Prepaid cards vs secured credit cards — they look almost identical in your wallet. Both carry a Visa or Mastercard logo. Both work for online purchases, subscriptions, and everyday spending. But one of them builds your credit history and the other does nothing for your score, no matter how long or responsibly you use it. That difference has real consequences for your financial future in Canada.

This guide breaks down exactly how each card works, who each one is for, and how to use a secured card strategically to build or rebuild your credit as efficiently as possible.

This article contains affiliate links. We may earn a commission if you open an account — at no cost to you. We only recommend products we’ve researched and trust.

In This Article

- The Quick Answer: Which One Should You Get?

- What Is a Prepaid Credit Card?

- What Is a Secured Credit Card?

- Prepaid vs Secured: Side-by-Side Comparison

- The Best Secured Credit Cards in Canada (2026)

- How Long Does It Take to Build Credit?

- How to Build Credit Faster with a Secured Card

- Real-World Example: Rebuilding from a 520 Score

- Which One Should You Choose?

- Once Your Credit Is Built: What’s Next?

- Frequently Asked Questions

The Quick Answer: Which One Should You Get?

If your goal is to build or rebuild a credit score, get a secured credit card. Full stop. Prepaid cards are useful spending tools, but they are invisible to Equifax and TransUnion — they will never move your score.

| Your Situation | Verdict |

|---|---|

| Your goal is building credit | Secured card. Every on-time payment is reported to the bureaus. A prepaid card reports nothing. |

| You want a card with no credit risk | Prepaid card. You spend your own money — no debt, no interest, no score impact. |

| You’re new to Canada with no credit history | Secured card immediately. Open one in your first month — you’ll have a meaningful credit file within 12–18 months. |

| You’re rebuilding after financial difficulty | Secured card. Most issuers approve applicants with any credit score — the deposit eliminates the lender’s risk. |

| You want a spending card for a teenager | Prepaid card. No debt risk, fixed spending limits, no credit history required. |

What Is a Prepaid Credit Card?

A prepaid card is a spending card you load with your own money before using it. Add $200, spend up to $200. When the balance runs out, you reload and start again. Popular prepaid options in Canada include KOHO, Wealthsimple Cash, and Stack.

Despite the name, a prepaid card is not actually a credit card. You’re not borrowing anything. There’s no credit limit, no monthly statement, and no lender involved. It functions more like a reloadable gift card — accepted anywhere Visa or Mastercard is used, but with none of the credit-building mechanics that matter for your financial profile.

Prepaid cards are not reported to Equifax or TransUnion. Using one for years will not move your credit score a single point in either direction.

When a prepaid card makes sense

- You want a card for online shopping but aren’t ready to take on credit

- You’re setting hard spending limits for yourself or a teenager

- You’ve been declined even for a secured card

- You don’t have a deposit available right now

One exception worth knowing: KOHO offers a paid Credit Building add-on ($10/month) that reports to Equifax. This is a workaround, not a true credit account — and at $120/year, it costs more than most secured cards with no annual fee. If your goal is building credit, a secured card is a more effective and usually cheaper path.

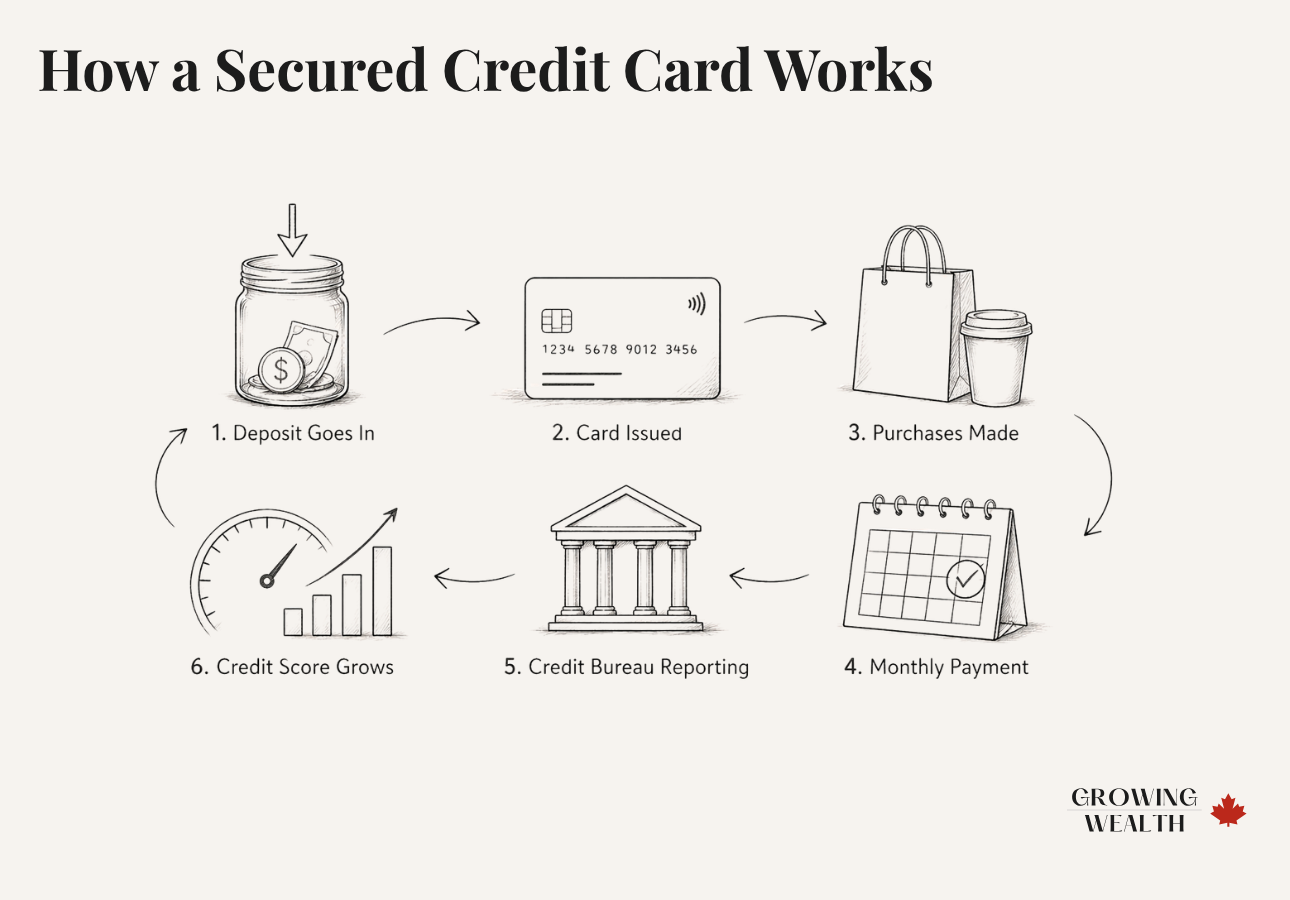

What Is a Secured Credit Card?

A secured credit card works like a regular credit card in almost every way — with one key difference. Before the card is issued, you put down a refundable security deposit. That deposit becomes your credit limit. Put down $200, and you have a $200 credit limit. Put down $500, and you have a $500 limit. The deposit sits safely with the issuer; it’s not used to pay your purchases.

You spend on the card, receive a monthly statement, and pay it off — exactly like any other credit card. What makes secured cards powerful for credit building is that the issuer reports your payment history to Equifax and TransUnion every month. To the credit bureaus, a secured card looks identical to a regular credit card. Every on-time payment is recorded. Every month you keep your utilization low is recorded. Over time, this builds a real credit history.

Who qualifies for a secured card?

Secured cards are designed for people who can’t get approved for a regular credit card. Most issuers in Canada offer near-guaranteed approval for residents over 18, regardless of credit score. Some don’t run a credit check at all. The deposit is what protects the lender — not your credit history.

Prepaid vs Secured: Side-by-Side Comparison

| Prepaid card | Secured credit card | |

|---|---|---|

| How it works | Spend your own pre-loaded money | Borrow against your deposit; pay monthly |

| Deposit required | No | Yes — typically $50–$500+ |

| Credit check | None | Usually none or soft check |

| Builds credit history | No | Yes |

| Reports to bureaus | No | Yes (Equifax and/or TransUnion) |

| Interest charges | None | Yes, if you carry a balance |

| Risk of missed payments | None | Yes — missed payments hurt your score |

| Annual fee | Usually none | Varies: $0–$60/year |

| Best for | Budgeting, online purchases | Building or rebuilding credit |

The Best Secured Credit Cards in Canada (2026)

There are three secured cards worth considering, depending on your situation. All three report to the credit bureaus and offer near-guaranteed approval.

How Long Does It Take to Build Credit with a Secured Card?

The honest answer depends on where you’re starting and how consistently you use the card. Here’s a realistic picture for someone starting from zero or rebuilding after financial difficulty. The Financial Consumer Agency of Canada (FCAC) outlines the same core factors lenders use to evaluate your file.

Months 1–3

Your credit file is established or begins rebuilding. Scores may dip slightly as the new account opens, then stabilize. This is normal — the file is thin but it exists.

Months 6–12 — score range: 600–650

Consistent on-time payments and low utilization push your score into the 600–650 range. This is meaningful — it starts opening doors to entry-level unsecured cards.

Months 12–24 — score range: 650–700+

A score of 650–700+ becomes achievable. You can start applying for no-fee unsecured cards like the Tangerine Money-Back card or a PC Financial Mastercard.

For newcomers to Canada with no Canadian credit history, a secured card opened in your first month can build a meaningful credit file within 12–18 months — putting you in a strong position well before most people think it’s possible.

How to Build Credit Faster with a Secured Card

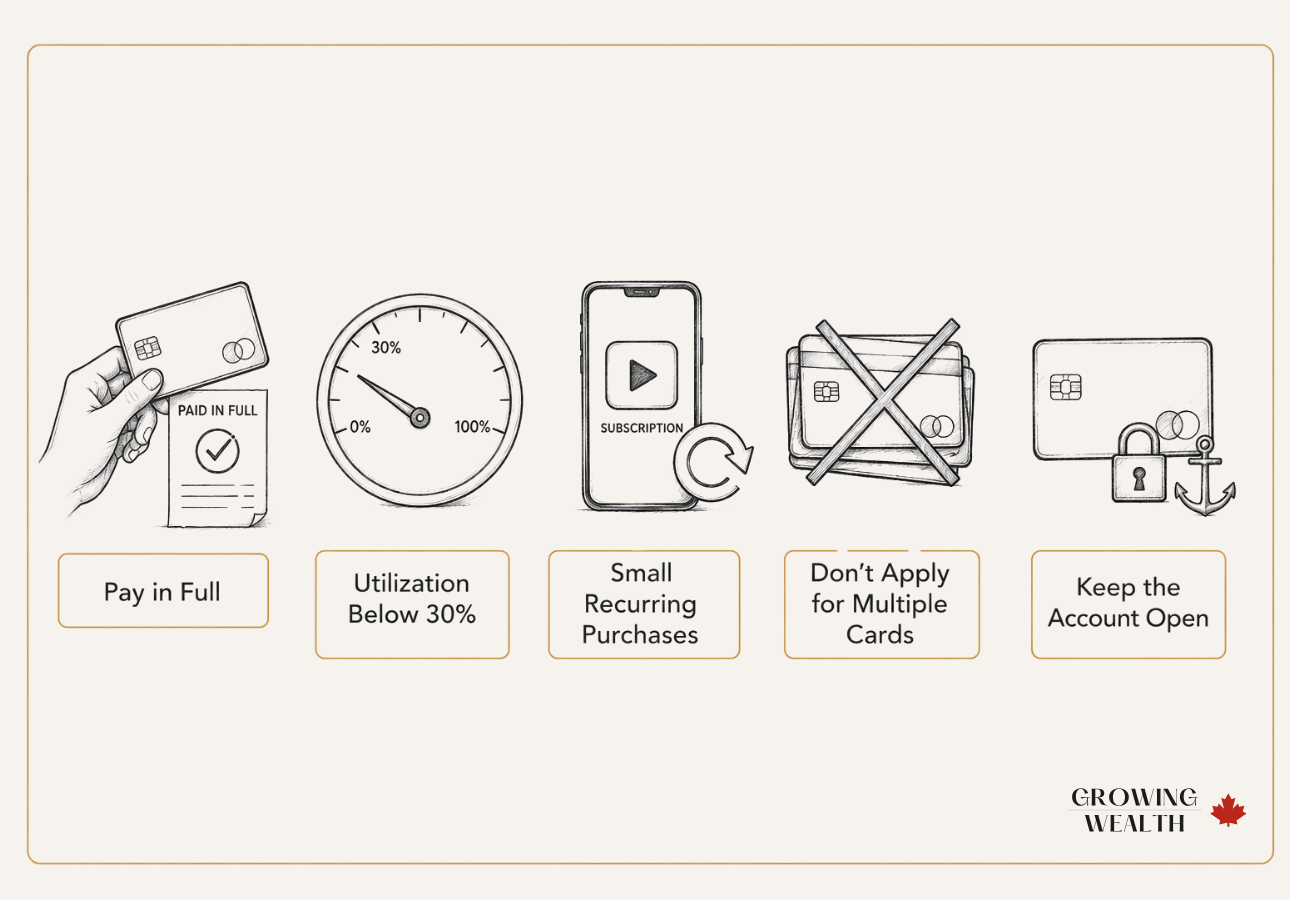

The card itself doesn’t build credit — your habits do. Here’s how to use a secured card strategically to reach a good credit score in Canada as efficiently as possible.

This is the single most important habit. Payment history makes up 35% of your credit score. Even one missed payment can set you back months. Set up automatic payments for at least the minimum, then manually pay the full balance before the due date to avoid interest charges.

Credit utilization accounts for about 30% of your score. On a $200 limit, keep your balance below $60. On a $500 limit, stay under $150. Start with $200 and spend $150/month, and you’re at 75% utilization even if you pay it off. Depositing $500 gives you breathing room.

The goal is to show regular, manageable borrowing activity. A monthly streaming subscription, your phone bill, or a weekly grocery run works well. You don’t need to charge a lot — you need to show consistent, responsible use over time.

Each credit application triggers a hard inquiry on your file. Multiple inquiries in a short period signals risk to lenders and can lower your score. Apply for one secured card, use it well for 6–12 months, then reassess your options.

Credit history length is a factor in your score. When you graduate to an unsecured card, consider keeping the secured card open with a small recurring charge — even a $5 subscription. Your deposit will be refunded when you eventually close it, but keeping the account open protects your credit age.

Real-World Example: Rebuilding from a 520 Score

A credit score of around 520 is low enough to be rejected for most regular cards, but not so damaged that recovery is out of reach. Here’s what a realistic rebuild looks like using the Neo Secured Mastercard with a $300 deposit.

Starting point: credit score ~520. Deposit: $300 on a Neo Secured Mastercard.

Month 1

Open Neo Secured Mastercard with a $300 deposit. Credit limit: $300. File established with both bureaus.

Score may dip slightly as new account opens — this is normal.

Months 1–6

Charge groceries and phone bill — $80–$100/month. Pay the full balance every month. Utilization stays around 30%.

6 months of perfect payment history accumulating.

Month 6

Score climbs to 580–600. Six months of on-time payments recorded. Entry-level options start opening up.

Month 12

Consistent use pushes score to 630–650. Now in range for entry-level unsecured cards.

Month 18

Score crosses 670. Apply for Tangerine Money-Back Mastercard — approved. Keep Neo card open on a small monthly charge.

Two accounts now open. Credit history growing on both.

Month 24

Two accounts with clean history. Score approaching 700. Access to cards that earn real rewards on everyday spending.

$300 deposit + consistent habits = a rebuilt credit file.

Which One Should You Choose?

Once Your Credit Is Built: What’s Next?

A secured card is a starting point, not a permanent home. Once your score reaches 650–680, you have options worth evaluating.

First, check whether your current secured card issuer will upgrade your account. Neo and Capital One both have upgrade pathways. In many cases, your deposit is refunded and your account history carries forward — protecting your credit age without requiring a new application.

If you decide to move to a new card, start with no-fee cards that reward everyday spending. Our roundup of the best no-fee credit cards in Canada covers the top options for 2026. Once your score is solidly above 700, compare rewards cards across our best credit cards in Canada guide to find what fits your spending patterns.

For a deeper look at what goes into your score and how to accelerate your progress, read our guides on understanding your credit score in Canada and how to improve your credit score.

The Bottom Line

If your goal is to build or rebuild credit, a secured card is the only tool that actually moves the needle. Prepaid cards are spending tools — useful, but invisible to the credit bureaus. The two are not interchangeable.

Start with the Neo Secured Mastercard if you want the lowest barrier to entry ($50 deposit, no credit check). Move to Home Trust if you can put down $500 and want to minimize fees. Pay your balance in full every month, keep utilization under 30%, and give it 12–18 months. The credit file you build in that time opens doors that stay closed without it.

Once your score reaches 650+, revisit the best no-fee credit cards in Canada — that’s your logical next step.Frequently Asked Questions

No. Prepaid cards are not reported to Equifax or TransUnion because you’re not borrowing money — you’re spending your own. Using a prepaid card, no matter how long or responsibly, will not change your credit score in either direction.

Yes. Most secured card issuers in Canada do not require any existing credit history. The deposit is what protects the lender — not your credit score. Neo’s secured card requires no credit check at all, making it one of the most accessible options available.

Deposit as much as you can comfortably set aside — not because a larger deposit builds credit faster, but because a higher credit limit makes it easier to keep your utilization low. Aim to keep your monthly spending below 30% of your limit. Starting with $200–$500 is practical for most people. If you can only deposit $50 with Neo, start there and increase it when you can.

Yes, if you carry a balance. Secured cards work exactly like regular credit cards — if you don’t pay your full balance by the due date, interest applies (typically 19.99%–29.99%). The way to avoid interest entirely is to pay your balance in full every month, which also maximizes your credit-building progress.

Most people can qualify for entry-level unsecured cards after 12–18 months of responsible secured card use, assuming on-time payments and low utilization throughout. A score of 650+ opens up options like the Tangerine card and PC Financial Mastercard. A score of 680–700+ opens up more rewards-focused options.

Yes. The security deposit on a secured card is fully refundable. When you close the account in good standing — or when the issuer upgrades you to an unsecured card — your deposit is returned. The timeline varies by issuer but is typically within 30–60 days of account closure.

Yes, and this is one of the most common use cases. After a bankruptcy discharge, a secured card is typically the fastest and most reliable way to start rebuilding. Most issuers don’t require a minimum credit score for approval. Expect your score to recover gradually over 2–3 years of consistent, responsible use — with meaningful progress visible within the first year.

Some companies — Neo Financial being the main example — offer both. Neo’s prepaid card (Neo Money) does not build credit. Neo’s secured card does. Despite coming from the same company and looking similar, they work very differently. Always confirm that the card you’re applying for is specifically labelled a “secured credit card” and that it reports to the credit bureaus.

Want to turn what you’ve just learned into lasting results? Read our guide to the best no-fee credit cards in Canada — the logical upgrade once your secured card has done its job.