Account (TFSA vs RRSP)

Before choosing investments, you need to choose the account that will hold them.

In Canada, that usually means starting with a TFSA or RRSP.

Quick Comparison

| Feature | TFSA | RRSP |

|---|---|---|

| Tax on contributions | No deduction | Tax deduction |

| Growth | Tax-free | Tax-deferred |

| Withdrawals | Tax-free | Taxed |

| Best for | Flexibility | Tax reduction |

The TFSA is often the best starting point because of its flexibility. Your investments grow tax-free, and you can withdraw funds without triggering taxes.

If you’re not fully clear on how contribution room, withdrawals, and limits work, review this complete TFSA guide for Canadians.

The RRSP works differently. Contributions reduce your taxable income today, but withdrawals are taxed later. This makes it more valuable when your income—and tax rate—are higher.

For a deeper breakdown, this RRSP guide for Canadians explains how it works.

If you’re deciding between the two, this TFSA vs RRSP comparison for Canadians walks through real scenarios.

You can also refer to official CRA rules:

Once you’ve chosen your account, the next step is where to open it.

Step 3 – Choose an Investment Platform

Your platform is the tool that holds your account and lets you invest.

For most Canadians, this comes down to simplicity versus control.

| Platform | Best For | Key Features | Fees | Ease of Use | Get Started |

|---|---|---|---|---|---|

| Wealthsimple | Beginners, hands-off investors | Automated investing, portfolio management, simple interface | Slightly higher | Very easy | 👉 Apply for a Wealthsimple account |

| Questrade | DIY investors | Self-directed trading, ETF purchases, full control | Lower | Moderate | 👉 Apply for a Questrade account |

Most people assume this decision is about fees. It isn’t.

It’s about behaviour.

If you want simplicity and automation, Wealthsimple is the easiest way to start. If you want control and lower long-term costs, Questrade gives you that flexibility.

If you’re unsure, start simple. You can always optimize later.

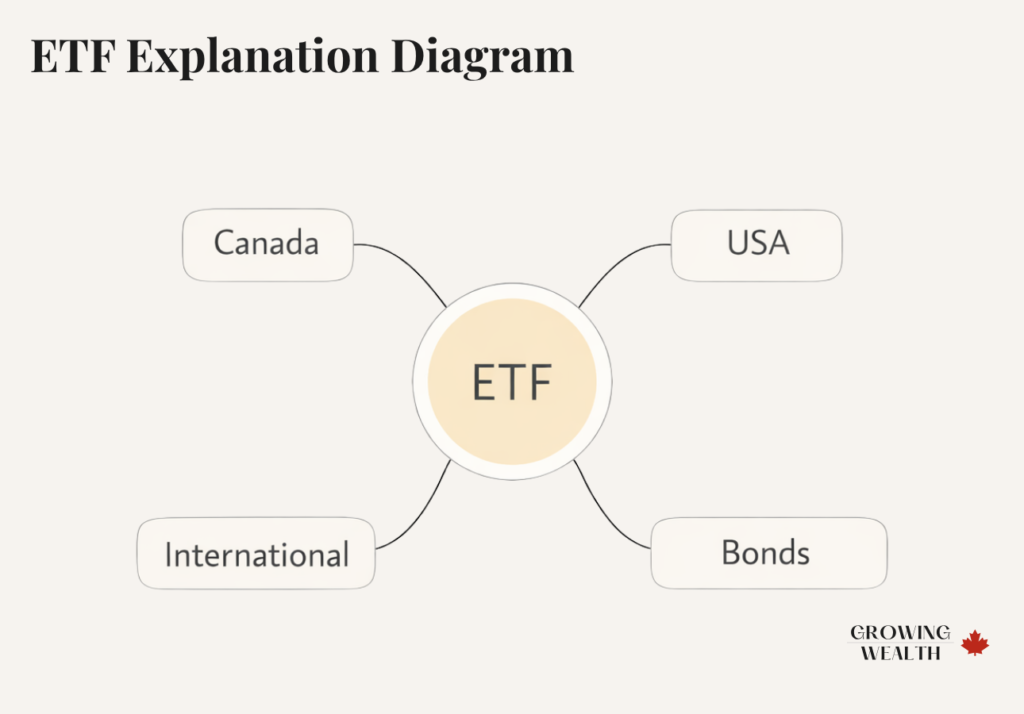

Step 4 – What Should You Actually Invest In?

This is where most beginners get stuck—and where most bad decisions happen.

Once your account is open, it’s tempting to search for the “best investment.” That usually leads to stock picking, trends, or reacting to headlines.

That approach introduces risk without improving long-term results.

A better approach is to focus on structure instead of prediction.

Start with ETFs. An ETF gives you exposure to hundreds or thousands of companies at once, reducing risk and simplifying decisions.

This is called index investing—tracking the market instead of trying to beat it.

A typical beginner portfolio includes exposure to Canadian, U.S., and international markets—often combined into a single all-in-one ETF.

If you want a full breakdown of what to buy and how to structure it, read what you should actually invest in as a beginner in Canada.

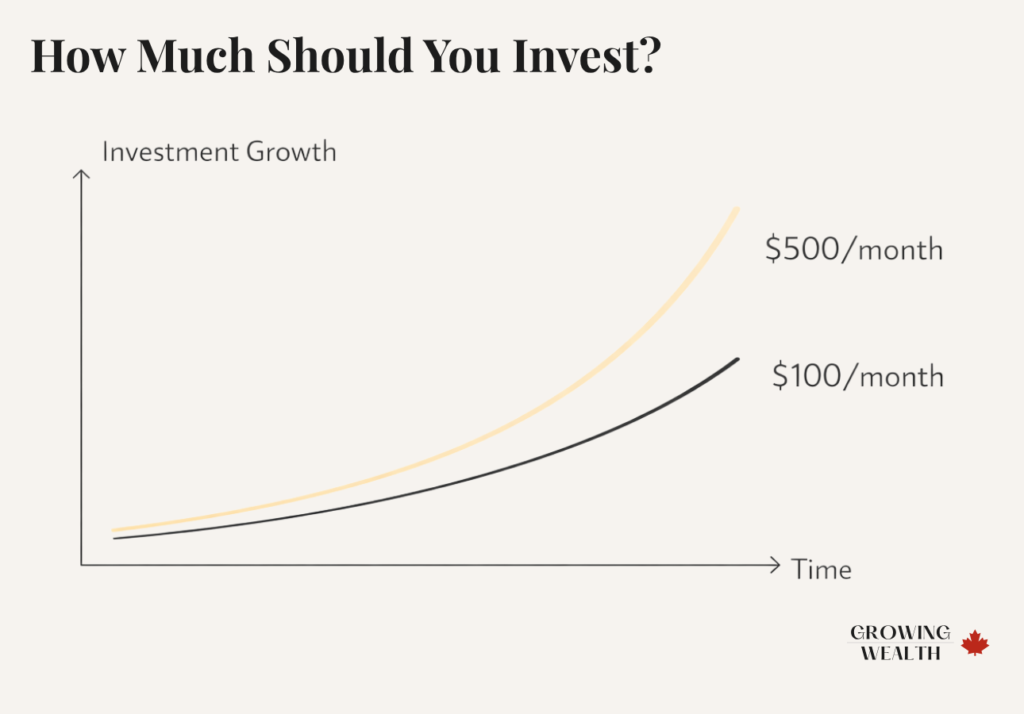

Step 5 – How Much Should You Invest?

Most people overestimate how much they need to start and underestimate how powerful consistency is.

The amount matters far less than the habit.

Someone investing a few hundred dollars every month for years will outperform someone investing larger amounts inconsistently.

A simple starting point:

- $100/month gets you started

- $250/month builds momentum

- $500/month creates strong long-term progress

If you want a structured way to decide your number, see how much you should be investing each month in Canada.

How Long Should You Stay Invested?

Investing only works when time is on your side.

- 3 years → moderate risk

- 5+ years → more stability

- 10+ years → meaningful compounding

Short-term investing increases risk. Long-term investing reduces it.

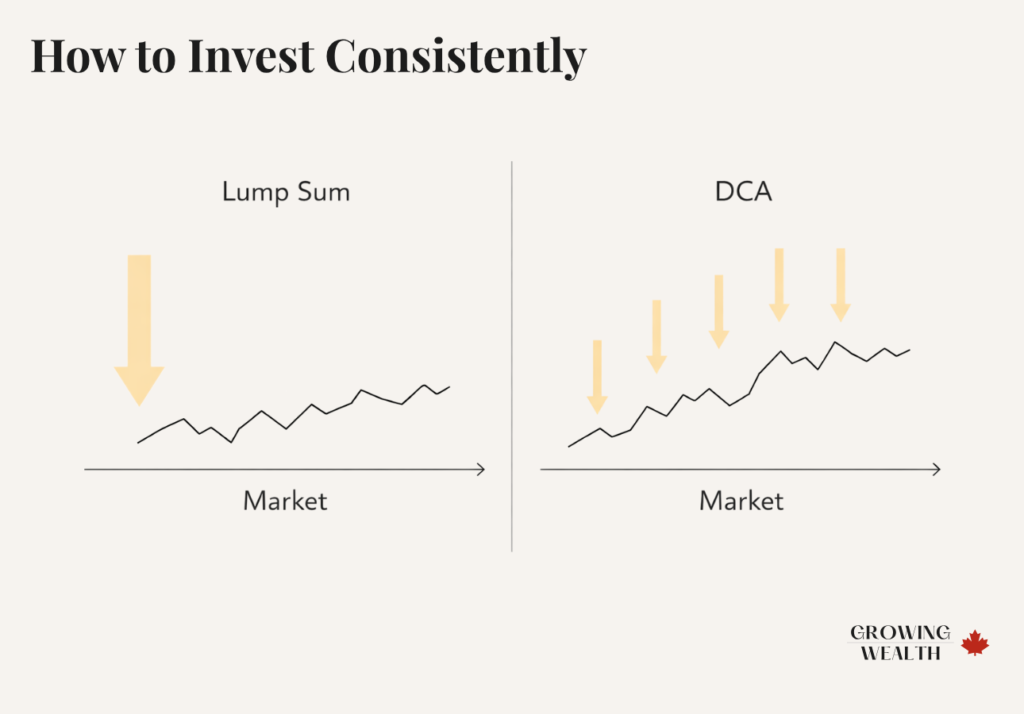

Step 6 – How to Invest Consistently (Lump Sum, DCA, and Automation)

Once you know how much to invest, the next step is deciding how to actually invest it—and how to keep doing it consistently.

There are two main approaches.

Lump sum investing means investing everything at once. This typically produces better long-term results because your money is working sooner.

Dollar-cost averaging means investing gradually over time. This reduces emotional stress and avoids worrying about timing.

If you’re investing from income, dollar-cost averaging happens naturally. If you have a large amount ready, lump sum is often more effective.

If you want a deeper breakdown, this lump sum vs dollar-cost averaging guide for Canadians explains when each approach makes sense.

Why Automation Is What Actually Matters

Most people don’t fail because they chose the wrong investing method.

They fail because they stop.

Without a system, investing becomes something you intend to do instead of something that actually happens.

Automation solves this.

By setting up automatic contributions and investments, you remove decision-making and ensure consistency over time.

If you want to build this into your finances, follow this simple family finance system for Canadians.

Common Mistakes Beginners Make

Most investing mistakes are predictable.

Waiting too long reduces the power of compounding.

Overcomplicating leads to hesitation and inconsistency.

Trying to time the market rarely works.

Picking individual stocks increases risk without improving outcomes.

Ignoring fees quietly reduces long-term returns.

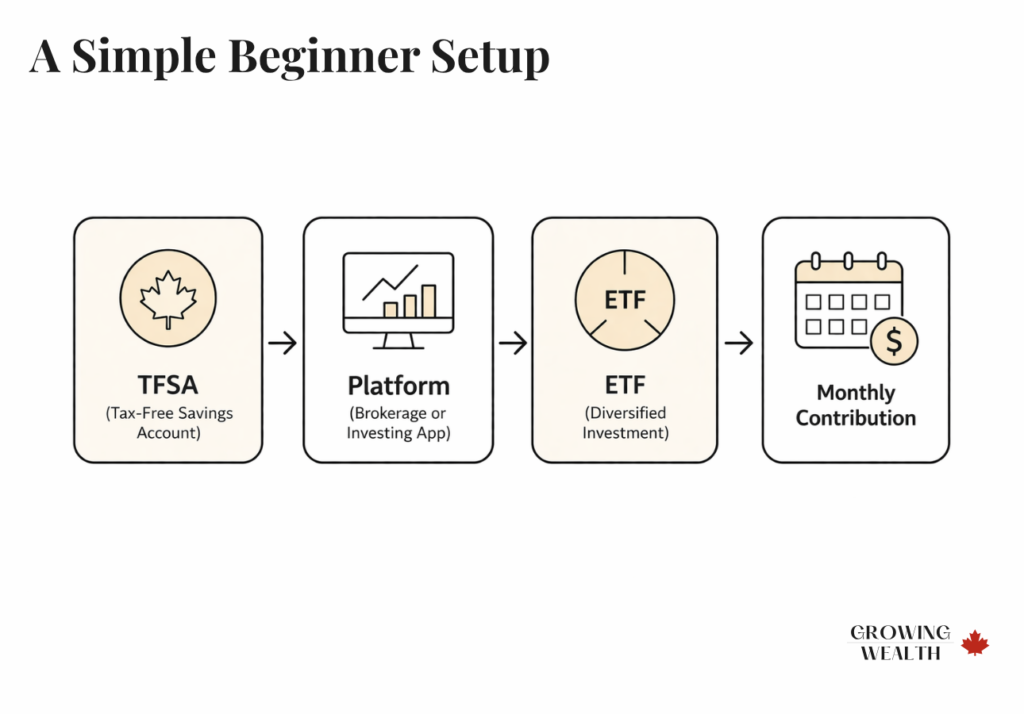

Example – A Simple Beginner Setup

At this point, you don’t need more theory—you need a starting point.

A simple setup:

- TFSA account

- Wealthsimple platform

- One diversified ETF

- $500 monthly automated contribution

This removes complexity, builds consistency, and allows compounding to work over time.

Final Thoughts

Investing is often presented as complex, but the reality is simpler.

You don’t need to predict markets or pick stocks.

You need a system:

- Choose the right account

- Use a low-cost platform

- Invest in diversified ETFs

- Contribute consistently

Start with that. Improve later.

Frequently Asked Questions

How much money do you need to start investing in Canada?

You can start with as little as $100. Consistency matters more than the amount.

Is Wealthsimple good for beginners?

Yes. It simplifies investing and removes most of the complexity.

Should I invest or pay off debt first?

High-interest debt should be paid off before investing.

What is the best investment for beginners in Canada?

For most beginners, a low-cost, diversified ETF is the best starting point.

Can I start investing with $100 in Canada?

Yes. Many platforms allow small starting amounts.

Can I lose money investing?

Yes, especially in the short term. Long-term investing reduces that risk.

TFSA or RRSP first?

Most beginners should start with a TFSA unless they are in a higher tax bracket.

How often should I invest?

Monthly investing is the simplest and most effective approach.

Affiliate Disclosure

💡 GrowingWealth.ca is supported by readers. Some of the links in this article are affiliate links, which means we may earn a small commission if you open an account or make a purchase — at no extra cost to you. We only recommend products and services we personally use, trust, or believe provide genuine value to Canadians. Our reviews and comparisons are always independent and objective.