Credit

Credit

This article contains affiliate links. We may earn a commission if you open an account — at no cost to you. We only recommend products we’ve researched and trust.

Your credit score is one of the most consequential numbers in your financial life — yet most Canadians have only a vague sense of what it actually measures, who calculates it, or what it’s costing them. It affects whether you’re approved for a mortgage, the interest rate you pay on a car loan, and in some cases whether a landlord accepts your rental application.

The frustrating part is that most of the factors that move your score are entirely within your control. The national average in Canada sits at around 680 — good enough for most approvals, but below the 720 threshold that unlocks the best mortgage rates. On a $500,000 mortgage, that gap can translate to tens of thousands of dollars in extra interest over a five-year term.

This guide covers everything you need: how scores are calculated, what the ranges actually mean for real products, how to check yours for free, and the fastest ways to move it in the right direction.

In This Article

- What Is a Credit Score in Canada?

- Credit Score Ranges in Canada

- Who Calculates Your Credit Score?

- How Credit Scores Are Calculated

- How to Check Your Credit Score for Free

- What Appears on Your Credit Report

- How Long Negative Information Stays on Your Report

- How Credit Scores Affect Real Financial Decisions

- How to Improve Your Credit Score

- Common Credit Score Myths

- The Bottom Line

- Frequently Asked Questions

What Is a Credit Score in Canada?

A credit score is a three-digit number between 300 and 900 that tells lenders how likely you are to repay borrowed money based on your financial history. The higher the number, the lower the risk you represent — and the better the terms you’ll receive on mortgages, loans, and credit cards.

In Canada, two organizations — Equifax and TransUnion — independently calculate your credit score using data reported by your lenders. Because not every lender reports to both bureaus, your Equifax score and your TransUnion score can differ by 20–50 points for the same person at the same time. This is normal. Neither score is “right.” What matters is that both scores are in good shape, because different lenders pull from different bureaus.

Credit scores affect more than just loan approvals. Landlords in competitive markets like Toronto and Vancouver regularly require scores above 660 for rental applications. Some employers run credit checks as part of background screening. Insurance companies in certain provinces factor credit history into premium calculations.

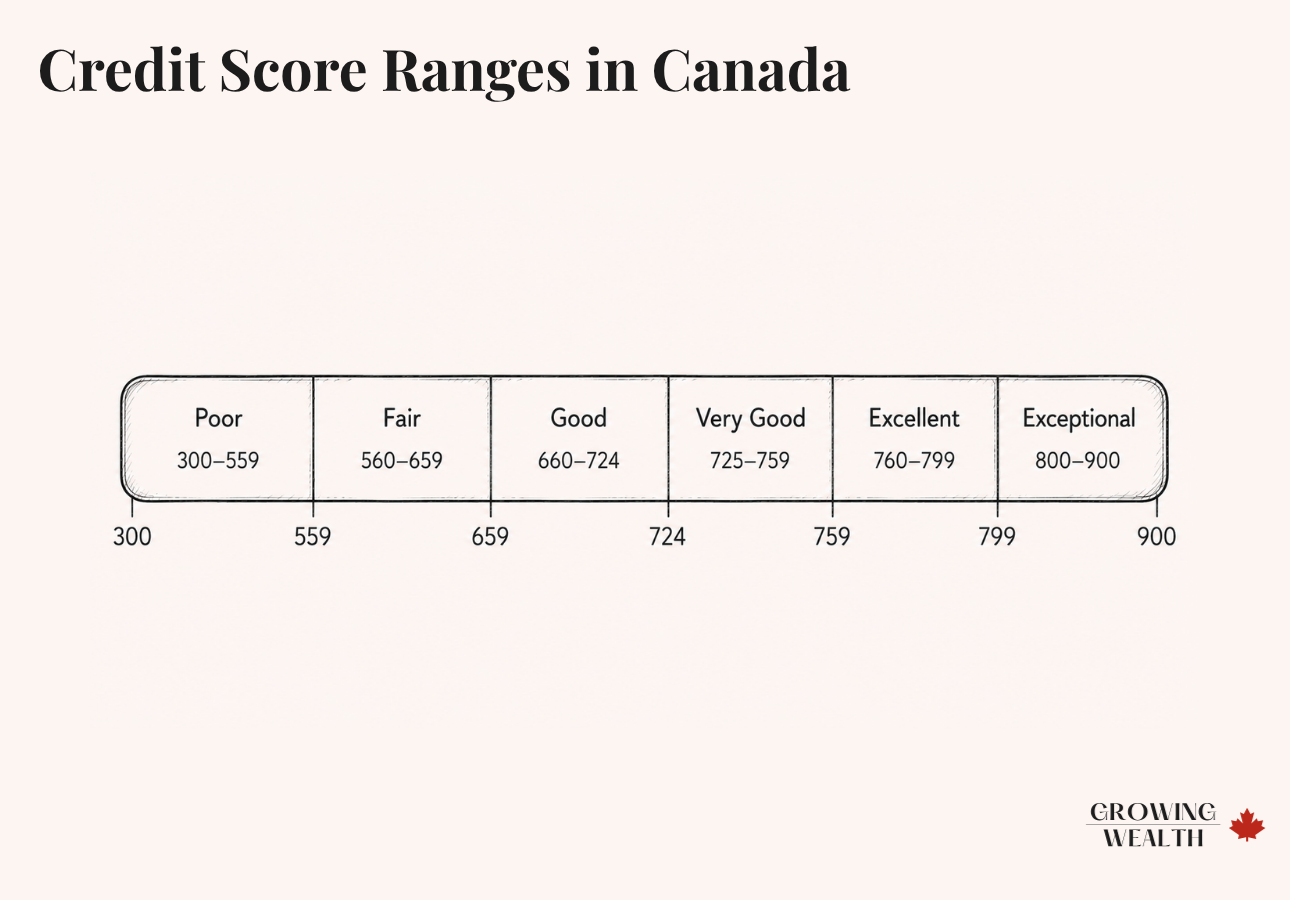

Credit Score Ranges in Canada

Both Equifax and TransUnion use the same 300–900 scale. The labels attached to ranges vary slightly by bureau and by lender, but the thresholds that determine your real-world borrowing options are consistent across the Canadian market.

| Range | Rating | What It Means in Practice |

|---|---|---|

| 800–900 | Exceptional | Best rates on all products; near-automatic approvals with A-lenders |

| 760–799 | Excellent | Preferred pricing; every mainstream product accessible |

| 725–759 | Very Good | Competitive rates; most products available at good terms |

| 660–724 | Good | Standard rates; full access to mainstream credit products |

| 560–659 | Fair | Higher rates; some products restricted; secured products may be required |

| 300–559 | Poor | Significant difficulty qualifying; subprime or secured products only |

The thresholds that matter most in practice: 600 is the minimum for a CMHC-insured mortgage. 680 is the effective floor for A-lender mortgage approvals. 720 is where most lenders offer their best pricing across all product categories. If you’re above 720, further gains are real but incremental. If you’re below 680, improving your score is one of the highest-return financial moves you can make.

The national average credit score in Canada is approximately 680 — solidly in the “Good” range, but below the 720 threshold required for the best mortgage rates. Most Canadians have scores between 650 and 750.

Who Calculates Your Credit Score?

Canada has two major credit bureaus: Equifax Canada and TransUnion Canada. They operate independently, collect data from different combinations of lenders, and calculate scores using their own proprietary models. The result is two separate credit files — and two separate scores — for every Canadian with a credit history.

| Feature | Equifax | TransUnion |

|---|---|---|

| Score range | 300–900 | 300–900 |

| Free monitoring tool | Borrowell | Credit Karma |

| Free annual report | Yes (by mail) | Yes (by mail) |

| Paid monitoring | $19.99/month | $19.99/month |

| Score update frequency (free tools) | Weekly | Weekly |

Because lenders may pull from either bureau — or both — a problem on one report can affect an application even if the other report is clean. Monitoring both scores is worth doing, and both can be tracked free of charge through third-party tools (covered in the next section).

The Financial Consumer Agency of Canada (FCAC) provides additional guidance on understanding your credit reports and how to dispute errors on either bureau’s file. You can request your full credit report from Equifax Canada or TransUnion Canada directly.

How Credit Scores Are Calculated

Both bureaus use proprietary models, but the five underlying factors and their approximate weights are publicly understood and consistent across both Equifax and TransUnion.

| Factor | Weight | What It Measures |

|---|---|---|

| Payment history | 35% | Whether you pay on time, every time |

| Credit utilization | 30% | How much of your available credit you’re using |

| Length of credit history | 15% | How long your accounts have been open |

| Credit mix | 10% | Variety of credit types (cards, loans, mortgage) |

| New credit inquiries | 10% | How often you apply for new credit |

Two factors — payment history and utilization — account for 65% of the score. That means most practical credit-building work comes down to two things: paying on time and keeping balances low.

Payment history is the single most important factor in your credit score. One missed payment reported to the bureaus — typically at 30 or more days past due — can drop a score of 700 or higher by 50–100 points. The damage is asymmetric: recovering what one missed payment removes takes months of consistent on-time payments. Setting up automatic minimum payments on every account eliminates this risk entirely, at no cost.

Accounts that contribute to payment history include credit cards, personal loans, car loans, mortgages, and lines of credit. Student loans also appear once you begin repayment.

Credit utilization is the percentage of your revolving credit limit you’re currently using — calculated both per card and across all cards combined. Keeping utilization below 30% is the general recommendation. Keeping it below 10% is better. Utilization above 60% causes significant damage even if every payment is made on time.

Utilization is measured when your lender reports to the bureau — typically your statement close date, not your payment due date. This means your score can show high utilization even if you pay the balance in full every month. Paying down your balance before the statement closes keeps your reported utilization low. For a full breakdown, read our guide on how credit card utilization affects your score.

Your credit history length is calculated using the age of your oldest account, your newest account, and the average age across all accounts. Closing your oldest credit card shortens your history and can reduce your score by 10–30 points — with the impact persisting for years. If a card has an annual fee you no longer want to pay, ask the issuer to downgrade it to a no-fee version. This preserves the account age without the ongoing cost.

Lenders like to see that you can manage both revolving credit (credit cards, lines of credit) and installment credit (car loans, mortgages, personal loans). The benefit is modest at 10%, and taking on debt solely to improve credit mix is not worthwhile. But if you’re considering a needed loan, knowing it also marginally helps your score removes one objection.

For Canadians who don’t yet qualify for a standard credit card, a Neo Secured Card is one of the most effective ways to begin building a credit mix from scratch. Our guide to prepaid vs secured credit cards in Canada explains exactly how secured cards work and how to use one effectively.

Every time you apply for credit, lenders perform a hard inquiry on your credit report. Each hard inquiry causes a small, temporary drop of roughly 5–10 points, and fades from your score after six months. The effect is minor — but multiple applications in a short period can signal financial stress to lenders.

One important protection: rate shopping for a mortgage or car loan is treated differently. Multiple inquiries for the same type of credit within a 14–45 day window are grouped as a single inquiry by both bureaus. You can — and should — shop multiple lenders for mortgage rates without worrying about your score.

How to Check Your Credit Score for Free

Checking your own credit score is always a soft inquiry — it has zero impact on your score, regardless of how often you check. There is no reason not to monitor it regularly.

Using Borrowell for Equifax and Credit Karma for TransUnion gives you visibility into both scores for free. This matters because different lenders pull from different bureaus — seeing both scores ensures no surprises when you apply for a mortgage or loan.

Your full credit report (not just the score number) is available free from both Equifax Canada and TransUnion Canada by mail. This is the document that contains your full account history, hard inquiries, and any collections or negative items. Reviewing it at least once a year to catch errors is worth the effort — inaccurate information on a credit report is more common than most Canadians assume.

What Appears on Your Credit Report

Your credit score is calculated using the data in your credit report. The report itself contains more detail than the score — and reviewing it is the only way to catch errors that may be dragging your score down.

Your credit report does not contain your income, employment history, assets, bank account balances, or investment holdings. Lenders gather that information separately as part of the application process.

How Long Negative Information Stays on Your Report

Negative items don’t stay on your credit report forever. Most fall off within 6–7 years — but the impact on your score fades well before they’re removed, as positive behaviour accumulates over time.

| Event | Typical Time on Report | Score Impact |

|---|---|---|

| Late payment (30+ days) | 6 years | Significant at first; fades with consistent on-time payments |

| Collection account | 6 years | Significant; reduced once paid or settled |

| Consumer proposal | 3 years from completion | Major initially; rebuilding possible within proposal period |

| Bankruptcy (first) | 6–7 years | Severe; scores can recover to 650+ within 2–3 years of discharge |

| Hard credit inquiry | 2–3 years | Minor (5–10 points); fades from scoring after 6 months |

Scores typically recover faster than most people expect, provided new credit habits are consistent. A discharged bankruptcy doesn’t preclude getting a mortgage — it extends the timeline. Many Canadians rebuild from a bankruptcy to a score above 650 within two to three years.

How Credit Scores Affect Real Financial Decisions

Credit scores aren’t just numbers. They translate directly into dollars — the interest you pay, the products you qualify for, and in some cases whether you can rent an apartment or land a job.

Mortgage Approval and Rates

Mortgage lenders place more weight on credit scores than almost any other factor. The Canadian market has three effective thresholds:

Qualifies for CMHC-insured mortgages (less than 20% down payment required). 600 is the hard minimum. Between 600–679, lenders apply stricter scrutiny to other factors including income stability and debt ratios. Rates will be higher than the best available.

Qualifies at most A-lenders (major banks and credit unions) at standard posted rates. The application will be approved for most products, but preferred pricing is not available at this range. Improving from 680 to 720 is one of the most financially impactful credit moves a Canadian can make before a mortgage application.

Access to the best available mortgage rates from A-lenders. On a $500,000 mortgage, a 60-point difference (660 vs 720) can translate to a rate gap of 0.25–0.50%, which compounds to $12,000–$25,000 in additional interest over a five-year term. That gap makes improving your score before applying for a mortgage one of the highest-return financial moves available.

Credit Card Eligibility

The best Canadian credit cards — premium cash back, travel rewards cards, and high-limit cards — require credit scores in the Good to Excellent range (generally 660+, with the most competitive cards requiring 720+). With a score below 620, options are typically limited to secured credit cards or prepaid products.

For families building credit: our Best Credit Cards in Canada guide covers which cards are accessible at each credit tier. If you’re rebuilding, the best no-fee credit cards are a practical entry point.

Loan Interest Rates

The rate difference by credit score is most visible on car loans and personal loans, where the gap between a strong and weak borrower is often 3–5 percentage points.

| Borrower A | Borrower B | |

|---|---|---|

| Credit score | 760 | 620 |

| Loan amount | $30,000 | $30,000 |

| Interest rate | 5.5% | 9.9% |

| Monthly payment (5 yr) | $574 | $638 |

| Total interest paid | $4,440 | $8,280 |

| Extra cost for weak credit | $3,840 on a single car loan | |

How to Improve Your Credit Score in Canada

The fastest improvements come from the two highest-weighted factors: payment history and utilization. Everything else is slower-moving. Prioritize in this order.

Set up automatic minimum payments on every account. One missed payment can drop a 700+ score by 50–100 points. Automatic payments cost nothing to set up and eliminate the most damaging single risk to your credit score.

Reducing utilization from 70% to below 30% can improve your score by 40–80 points within one to two statement cycles — faster than almost any other intervention. If you can’t pay the balance down, request a credit limit increase on an existing card. The same ratio improvement happens without requiring you to pay down debt.

Utilization is measured at statement close, not payment due date. Pay your balance down before the statement closes each month — even if you plan to pay the remainder on the due date. This keeps your reported utilization low even if you regularly carry a balance temporarily.

Closing your oldest credit card shortens your credit history and reduces your available credit limit, both of which can lower your score. If the card has no annual fee, keep it open and use it occasionally. If there’s a fee, ask the issuer to downgrade it to a no-fee version.

Each hard inquiry temporarily dips your score 5–10 points. Avoid applying for multiple new credit products within a few months of a major application like a mortgage. When shopping for mortgage or car loan rates, do it within a 14–45 day window so all inquiries count as one.

Errors on credit reports are more common than most Canadians realize — incorrect late payments, accounts you don’t recognize, or collections you’ve already paid. Disputing a legitimate error with Equifax or TransUnion is the fastest way to improve a score that has been dragged down by inaccurate data. Use Borrowell (Equifax) and Credit Karma (TransUnion) to monitor for changes.

For a full tactical playbook, read our dedicated guide: How to Improve Your Credit Score in Canada.

Building Credit From Scratch

If you’re new to Canada, have never had credit, or are rebuilding after a difficult financial period, the path is straightforward — it just takes 6–12 months to establish a usable score. Start with a secured credit card, use it for one or two small purchases per month, and pay the balance in full. Within six months you’ll typically have a score in the 600–650 range. A year of consistent use usually brings you into the 650–700 range.

Our guide to prepaid vs secured credit cards in Canada covers the best products for this purpose and exactly how to use them. If you’re ready to start, here’s the one we’d recommend:

The Neo Secured Card reports to both Equifax and TransUnion and earns cashback on purchases — making it one of the most effective ways to build credit from scratch while earning rewards on everyday spending. The $7.99/month fee is waived for Build members (free with $5,000+ held across any Neo account). Funds are held in trust at one or more CDIC member institutions.

Apply for the Neo Secured Card →Common Credit Score Myths

The Bottom Line

Your credit score is one of the most financially consequential numbers in your life — not because it’s hard to understand, but because most Canadians don’t optimize it until they’re already sitting across from a mortgage lender. The two factors that matter most are payment history (35%) and credit utilization (30%). Master those two and everything else follows.

If your score is below 680, the priority is clear: pay on time, pay down balances, and avoid new applications until you’ve applied for the mortgage or loan you need. If your score is above 720, the returns on further optimization are real but diminishing. Check both your Equifax and TransUnion scores for free through Borrowell and Credit Karma, review your full report once a year for errors, and let consistent habits do the work over time.

The national average is 680. The best mortgage rates start at 720. That 40-point gap is achievable for most Canadians within 6–12 months of focused effort.Frequently Asked Questions

A credit score of 660 or higher is generally considered good in Canada. Scores above 720 unlock the best rates across mortgages, car loans, and credit cards. The national average is approximately 680, which qualifies for most mainstream credit products at standard rates — but not the best available rates. For a full breakdown by score tier, read our guide on what is a good credit score in Canada.

The minimum score for a CMHC-insured mortgage (less than 20% down) is 600. For A-lender (major bank) approval, the effective floor is 680. For the best available mortgage rates, you generally need 720 or higher. Borrowers between 600 and 679 may qualify but will face stricter scrutiny on income, debt ratios, and other factors, and will typically pay higher rates.

It depends on which factor you’re improving. Paying down credit card utilization from 70% to below 30% can increase your score by 40–80 points within one to two statement cycles — often within 30–60 days. Payment history improvements are slower, building gradually over months of consistent on-time payments. Recovering from a missed payment or collection typically takes 6–12 months before the impact significantly fades.

No. Checking your own credit score is a soft inquiry and has no impact on your score whatsoever. Only hard inquiries — generated when a lender checks your credit after you apply for credit — affect your score, and those only by 5–10 points temporarily. You can monitor your score weekly through Borrowell (Equifax) or Credit Karma (TransUnion) without any risk to your score.

Both bureaus calculate scores on the same 300–900 scale and use the same five factors. They operate independently and collect data from different combinations of lenders, which is why your Equifax and TransUnion scores can differ by 20–50 points for the same person at the same time. Neither score is “correct” — lenders may pull from either bureau, so monitoring both is worth doing. Use Borrowell for your Equifax score and Credit Karma for your TransUnion score, both free.

No. Debit card transactions, chequing account balances, and savings account activity are not reported to credit bureaus and have no impact on your credit score. Only credit products — credit cards, loans, mortgages, and lines of credit — appear on your credit report. NSF (non-sufficient funds) fees and overdraft charges don’t affect your score either, unless the account goes to collections.

Yes, but it’s harder. Any credit product — a car loan, student loan in repayment, or line of credit — can establish a credit file. However, a credit card is the most accessible starting point for most Canadians because it has the lowest barriers to entry and allows you to build history on a monthly basis. If you don’t qualify for a standard card, a secured credit card works identically for credit-building purposes — it just requires a deposit upfront.

Submit a dispute directly to the bureau that has the error — Equifax Canada or TransUnion Canada — with documentation supporting your claim. Both bureaus are legally required to investigate disputes and respond within 30 days. Common errors worth disputing include incorrect late payments, accounts that aren’t yours (possible identity theft), and collections you’ve already paid that still show as unpaid. The Financial Consumer Agency of Canada provides guidance on the dispute process.

Most negative information stays on your report for six years from the date of the delinquency. Bankruptcies remain for six to seven years from the date of discharge. Hard credit inquiries stay for two to three years but stop affecting your score after six months. The score impact of negative items fades over time as positive behaviour accumulates — a late payment from four years ago carries far less weight than a recent one.

Now that you understand how credit scores work, put it into action. Read How to Improve Your Credit Score in Canada — a full tactical guide to moving your score up as fast as possible.