This article contains affiliate links. We may earn a commission if you open an account — at no cost to you. We only recommend products we’ve researched and trust.

Home Buying

Home Buying

In This Article

Your mortgage renewal is not a formality. It’s one of the few moments in homeownership where you have real leverage — the ability to shop around, negotiate, and change your terms. Most Canadians sign the renewal letter their lender mails them and move on. That decision can cost thousands over the next five years.

If your renewal is 60–90 days away, you still have time to do this properly. Here’s exactly what to do and when.

What mortgage renewal actually means

Your mortgage has two timelines: the amortization (typically 25 years — how long until the mortgage is fully paid off) and the term (usually 5 years — the period covered by your current rate and conditions). At the end of each term, you renew. You’re not applying for a new mortgage; you’re negotiating the terms for the next stretch of your existing one.

This distinction matters because it shapes your rights. If you’re staying with the same lender, you typically don’t need to re-qualify at renewal, even if your income has changed. If you’re switching lenders, you will need to re-qualify under today’s stress test rules.

According to the Financial Consumer Agency of Canada, your lender is legally required to send a renewal statement at least 21 days before your term ends. That’s the legal minimum — not a recommendation for when to start thinking about it. By the time that letter arrives, you’ve already missed most of your window.

The rate reality for 2026 renewals

Over 1.15 million Canadian mortgages are renewing in 2026, according to CMHC estimates. A significant share of those were locked in during 2020 and 2021, when 5-year fixed rates sat between 1.5% and 2.5%. Those borrowers are now renewing into a meaningfully different environment.

The good news: rates have fallen substantially from their 2023 peak of 5%. The Bank of Canada held the overnight rate at 2.25% in April 2026, and most economists expect it to stay roughly there through the year. That means fixed rates have stabilized, and the severe payment shock that was predicted for this renewal wave has been partially absorbed by rate cuts.

That said, if you locked in at 2.1% five years ago, renewal at 4.09% still represents a real increase in monthly cost. Here’s what that looks like concretely.

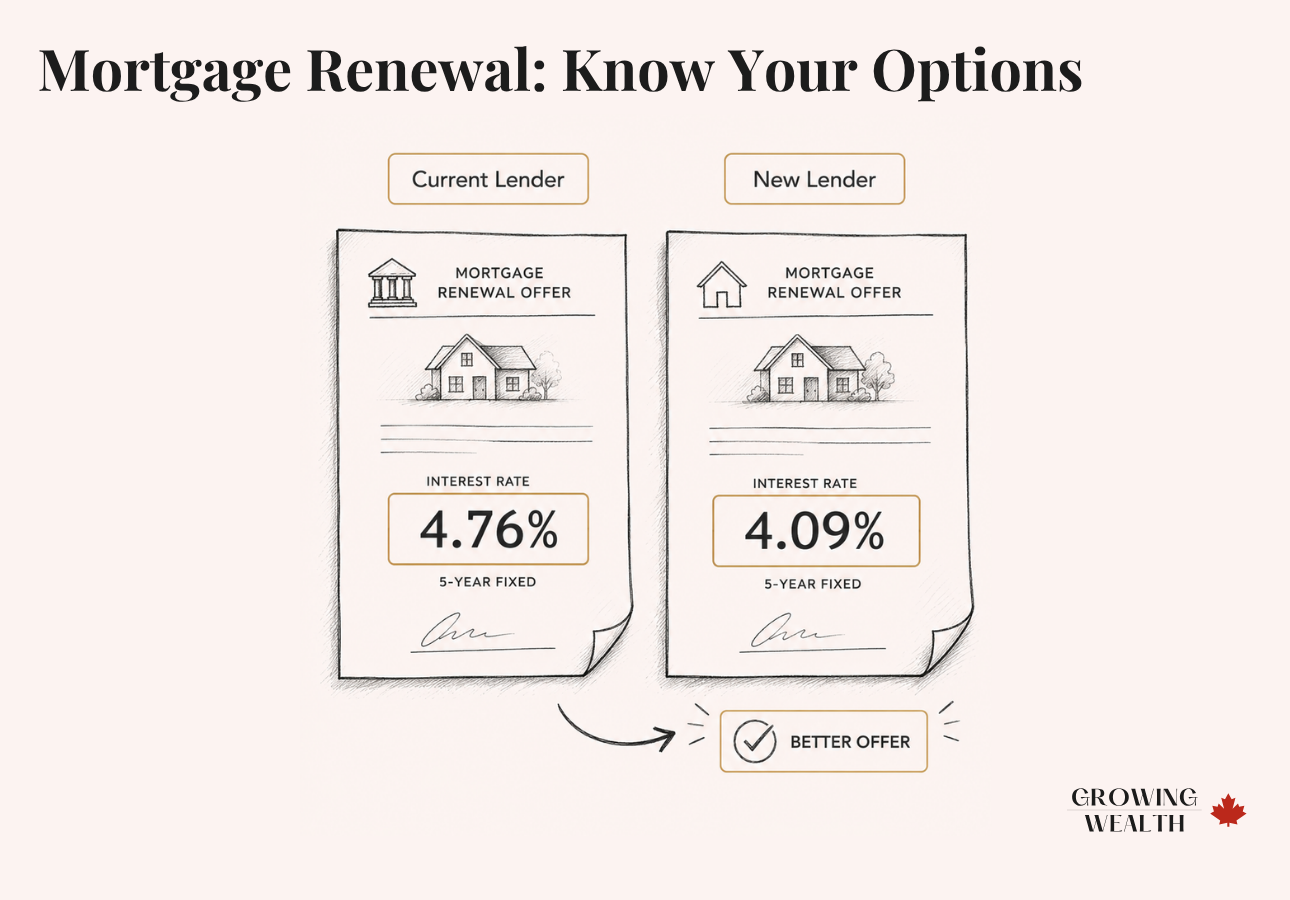

On a $450,000 balance with a 20-year remaining amortization, a rate of 2.1% produces a monthly payment of roughly $2,295. Renewing at the best available 5-year fixed today (4.09%) pushes that to approximately $2,740 per month — an increase of about $445/month, or $5,340 per year. That’s real money. The difference between that rate and what a big bank might post (4.76%) is another $180/month, or $10,800 over five years. Shopping the renewal matters.

Your 120-day renewal action plan

Most rate holds are 120 days — that’s when you should start the process, not 90 days out. Starting at the full 120-day mark gives you the entire window to shop, negotiate, and make a decision without any deadline pressure. Here’s the timeline.

Pull your mortgage statement and note your exact renewal date, remaining balance, and current rate. Then contact a mortgage broker and get a rate hold. A rate hold locks in today’s best available rate for up to 120 days — if rates go up before you renew, you’re protected. If they go down, you can take the lower rate instead. This costs you nothing and eliminates rate risk for the entire shopping window. Starting here, at 120 days, means you have maximum time to compare and negotiate without pressure.

Contact at least two lenders or brokers beyond your current one and get written rate offers. These don’t need to be final applications — just enough to see what the market will actually give you. A written offer from a competing lender is the single most effective negotiating tool you have with your current bank. Without one, you’re asking your lender to compete against nothing.

Call your current lender — not the branch, the retention department — and present your competing offers. Ask them directly: “Can you beat this rate?” Many lenders will match or come close rather than lose a customer who’s already qualified. See the negotiation section below for exactly how to run this conversation.

Compare your lender’s best offer against the competing offers, factoring in any switching costs (legal fees, discharge fees) if you’re moving to a new lender. If you have mortgage default insurance and are switching lenders, you may not need to re-qualify. If you don’t, you will need to pass the stress test at the new lender. Confirm before committing.

Complete the renewal agreement with your chosen lender. If switching, confirm the discharge and transfer timeline with both lenders to avoid any gap. If staying, confirm the rate, term, and payment amount in writing before signing.

Stay with your lender or switch?

Your current lender’s renewal offer is their opening bid, not their best offer. They know most Canadians renew by convenience. That’s what they’re counting on.

| Your Situation | What It Suggests |

|---|---|

| Lender matches the best market rate after negotiation | Stay — switching costs aren’t worth it when rates are equal |

| Lender’s best offer is 0.20%+ above the market | Switch — the math usually favours moving after accounting for fees |

| You have CMHC-insured mortgage and are switching | Switch is easier — you typically don’t need to re-qualify |

| You have a conventional mortgage and your income has changed | Check if you’d pass the stress test before committing to switch |

| You want to refinance (access equity or change amortization) | Renewal is the moment to do it — refinancing mid-term triggers a penalty |

| Your current lender has a collateral charge mortgage | Switching is more complex and costly — factor in legal fees (~$1,000–$1,500) |

The typical cost to switch lenders at renewal includes a discharge fee from your current lender ($200–$350), legal or title transfer fees ($500–$1,200 depending on province), and potentially an appraisal fee. A broker will often cover some or all of these costs. Add them up and compare against the rate savings before deciding.

If you have a collateral charge mortgage — which most Big Six banks register by default — switching lenders requires a full legal discharge and re-registration rather than a simple assignment. This adds cost and complexity. Ask your lender now which type of charge your mortgage uses.

Fixed or variable at renewal?

With the Bank of Canada holding at 2.25% and most forecasters expecting rates to stay roughly flat through 2026, this decision comes down to your tolerance for uncertainty — and your financial cushion if rates move unexpectedly.

| Choose Fixed if… | Consider Variable if… |

|---|---|

| Your budget is tight and you need predictable payments | You have room to absorb a payment increase of $200–$300/month |

| You’re planning to sell or move within 3–5 years and want no surprises | You believe the Bank of Canada is more likely to cut than raise from here |

| You’d lose sleep over rate increases during the term | You value flexibility and may want to break or refinance before term end |

| The rate spread between fixed and variable is less than 0.50% | The rate spread between fixed and variable is 0.75%+ in variable’s favour |

As of May 2026, the best 5-year fixed (4.09%) and best 5-year variable (3.35%) from brokers are separated by 0.74 percentage points. That’s a meaningful spread in variable’s favour — but variable means your rate moves with the prime rate, and if the Bank of Canada raises in late 2026 or 2027, that spread can narrow or disappear. On a $450,000 balance, the current savings from variable over fixed is roughly $200/month. You’d need rates to stay roughly flat for about three years to come out ahead over a 5-year term, assuming one rate increase.

For most families where budget predictability matters, a 5-year fixed remains the lower-risk choice. If you have financial flexibility and want to benefit if rates continue to ease, a 3-year fixed or variable is worth modelling out with a broker who can run the numbers on your specific balance.

For a deeper look at how fixed and variable mortgages work under the hood, see our fixed vs. variable mortgage guide.

How to negotiate your renewal rate

Thirteen percent of Canadians don’t know their mortgage rate is negotiable at renewal, according to FCAC research. Of those who do negotiate, most don’t do it effectively. Here’s what actually works.

Call the retention department, not the branch

Branch staff typically have less authority to move on rate. Ask to speak with the mortgage retention team specifically — they have more pricing flexibility and a direct incentive to keep you as a customer.

Lead with a written competing offer

Don’t say “I’ve been looking around.” Show them a specific written offer: “I have a 5-year fixed at 3.94% from [lender]. Can you match that?” A concrete number forces a concrete response. Vague pressure is easy to deflect; a documented competing offer is not.

Ask about the full package, not just rate

Your lender may not budge on rate but might offer to waive the discharge fee, increase your prepayment privileges, or provide a cash-back incentive. These have real dollar value. Get the full picture before walking away.

Be willing to leave

Your negotiating position is only as strong as your willingness to actually switch. If you’ve already done the work to get competing offers and you’ve confirmed you’d qualify at the new lender, you’re in a real position. If you haven’t, your current lender knows it.

The auto-renewal trap

If you do nothing before your term ends, your lender will almost certainly auto-renew your mortgage. Under federal rules, your lender must give you at least 21 days’ written notice — but that notice often includes a default renewal offer at a posted rate, which is almost never the best rate available.

An auto-renewal locks you in for another full term on those terms. Breaking a mortgage mid-term to get a better rate triggers a prepayment penalty — typically three months’ interest on a variable rate, or an Interest Rate Differential (IRD) calculation on a fixed rate that can reach several thousand dollars on a large balance.

If your renewal is approaching and you’re feeling overwhelmed, the single most useful thing you can do is contact a mortgage broker. They’re paid by the lender, not by you, and they can shop your renewal across dozens of lenders without you doing the legwork. Most Canadians who use a broker at renewal end up with a lower rate than they’d have gotten by calling their bank directly.

See our guide to how mortgages work in Canada for a full explanation of prepayment penalties and how the IRD is calculated.

The Bottom Line

If your renewal is 60–90 days away, you’re in the window where action pays. Get a rate hold from a broker now, collect at least two written competing offers, and call your lender’s retention team with those offers in hand. That sequence alone can save the average Canadian homeowner $5,000 to $15,000 over a five-year term.

The 2026 rate environment is more favourable than it was in 2023 — the Bank of Canada overnight rate is at 2.25% and the best available 5-year fixed from brokers is around 4.09%. That’s meaningfully lower than big bank posted rates of 4.32%–4.86%. The difference is negotiable. Most of it won’t come to you unless you ask for it.

Don’t sign the first renewal offer your lender sends. It almost always has room to move.Frequently Asked Questions

Most lenders allow you to renew up to 120 days (about four months) before your current term ends without triggering a prepayment penalty. This early renewal window is when you should be shopping, comparing offers, and negotiating — not in the final weeks before the deadline. The earlier you start, the more leverage you have.

It depends on your mortgage type. If you have an insured mortgage (one with CMHC, Sagen, or Canada Guaranty default insurance), you typically don’t need to requalify under the stress test when switching lenders at renewal — this is a right established under the Canadian Mortgage Charter. If your mortgage is uninsured (conventional, with 20% or more equity), you will need to pass the stress test at the new lender. Confirm your mortgage type before committing to a switch.

You’ll be locked into whatever rate and terms were in that offer for your next full term. The rate in a lender’s initial renewal letter is almost never their best rate — it’s their opening offer. If you sign without negotiating or shopping around, you give up your chance to reduce your rate. On a $400,000–$500,000 balance, the difference between a posted rate and a negotiated rate from a broker can easily be $10,000 or more over five years.

Yes, renewal is one of the most accessible moments to adjust your amortization. If you want to pay your mortgage off faster, you can shorten the remaining amortization period — this increases your monthly payment but reduces your total interest cost significantly. If your budget is tighter than when you first borrowed, you may be able to extend the amortization to reduce monthly payments. Note that extending the amortization increases your total interest cost over time. Your lender needs to approve the change, and switching to a new lender with a different amortization may require full requalification.

For most homeowners, yes. A mortgage broker is paid by the lender — not you — and can shop your renewal across dozens of lenders simultaneously, including smaller credit unions and trust companies that consistently offer rates below the Big Six banks. Brokers also know which lenders will cover switching costs, which is valuable if you’re considering a move. The main limitation is that some major banks (like RBC and TD) don’t work with brokers, so you’ll need to negotiate with them directly if you want to compare.

If you’re switching lenders at renewal and need to requalify, the stress test requires you to qualify at the higher of 5.25% or your contract rate plus 2%. As of May 2026, with the best 5-year fixed rates at approximately 4.09%, the stress test rate is 6.09% (contract rate + 2%), since that exceeds the 5.25% floor. If you’re staying with your current lender at renewal, you don’t need to pass the stress test regardless of your mortgage type.

A shorter term makes sense if you believe rates will fall meaningfully before your next renewal — you’d be locking in for less time and renewing again when rates are lower. The risk is that you’re exposed to renewal uncertainty more frequently, and short-term fixed rates are currently higher than 5-year fixed rates in most cases. A 3-year fixed rate from a broker is currently around 3.9%–4.4% depending on the lender — not dramatically lower than a 5-year fixed. The right choice depends on your rate outlook and how much certainty you want. Discuss this with a broker who can model it on your specific balance.

Want to understand everything that goes into your mortgage — amortization, interest calculations, prepayment penalties, and how your payments are structured? Read How Mortgages Work in Canada — a complete breakdown of the mechanics before and after renewal.