Getting pre-approved for a mortgage is one of the first real steps in buying a home — and one of the most misunderstood. Many buyers skip it or confuse it with a basic pre-qualification, then find themselves scrambling when they find a home they want. A proper pre-approval tells you exactly what you can borrow, locks in a rate for up to 120 days, and signals to sellers that you’re a serious, qualified buyer. Here’s how to do it right.

This article contains affiliate links. We may earn a commission if you open an account — at no cost to you. We only recommend products we’ve researched and trust.

HOME BUYING

HOME BUYING

In This Article

- Pre-Approval vs. Pre-Qualification

- What Lenders Actually Check

- The Pre-Approval Process, Step by Step

- Documents You’ll Need

- The Mortgage Stress Test Explained

- Broker vs. Bank: Which Should You Use?

- Where to Keep Your Down Payment While You Wait

- After Pre-Approval: What Comes Next

- The Bottom Line

- Frequently Asked Questions

Pre-Approval vs. Pre-Qualification: Not the Same Thing

These terms get used interchangeably, but they represent very different levels of commitment from a lender. The distinction matters when you’re making an offer on a home.

| Feature | Pre-Qualification | Pre-Approval |

|---|---|---|

| How it works | Self-reported financial estimate | Lender verifies your finances |

| Credit check | Soft check or none | Hard inquiry (may affect score temporarily) |

| Documents required | None or minimal | Full document package |

| Rate hold | ✗ No | ✓ 90–120 days |

| Seller confidence | Low | High |

| Worth doing | Only to get a rough number early | Always — before serious house hunting |

A pre-qualification gives you a ballpark. A pre-approval tells you where you actually stand. Always get pre-approved before making offers — especially in competitive markets where sellers expect it.

A pre-approval is conditional, not a guaranteed mortgage. The lender will still need to appraise the property you choose and confirm your financial situation hasn’t changed. Think of it as a strong commitment, not a signed contract.

What Lenders Actually Check

Lenders assess four areas when reviewing your pre-approval application. Understanding these lets you identify and fix weak spots before you apply.

1. Income and employment

Lenders want to see stable, verifiable income. Salaried employees have the easiest time — two recent pay stubs and a letter of employment usually suffice. Self-employed applicants typically need two years of T1 generals and Notices of Assessment, since lenders use declared income on tax returns. If you’ve aggressively minimized your taxable income, your qualifying mortgage amount will be lower than you might expect.

2. Credit score

A score of 680 or higher is the standard threshold for major banks and “A lenders” (the best rates and terms). Scores between 600 and 679 can still qualify for CMHC-insured mortgages, but you’ll likely face a smaller selection of lenders and potentially higher rates. A score below 600 typically requires alternative lenders or a co-borrower. Checking your own score does not hurt it — it’s only the lender’s hard inquiry that has a temporary impact, typically 5–10 points.

3. Down payment

The size of your down payment affects both your maximum mortgage amount and whether CMHC mortgage default insurance applies. In Canada, the minimum down payment is 5% on the first $500,000 of a home’s purchase price, and 10% on any amount above that (up to the $1.5 million insured mortgage cap). Putting down less than 20% means you’ll need CMHC insurance, which adds a premium of 2.80% to 4.00% to your mortgage balance depending on your down payment percentage. Keep in mind that your savings target needs to cover more than the down payment — closing costs in Canada typically run 1.5–4% of the purchase price and must be paid in cash at closing, separate from your mortgage.

4. Debt ratios

Lenders calculate two ratios to determine how much of your income goes toward housing and debt. Your Gross Debt Service (GDS) ratio — mortgage payment, property taxes, heat, and 50% of condo fees — must not exceed 39% of gross income. Your Total Debt Service (TDS) ratio adds all other debt payments (car loans, lines of credit, student loans, minimum credit card payments) and must not exceed 44%. These ratios are calculated at the stress test qualifying rate, not your actual contract rate — which is why they matter so much.

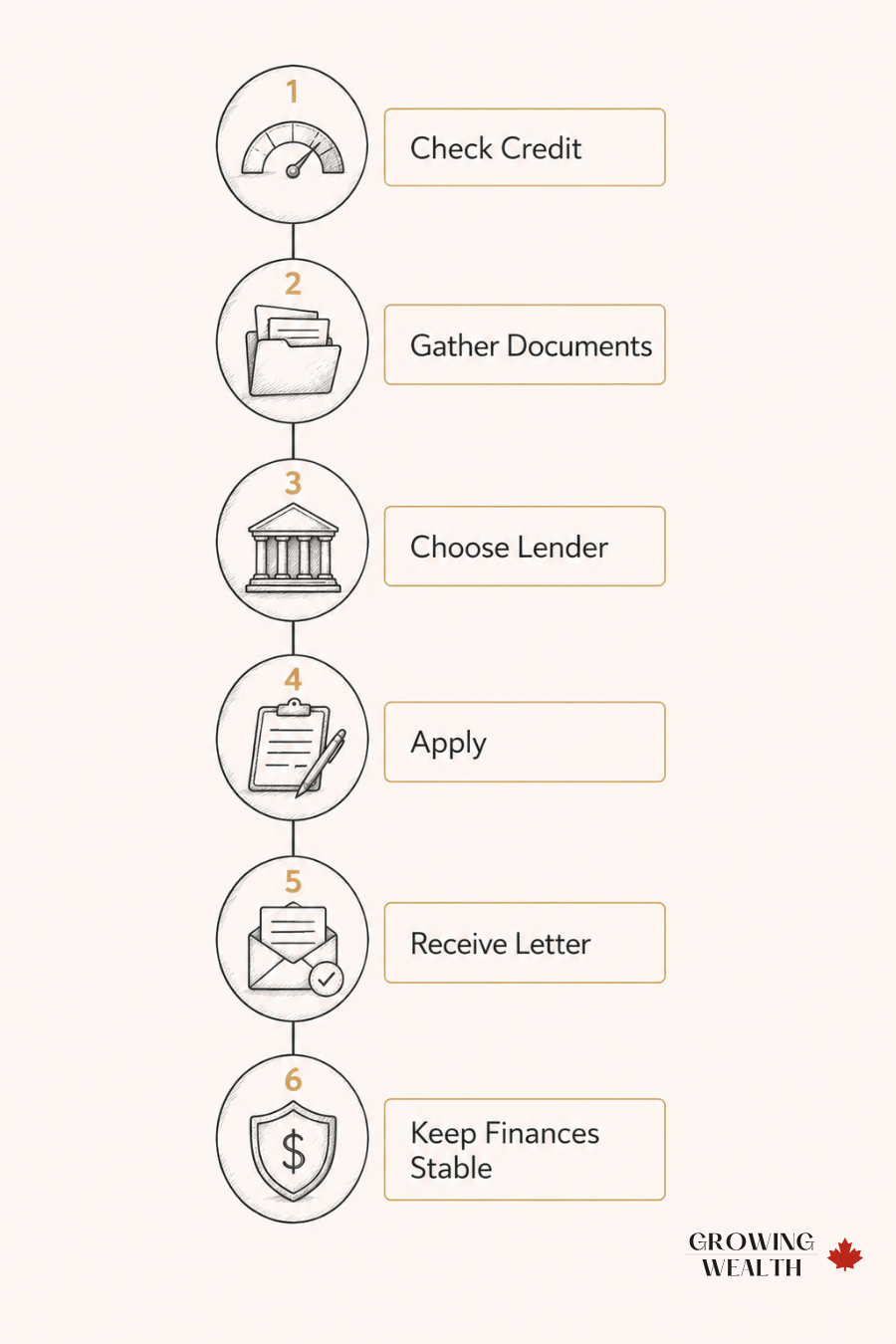

The Pre-Approval Process, Step by Step

Before a lender pulls your credit, pull it yourself. You’re entitled to a free credit report from Equifax and TransUnion. Review it for errors — incorrect late payments or accounts that aren’t yours can lower your score without cause. Dispute any errors before applying. If your score is below 680, spend time improving it before starting the pre-approval process. See our guide on how to improve your credit score in Canada.

Missing documents are the most common cause of pre-approval delays. Collect everything before you apply — the full checklist is below. Having your package ready means a broker or bank can turn your pre-approval around in as little as 24–48 hours.

This is a real decision with tradeoffs — see the full breakdown below. Either way, it’s worth getting more than one quote. A 0.25% difference in rate on a $500,000 mortgage saves roughly $7,200 over a five-year term.

Your lender or broker will review your documents, run a hard credit check, and assess your debt ratios using the stress test qualifying rate. They’ll come back with a maximum pre-approved amount and the rate they can hold for you. If applying to multiple lenders within a 14–30 day window, the multiple credit inquiries typically count as a single inquiry for scoring purposes.

Your pre-approval letter outlines your maximum loan amount, the rate being held, and the expiry date (90–120 days). Use this as your house-hunting budget ceiling — but consider buying below it, not at it. The pre-approved amount is the maximum the lender will lend, not a recommendation to borrow that much.

From the moment you’re pre-approved until your mortgage closes, avoid any major financial changes. Don’t take on new debt, make large purchases on credit, change jobs, or move significant amounts of money between accounts without being able to explain the transfer. Lenders re-verify your situation before final approval — a changed TDS ratio can disqualify you even after pre-approval.

Documents You’ll Need

Income Verification

- Two most recent pay stubs (salaried employees)

- Letter of employment confirming position, salary, and employment length

- Last two years of T4 slips

- Last two years of T1 generals (Notices of Assessment) — required for self-employed

- Business financial statements (if self-employed, typically last 2 years)

Down Payment Verification

- Last 90 days of bank statements showing down payment funds

- RRSP or TFSA statements if using registered savings

- Gift letter (if receiving money from family) signed and dated

- FHSA withdrawal documentation if applicable

Identity and Existing Debt

- Government-issued photo ID (passport or driver’s licence)

- Statements for any existing mortgages, loans, or lines of credit

- Most recent credit card statements

- Rental history or current lease agreement (if applicable)

If you plan to use your FHSA or the RRSP Home Buyers’ Plan toward your down payment, include statements for both. Lenders need to confirm the funds are available and accessible. Read our guide on how to save for a down payment using the FHSA and HBP if you haven’t mapped this out yet.

The Mortgage Stress Test Explained

The stress test is a federally mandated rule under OSFI’s Guideline B-20. It requires lenders to qualify you at a rate significantly higher than the one you’ll actually pay — proving you could still afford your mortgage if rates rose. OSFI confirmed in January 2026 that the stress test rules remain unchanged.

The qualifying rate is the higher of two values: your contract rate plus 2%, or the 5.25% floor. With current 5-year fixed rates sitting around 4.04–4.29%, the floor is irrelevant for most buyers right now — the contract rate plus 2% dominates, producing a qualifying rate of roughly 6.04–6.29%.

Based on GDS ≤ 39%, 25-year amortization, $500/month estimated property taxes and heat. Illustrative only — your figures will vary.

The stress test typically reduces your maximum mortgage by 20–25% compared to qualifying at your actual rate. This is not a reason to avoid getting pre-approved — it’s simply the reality of what you’ll qualify for, and knowing it early prevents the frustration of falling in love with a home outside your actual range.

A few groups are exempt or have different rules. Provincially regulated credit unions are not subject to OSFI’s B-20 guideline and may apply more flexible qualifying standards — sometimes at the contract rate alone. And as of November 2024, borrowers renewing an existing mortgage with the same lender no longer need to pass the stress test, provided the loan amount and amortization remain unchanged. This change gives renewing borrowers more flexibility to stay with their current lender.

To understand how mortgages work in Canada more broadly — including how your payment splits between interest and principal over time — our mortgage basics guide walks through the full picture.

Broker vs. Bank: Which Should You Use?

| Factor | Mortgage Broker | Bank Directly |

|---|---|---|

| Rate access | Shops 50+ lenders — often finds lower rates | One lender’s rates only |

| Cost to you | Usually free (paid by lender) | Free |

| Credit inquiries | One submission can reach multiple lenders | Each bank runs its own inquiry |

| Product range | Broader — includes B lenders and credit unions | Limited to that bank’s products |

| Relationship | Independent — works for you | Works for the bank |

| Best for | Most buyers, especially first-timers or complex situations | Buyers with existing bank relationship or strong preference |

- Access to rates your bank won’t offer you directly

- One application reaches many lenders

- Useful if your situation is complex (self-employed, lower credit, high debt)

- Brokers are regulated and must act in your interest

- Existing relationship may unlock loyalty rates

- Bundling mortgage with other banking products can have perks

- Some buyers prefer one point of contact for all finances

- Certain bank-exclusive products not available through brokers

For most first-time buyers, a broker is worth trying first. The rate difference on a $500,000 mortgage over five years can be meaningful, and brokers are experienced at handling the documentation and stress test calculations. That said, it’s not either/or — you can get quotes from both and compare.

Where to Keep Your Down Payment While You Wait

Once you know your pre-approved amount and have started house hunting, your down payment funds need to be liquid, safe, and earning something while they wait. Lenders will ask for 90 days of bank statements to verify the source of your down payment, so avoid moving the money around unnecessarily.

A high-interest savings account (HISA) is the right place for down payment savings you’ll need within the next one to two years. The money is accessible, protected up to CDIC limits, and earns a meaningful rate without any market risk. Investing down payment savings in the stock market is a risk most buyers shouldn’t take — a 15% portfolio drop six months before closing is not a recoverable situation.

EQ Bank’s savings account consistently offers one of the highest HISA rates in Canada with no monthly fees, making it a straightforward place to park your down payment while you search.

Open an EQ Bank account →If your purchase is still 12–18 months away, your FHSA and TFSA are worth maximizing first — both allow tax-sheltered growth and can be withdrawn for a home purchase under the right conditions. Our down payment savings guide covers the FHSA and Home Buyers’ Plan strategy in detail.

After Pre-Approval: What Comes Next

A pre-approval is valid for 90–120 days depending on the lender. If your rate hold expires before you find a home, you’ll need to reapply — which means another credit check and updated documents. If rates have risen in the meantime, your new rate will reflect current market conditions. This is why timing your pre-approval to roughly 90–120 days before you expect to buy is more useful than doing it six months out.

Once you find a property and your offer is accepted, the lender will move to full approval. This involves ordering an appraisal of the property to confirm its value supports the mortgage amount, verifying that your financial situation hasn’t changed since pre-approval, and finalizing the mortgage terms. If you used a variable rate pre-approval, you’ll also lock in your choice of fixed vs. variable at this stage. Our guide to fixed vs. variable mortgages in Canada can help you work through that decision.

Understanding how much house you can actually afford — factoring in property taxes, utilities, and maintenance beyond the mortgage payment — is worth doing before you start making offers, not after.

The Bottom Line

The Bottom Line

Get pre-approved before you start seriously house hunting — not after you’ve found something you want. The process takes a few days with documents in hand, locks in a rate for up to 120 days, and gives you a realistic number to shop within rather than a rough guess.

For most buyers, working with a mortgage broker is worth trying first. The rate access across 50+ lenders typically produces better terms than a single bank’s posted rate, and the process is free to you. If you already have a strong banking relationship, get a broker quote first and then compare — you can always go back to your bank if they match or beat it.

The stress test reduces your maximum mortgage by roughly 20–25% compared to your actual contract rate. Build your house-hunting budget around that number, not the maximum the lender approves. The difference is your financial breathing room.Frequently Asked Questions

Yes, but minimally and temporarily. A full pre-approval requires a hard credit inquiry, which may lower your score by 5–10 points. The effect typically fades within a few months. If you apply to multiple lenders within a 14–30 day window, those inquiries usually count as a single inquiry for scoring purposes — so shopping around doesn’t compound the impact significantly.

With a complete document package, a broker can often turn around a pre-approval in 24–48 hours. Banks may take 2–5 business days depending on their workload and whether they need to verify anything with your employer or financial institution. Delays almost always come down to missing documents, so having everything ready upfront matters.

Yes, but the process requires more documentation. Lenders use your declared income on your tax returns — two years of T1 generals and Notices of Assessment are standard. If you’ve aggressively minimized your taxable income to reduce taxes, your qualifying mortgage amount will be lower than your actual earnings might suggest. Some lenders offer stated-income programs for self-employed applicants with a 20% or greater down payment, though rates may be higher. A mortgage broker with experience in self-employed files is often the right starting point.

You’ll need to reapply. This means another hard credit inquiry and updated documents. If rates have risen since your original pre-approval, your new rate will reflect current market conditions — the previous rate hold no longer applies. If rates have fallen, you’ll benefit from the lower rate. Timing your pre-approval to roughly 90–120 days before you plan to buy is more effective than applying too early.

No. A pre-approval is conditional. The lender still needs to appraise the property you choose — if the appraised value comes in lower than the purchase price, your mortgage amount may be reduced. The lender also re-verifies your financial situation before final approval. Changes to your income, employment, credit, or debt load between pre-approval and closing can affect your final approval. Avoid major financial changes during this period.

It can happen in either order, but getting pre-approved first is generally better. Knowing your actual budget before working with an agent means you won’t waste time looking at homes outside your range — and real estate agents take pre-approved buyers more seriously. Many agents will ask for proof of pre-approval before spending significant time with a buyer in a competitive market.

Yes to both. Under the RRSP Home Buyers’ Plan, first-time buyers can withdraw up to $35,000 from their RRSP tax-free for a home purchase (the amount must be repaid over 15 years). The FHSA allows first-time buyers to contribute up to $8,000 per year (lifetime limit $40,000) and withdraw the full amount tax-free for a qualifying home purchase with no repayment required. You can combine both. Include statements for any accounts you plan to use when submitting your pre-approval documents.

The Gross Debt Service (GDS) ratio measures how much of your gross income goes toward housing costs: mortgage payment (at the stress test rate), property taxes, heating, and 50% of any condo fees. The maximum is 39%. The Total Debt Service (TDS) ratio adds all your other debt payments — car loans, student loans, credit cards, lines of credit — to those housing costs. The maximum is 44%. Both ratios are calculated at the stress test qualifying rate, not your actual contract rate. If your TDS is close to 44%, paying down existing debt before applying can meaningfully increase your maximum mortgage amount.

Ready to understand the full home-buying journey? Read Canadian Home Ownership: From First-Time Buyer to Mortgage Renewal — a complete roadmap from saving for a down payment through to owning your home outright.