Registered Accounts

Registered Accounts

This piece of advice gets repeated so often in Canadian personal finance that most people accept it without question. It sounds logical. And for a small slice of Canadians, it is.

The problem is that this advice requires you to predict something nobody actually knows — where tax brackets and rates will sit 20, 30, or 40 years from now, and exactly what your income will look like when you get there. For most Canadian families, that’s not a calculation. It’s a guess.

This article makes the case that for the majority of working Canadians, the right answer isn’t TFSA or RRSP. It’s both — and here’s how to think about which gets priority.

The Standard Advice Assumes Too Much

The “lower bracket in retirement” logic works if three things are true simultaneously:

- You know what your income will be in retirement

- You know what the tax brackets will look like at that point

- You know how other income sources (CPP, OAS, a pension, part-time work) will interact with your withdrawals

Most Canadians can’t confidently check any of those boxes — especially not 30 years out.

Tax policy has changed significantly across every decade in Canadian history. Bracket thresholds shift. Rates adjust. New rules appear (the OAS clawback didn’t always exist in its current form). Inflation quietly pushes nominal income higher even when purchasing power stays flat.

If you’re 35 today earning $85,000, you genuinely don’t know whether your retirement income will land you in a higher or lower bracket when you’re 68. And anyone who tells you they do know is either working with a very specific and unusual situation — or oversimplifying.

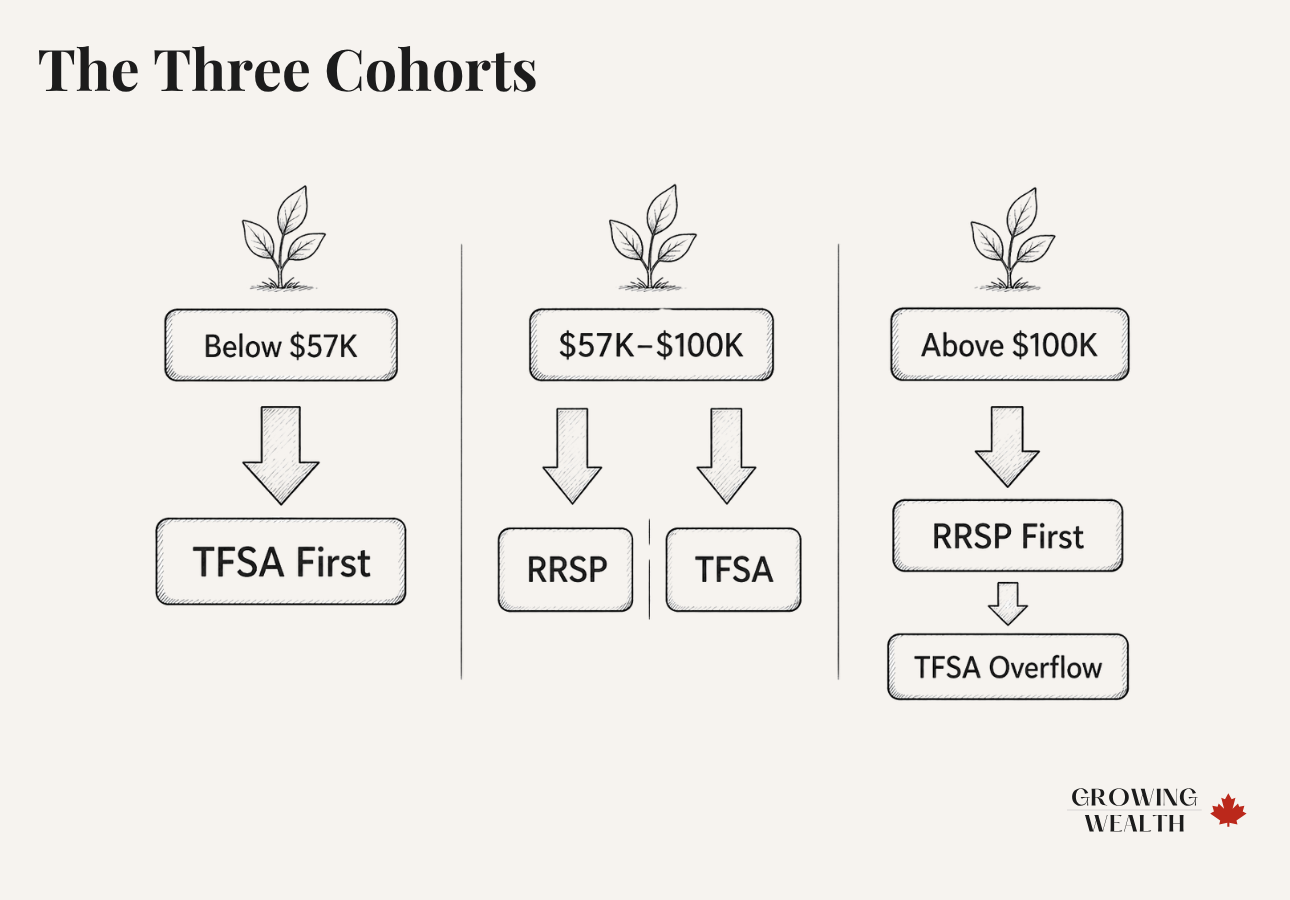

The Three Cohorts (And Which One You’re In)

Rather than treating this as a binary choice, it helps to think about three distinct groups.

If your income today sits below the top of the lowest federal tax bracket — roughly $57,000 in 2025 — there’s a reasonable argument that your retirement income will be higher in real terms than your current income, especially once CPP and OAS kick in.

In this case, deferring tax via RRSP may mean you pay more tax later, not less. There’s also a more immediate problem: the RRSP deduction isn’t worth much right now. At $45,000 in Ontario, a 10% RRSP contribution — $4,500 — returns approximately $880 on your tax return. That’s a modest benefit in exchange for locking money into an account where every dollar withdrawn in retirement will be taxed as income. The TFSA is likely the better primary account for this group, because withdrawals are completely tax-free at any income level, now or in retirement.

That said, small RRSP contributions aren’t necessarily wrong if you expect your income to rise significantly — the deduction can be saved and applied in a future high-income year when it’s worth more.

If you’re earning well above $100,000 today, the math does favour RRSP more clearly — and not just in retirement. You’re getting a deduction at a high marginal rate now — which directly reduces your taxable income for the year (see How RRSP Contributions Reduce Your Taxes). At $130,000 in Ontario, a 10% RRSP contribution — $13,000 — returns approximately $5,640 on this year’s tax return at a combined marginal rate of 43.41%. That’s an immediate, tangible benefit that compounds the long-term advantage of tax-deferred growth.

The case for RRSP in this cohort works on both timelines: it pays off now, and it’s likely to pay off in retirement too, since even with CPP, OAS, and investment income, you may well land in a lower effective rate.

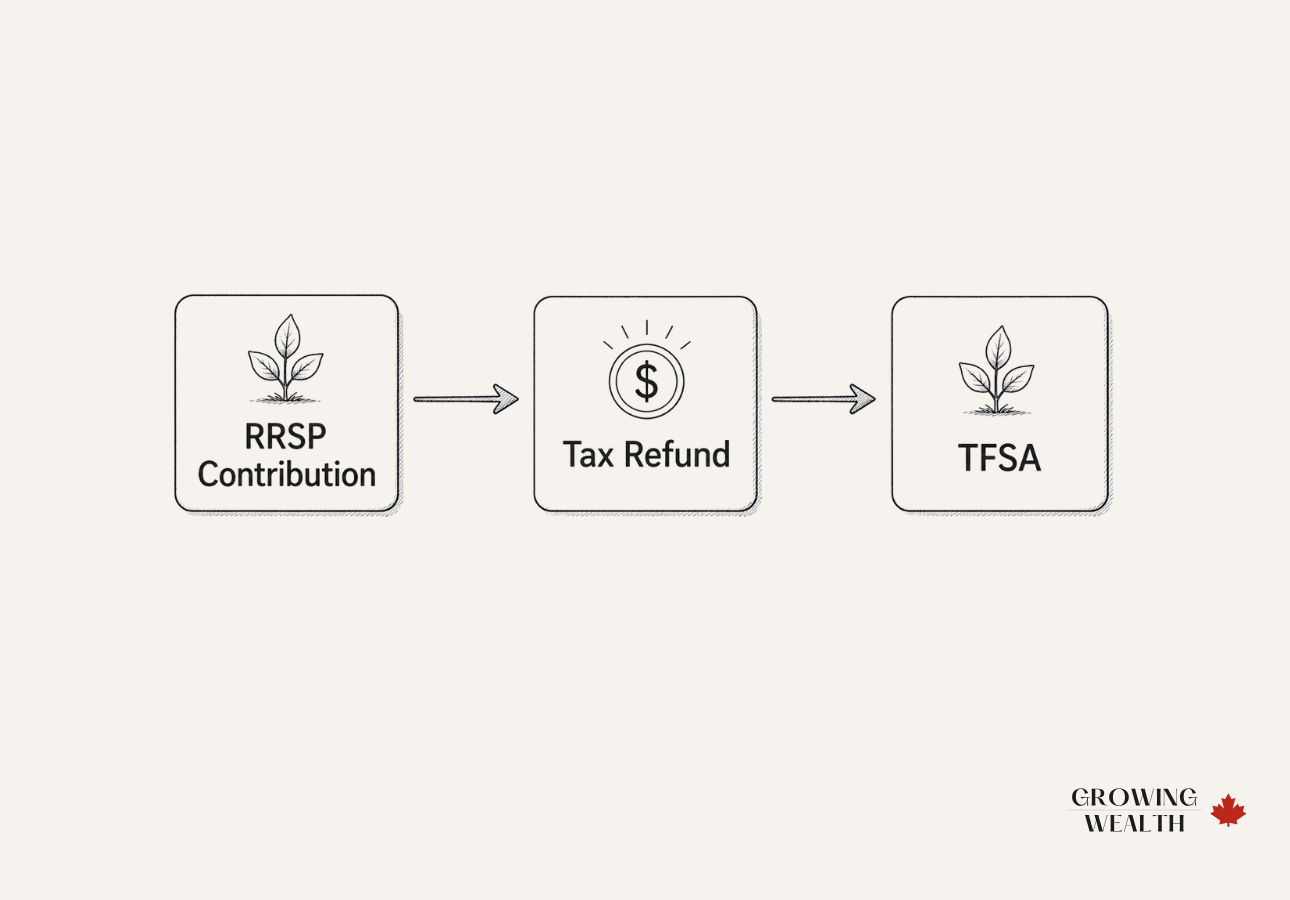

That ~$5,640 refund doesn’t have to sit in a chequing account. Redirecting it into your TFSA is one of the most efficient moves available to high earners — you’ve already captured the RRSP deduction at a high marginal rate, and now the refund itself is compounding tax-free. It’s a two-account strategy funded by a single year’s contribution. See What to Do With Your Tax Refund for how to put it to work.

This is where most Canadian families actually live. And this is the group for whom the standard advice most consistently fails.

At $75,000 or $90,000 today, you genuinely cannot know whether your retirement income — factoring in CPP, OAS, a possible pension, RRIF minimums, and part-time work — will put you above or below your current bracket. The variables are too many, the timeline too long, and the future tax environment too uncertain.

The current-year picture is equally ambiguous. At $80,000 in Ontario, a 10% RRSP contribution — $8,000 — returns approximately $2,370 on your tax return. That’s real money, but not so compelling that it should determine your entire long-term strategy.

For this cohort, trying to pick one account is a bet. Splitting contributions across both is a hedge — and hedging is almost always the smarter move when the future is genuinely uncertain on both the immediate and retirement timelines.

One practical approach for this cohort: contribute enough to your RRSP to drop your taxable income to the next lower bracket threshold, capturing the maximum refund at your current marginal rate, then direct that refund directly into your TFSA. The refund itself becomes your TFSA contribution — effectively funding both accounts from a single savings decision. It’s not an either/or decision — it’s a sequencing one. See What to Do With Your Tax Refund for how to deploy it.

To see how sharply the current-year value of an RRSP contribution varies across cohorts, consider this side-by-side at 10% of income in Ontario (2025):

| Income | 10% Contribution | Marginal Rate | Approx. Refund | Verdict |

|---|---|---|---|---|

| $45,000 | $4,500 | 19.55% | ~$880 | Low — prioritize TFSA |

| $80,000 | $8,000 | 29.65% | ~$2,370 | Moderate — split |

| $130,000 | $13,000 | 43.41% | ~$5,640 | High — RRSP first |

Combined federal and Ontario marginal rates for 2025. Actual refund depends on individual tax situation.

The Concrete Risk Most Advisors Underemphasize: The OAS Clawback

Beyond the general uncertainty argument, there’s one specific, calculable risk that makes over-relying on RRSP genuinely dangerous for middle-income earners: the OAS recovery tax.

Old Age Security starts being clawed back at a net income of approximately $90,997 in 2025, according to the Government of Canada’s OAS recovery tax rules. Above that threshold, you lose 15 cents of OAS for every dollar of income — which effectively adds 15% to your marginal tax rate at that income range.

Here’s where it becomes a trap: RRIF withdrawals (the mandatory withdrawals you must take from your converted RRSP starting no later than age 72) count as taxable income. If you’ve aggressively deferred into an RRSP for 30 years, your RRIF balance may force withdrawals that push you into or well above the clawback zone — regardless of what you actually need to spend.

TFSA withdrawals, by contrast, don’t count as income at all. They don’t affect your OAS. They don’t affect income-tested benefits. They’re invisible to the CRA for purposes of calculating your net income.

A family that splits contributions across both accounts through their working years arrives at retirement with more control. They can draw from their TFSA strategically to keep net income below the clawback threshold — something an RRSP-only saver cannot do.

The CPP + OAS + RRIF Minimums Problem

Related to the clawback risk is a broader issue that catches people off guard: in retirement, you may have less control over your income than you expect.

CPP and OAS are not optional. Once you’re receiving them, that income flows whether you need it or not. If you also have mandatory RRIF minimums forcing withdrawals from a large RRSP balance, your taxable income can end up higher in retirement than it ever was while you were working — even if your actual spending is modest.

This isn’t a fringe scenario. It’s a predictable outcome for middle-income earners who saved diligently into RRSP over a 30+ year career. The solution isn’t to save less — it’s to balance where those savings sit.

A Worked Example: Two Versions of the Same Family

Meet a couple in their mid-30s with a combined household income of $95,000. They contribute $10,000 per year to registered accounts and keep this up for 30 years. Assume their investments grow identically in either scenario.

RRSP-Focused

They put most of their contributions into RRSP, taking the deductions each year. By retirement, they have a large RRSP/RRIF balance. Their RRIF minimums, combined with CPP and OAS for two people, put their combined household net income at approximately $105,000 — pushing them into or near the OAS clawback zone and into a higher marginal bracket than they ever paid during their working years.

Split Approach

They divide contributions roughly 60/40 between RRSP and TFSA across their working years. In retirement, their RRIF minimums are lower because the balance is smaller. They draw from their TFSA to cover the income gap without triggering additional taxable income. Combined household net income stays around $80,000–$85,000 — below the clawback threshold, with a lower effective tax rate than Version A.

Same total savings. Same investment returns. Meaningfully different tax outcome — simply because of where the money sat.

What About the FHSA?

If you’re saving toward a first home, the First Home Savings Account adds a third registered account worth knowing about. It combines the best features of both: contributions are tax-deductible like an RRSP, and withdrawals for a qualifying home purchase are tax-free like a TFSA.

If you’re eligible and not yet a homeowner, the FHSA deserves priority before either RRSP or TFSA simply because of how powerful that combination is. You can learn more in the FHSA Guide.

How to Prioritize If You Can’t Maximize Both

Most Canadian families aren’t in a position to max both accounts every year — and that’s fine. Here’s a practical framework:

If your income is below ~$57,000: Prioritize TFSA. Consider small RRSP contributions only if you anticipate a significant income increase in coming years — you can carry forward the deduction and apply it in a higher-income year when it’s worth more.

If your income is $57,000–$100,000: Split contributions, with the balance depending on your specific marginal rate. A rough starting point is 60% RRSP / 40% TFSA, adjusted as your income changes. In strong income years — a bonus, a promotion — consider directing more to RRSP to capture a larger deduction while your rate is elevated.

If your income is above $100,000: Prioritize RRSP up to your contribution limit, then direct remaining savings to TFSA. The current-year deduction is working hard for you at this income level — don’t leave it on the table. But don’t leave TFSA room unused either.

If you have an employer pension: Be careful with RRSP. A Pension Adjustment (PA) reduces your available RRSP room, and a strong pension already provides the income-deferral effect. TFSA often becomes more important for pension members.

| Your Situation | Primary Account | Secondary Account |

|---|---|---|

| Income below $57K | TFSA | Small RRSP if income rising |

| Income $57K–$100K | Split ~60/40 RRSP/TFSA | Adjust as income changes |

| Income above $100K | RRSP to limit | TFSA with remaining room + refund |

| Strong employer pension | TFSA | RRSP with caution |

| Saving for first home | FHSA first | Then TFSA or RRSP |

One common mistake worth flagging: contributing to an RRSP primarily to get a tax refund. The refund is a consequence of a good decision — not a reason to make it. If your marginal rate is low, the refund is modest, and you may be deferring tax into a higher-rate future. Make the account choice based on your income and long-term picture first. The refund follows from that.

The Bottom Line

The standard advice — RRSP if you’ll be in a lower bracket, TFSA if you won’t — is not wrong for everyone. It’s just incomplete for most people.

If you’re confidently in a high income bracket today, RRSP-first with TFSA overflow is likely the right call. If you’re clearly in a low bracket today, TFSA-first makes sense. But if you’re somewhere in the middle — which describes the majority of Canadian families — you genuinely don’t have enough information to bet your retirement tax strategy on a single account.

Diversifying your tax exposure across RRSP and TFSA isn’t admitting you don’t know what you’re doing. It’s the financially sophisticated acknowledgment that the future is uncertain, and that flexibility has real, measurable value.

The goal isn’t to pay the least tax this year. It’s to pay the least tax across your entire lifetime — and a split strategy gives you the tools to manage that as your situation evolves.

For a deeper look at how RRSP and TFSA compare side by side, see RRSP vs TFSA: Which Is Right for You? For a full breakdown of how each account works, visit the TFSA Guide and the RRSP Guide.

Frequently Asked Questions

Yes. They are entirely separate accounts with independent contribution limits. Your TFSA room accumulates based on the annual limit set by the government (currently $7,000/year for 2025) plus any unused room from prior years. Your RRSP room is 18% of your previous year’s earned income, up to the annual maximum, minus any pension adjustment — you can check your available room on the CRA My Account portal, or read more about how it’s calculated in RRSP Contribution Room Explained. Contributing to one has no effect on the other.

Use the income framework above as your guide. Below $57,000, lean TFSA. Above $100,000, lean RRSP. In the middle, the TFSA is often the safer default because of its flexibility — withdrawals don’t affect income-tested benefits, and unused room is never lost. You can always shift more toward RRSP as your income grows.

It depends on your income and marginal rate today. For most middle-income earners, a split is better than trying to max one first. If you’re in the $57K–$100K range and truly can only pick one, the TFSA’s flexibility and absence of mandatory withdrawals make it a strong default.

Yes — just differently than an RRSP. You don’t get a deduction when you contribute, but everything that grows inside the TFSA — dividends, capital gains, interest — is completely tax-free when withdrawn. The RRSP defers tax. The TFSA eliminates it on the growth. Both are genuinely valuable tools.

You must convert your RRSP to a Registered Retirement Income Fund (RRIF) by the end of the year you turn 71. From that point, you’re required to withdraw a minimum percentage each year, and those withdrawals are fully taxable as income. The minimum percentage increases as you age, which is why a very large RRIF balance can create a tax problem in your late 70s and 80s.

Yes. The idea of spreading assets across accounts with different tax treatments — taxable accounts, tax-deferred accounts (RRSP/RRIF), and tax-free accounts (TFSA) — is a well-established strategy in Canadian financial planning. It gives you flexibility to manage your taxable income in retirement rather than being locked into a single withdrawal structure.

They might. In that case, someone who deferred heavily into RRSP might pay less tax than expected. This is the scenario where RRSP-first works out best. But betting on lower future tax rates requires you to predict government policy across multiple decades — a bet most financial planners wouldn’t recommend making with your entire retirement savings. Diversifying hedges against both outcomes.

Ready to put this into action? Read FHSA vs TFSA vs RRSP: Which Should You Use? — the decision framework that shows you exactly how to allocate between all three accounts based on your income and goals.