This article contains affiliate links. We may earn a commission if you open an account — at no cost to you. We only recommend products we’ve researched and trust.

Choosing the right travel credit card depends on spending level and travel frequency.

Most Canadians choose travel credit cards based on welcome bonuses. That’s the wrong metric. A flashy sign-up offer disappears after year one, but the fee, the everyday earn rate, and the redemption rules stay with you for as long as you carry the card.

Will this card outperform a strong 2% cashback setup for your household, year after year? That’s the only question that actually matters.

Before diving into travel cards specifically, see our complete guide to Best Credit Cards in Canada — it covers all card types so you can decide if travel is even the right category for you.

In our guide to the Best Cash Back Credit Cards in Canada, we evaluated realistic spending levels. We’ll use the same profiles here:

These spending assumptions align with broader patterns in Statistics Canada’s household expenditure data, which shows wide variation in discretionary and travel-related spending across income brackets.

In This Article

- Quick Picks: Best Travel Credit Cards (2026)

- Fixed-Value vs. Transferable Points

- Best for Moderate Spend Households (~$30K/Year)

- Not Ready for an Annual Fee? Start Here

- Best for Frequent Air Canada Flyers (~$60K/Year)

- Full Travel Credit Card Comparison Table

- Airline Loyalty Cards: What Changed With Aeroplan in 2026

- The Break-Even Math

- Using Travel Rewards Responsibly

- Where to Open

- Frequently Asked Questions

Quick Picks: Best Travel Credit Cards (2026)

| Category | Moderate Spend (~$30K) | High Spend (~$60K) |

|---|---|---|

| Fixed-Value Travel | Scotia Gold Amex | Scotia Gold (simple option) |

| Flexible, Low Fee | Amex Cobalt (if not ready for a bigger fee) | — |

| Airline Loyalty (mid-tier) | WestJet RBC (if loyal) | TD Aeroplan Visa Infinite |

| Flexible Transfer | RBC Avion (if optimizing) | Strong mid-tier transfer |

| Premium Airline Loyalty | Not recommended | Amex Aeroplan Reserve (frequent Air Canada flyers) |

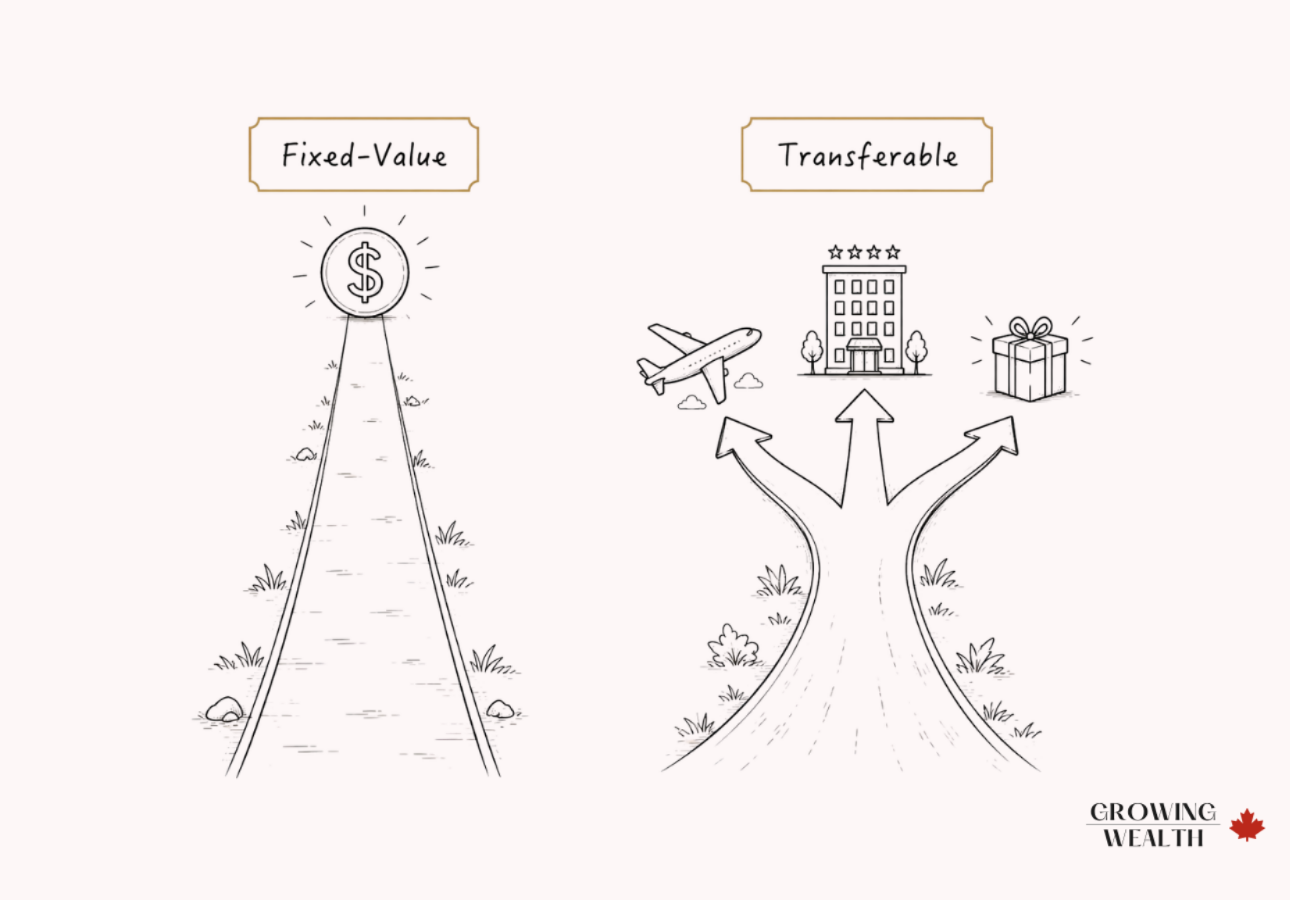

Fixed-Value vs. Transferable Points: What Actually Determines Value

This is the distinction most comparison sites skip, and it’s the one that actually determines whether a card is worth its fee.

- Examples: Scotia Gold Amex’s Scene+ points, WestJet dollars

- Worth a set amount — typically 1 cent per point, no matter how you redeem

- No strategy required, no waiting for a “good” redemption

- No risk of a program devaluation cutting your points’ value overnight

- Trade-off: a ceiling — never outsized value the way transferable points can offer

- Examples: Aeroplan, RBC Avion, Amex Membership Rewards

- Value fluctuates depending on how you redeem — a point can be worth 3-4 cents at a sweet-spot award

- Lazy redemptions (cash-equivalent credits) often land closer to 1 cent per point

- Upside is real, but requires learning redemption charts and tracking seat availability

- Occasionally means waiting months for the right award to open up

Fixed-value points are predictable. Transferable points have a higher ceiling but require more effort to optimize.

If you don’t have the time or interest to optimize redemptions, a fixed-value card at a lower fee will out-earn a transferable-points card for you in practice, even if the transferable program has a higher theoretical ceiling. Match the card to your actual behaviour, not your aspirational one.

Best for Moderate Spend Households (~$30K/Year)

Scotiabank Gold American Express

For moderate spenders, this card delivers:

Up to 5-6x Scene+ points in bonus categories

No transfer charts to learn

Including trip cancellation coverage

A genuine rarity among Canadian cards

- No foreign transaction fee saves roughly 2.5% on every purchase made abroad or in foreign currency online

- Points never expire and can be redeemed toward almost any travel expense, not just flights booked through a specific portal

- Not accepted everywhere in Canada — notably not at Costco or many Loblaws-owned grocery banners

- Accelerated earn rates cap at $50,000 in annual spending, after which the rate drops to 1 point per dollar

| Metric | Amount |

|---|---|

| $30,000 × ~2.2% effective earn | ~$660 |

| Annual fee | ~$120 |

| Net value | ~$540 |

For households in this spending range, this card consistently clears a 2% cashback baseline without requiring complex point transfers.

Simple, fixed-value travel redemption with no foreign transaction fee — the easiest travel card to justify at this spend level.

Learn more about the Scotia Gold Amex →Not Ready for an Annual Fee? Start Here

If you’re not confident you’ll spend $25,000+ a year or you travel infrequently, jumping straight to a $120+ annual fee card is premature. The American Express Cobalt Card is a reasonable middle ground: a $15.99/month fee (about $192/year) that earns 5x Membership Rewards points on groceries, dining, and food delivery, with full access to Amex’s transfer partner network if you later want to explore the transferable-points side of the equation.

It won’t outperform a dedicated travel card for a household that travels often and spends deliberately in travel categories, but it’s a lower-commitment way to start earning flexible points before deciding whether a bigger annual fee is worth it. For a full breakdown of when an annual fee actually pays for itself, see our guide on whether annual fee credit cards are worth it in Canada. If you’d rather skip annual fees altogether while you build spending habits, our Best No-Fee Credit Cards in Canada guide covers stronger $0-fee options.

Best for Frequent Air Canada Flyers (~$60K/Year)

American Express Aeroplan Reserve Card

At $60,000 in annual spending and frequent Air Canada travel, this is the card that separates itself from the mid-tier Aeroplan option.

Beyond the earn rate, the card includes:

2 points per dollar, plus 1.25 points per dollar on everything else

Plus priority check-in, boarding, and baggage handling

At $25,000 net purchases — a companion flies Air Canada economy for a fixed $99-$599 fare

Up to $100 toward application or renewal every four years

- For a household that already flies Air Canada regularly, the combination of lounge access, free checked bags for up to eight companions, and the companion pass can comfortably exceed the fee

- Points never expire as long as you hold the card

- The $599 annual fee only makes sense for genuinely frequent Air Canada flyers — occasional travellers will get more value from the TD Aeroplan Visa Infinite at a fraction of the cost

- Carries a 2.5% foreign transaction fee, unlike the Scotia Gold Amex’s no-FX-fee benefit — not the right pick for someone who shops or travels heavily outside Canada

Note this is a different tier from the TD Aeroplan Visa Infinite covered below — both earn Aeroplan points, but this one is built for households who will actually use premium airport perks, not just accumulate points.

| Metric | Amount |

|---|---|

| $60,000 spend at blended tiered earn rate | ~100,000 Aeroplan points |

| Estimated point value (~1.8 cents/point average) | ~$1,800 |

| Annual fee | ~$599 |

| Net rewards | ~$1,201 |

| Companion pass + lounge access + credits (if fully used) | $700-$1,000+ |

| Total potential value | $1,600-$2,200+ |

When Air Canada spend, the companion pass, and lounge access are all genuinely used, this comfortably surpasses mid-tier cards. If those benefits go unused, most of that value evaporates and a lower-fee card is the better fit.

The highest Air Canada earn rate on the market, plus lounge access and an annual companion pass — built for households who will genuinely use the perks.

Learn more about the Aeroplan Reserve Card →Full Travel Credit Card Comparison Table (2026)

| Card | Annual Fee | Best For | Key Strength |

|---|---|---|---|

| Scotia Gold Amex | $120 | Moderate spend households | Grocery earn + simple redemption |

| Amex Cobalt | ~$192/yr | Entry-level flexible points | Low commitment, transfer partner access |

| Amex Aeroplan Reserve | $599 | Frequent Air Canada flyers | 3x Air Canada earn + lounge access + companion pass |

| WestJet RBC World Elite | $139 | WestJet loyal flyers | Companion voucher + free bags |

| TD Aeroplan Visa Infinite | $139 | Occasional Air Canada flyers | Aeroplan earning at a lower fee |

| RBC Avion Visa Infinite | $120 | Transfer strategy users | Airline partner transfers |

Airline Loyalty Cards: What Changed With Aeroplan in 2026

If you’re considering an airline-specific card, the mechanics changed meaningfully at the start of this year. As of January 1, 2026, Aeroplan members earn points on eligible Air Canada flights based on dollars spent rather than distance flown — and Elite Status now runs on Status Qualifying Credits (SQC) instead of the old mileage-based system.

- Points earned based on distance flown

- Elite Status built on Status Qualifying Miles + Status Qualifying Segments

- Points earned based on dollars spent on Air Canada flights

- Elite Status built entirely on Status Qualifying Credits (SQC)

For a cardholder, the practical effect is that Aeroplan co-branded cards now contribute more predictably toward Elite Status progress, based on spend rather than distance flown. This favours households who spend heavily on the card but don’t necessarily fly long-haul routes.

Suits someone who flies Air Canada a few times a year and wants Aeroplan earning without a steep fee.

Built for genuinely frequent flyers who will use Maple Leaf Lounge access, the companion pass, and the higher 3x Air Canada earn rate — occasional flyers won’t recoup this fee.

WestJet’s companion voucher program works differently and wasn’t affected by the Aeroplan changes. Review WestJet’s official page on how the annual companion voucher works, including route restrictions and fare rules, before assuming the value applies to your typical trip. These details matter when calculating real value, since a headline “up to $500 in value” companion voucher can be worth far less once route and fare restrictions are factored in.

The Break-Even Math: How to Know If a Travel Card Is Worth It

The formula is simple:

(Annual Spend × Effective Reward Rate) − Annual Fee > Cashback Alternative

If your travel card cannot outperform a strong 2% cashback baseline, reconsider it. Here’s how that plays out at each spend level:

A $120-fee travel card would need to earn better than 2.8% just to match that baseline once the fee is subtracted — a bar most travel cards don’t clear at this spend level.

The Scotia Gold Amex’s ~$660 in rewards minus its $120 fee nets ~$540 — this is where cashback starts to lose its edge, but only marginally.

The Amex Aeroplan Reserve’s total potential value of $1,600-$2,200+ (with the companion pass and lounge access fully used) clearly outperforms cashback, but that outcome depends entirely on actually flying Air Canada often enough to use the perks — not just holding the card.

Always compare rewards earned against annual fees before choosing a travel card.

For the detailed comparison of when travel rewards actually beat cashback, see our guide to Cash Back vs Travel Rewards in Canada.

Using Travel Rewards Responsibly

Rewards only create value when balances are managed properly. The Financial Consumer Agency of Canada’s guidance on using credit cards responsibly emphasizes paying your balance in full, understanding interest charges, and reviewing your card’s terms carefully.

Never let a balance carry over just to keep earning points.

Interest rates on these cards typically run 20.99% or higher, which erases months of earned rewards almost instantly.

Annual fees, foreign transaction fees, and penalty rates all affect whether a card is actually worth it.

Travel rewards never compensate for high-interest debt. For a practical guide to maximizing rewards without overspending, see How to Use Credit Cards for Rewards.

Where to Open

Best starting point for moderate-spend households who want simple, fixed-value redemption without a transfer-chart learning curve.

Learn more about the Scotia Gold Amex →Best for households already spending $60K+ a year who fly Air Canada often enough to genuinely use the lounge access and companion pass, not just hold the card for status.

Learn more about the Aeroplan Reserve Card →Best for households loyal to Air Canada who want their spending to count toward Elite Status under the new SQC system, without the $599 fee.

Learn more about the TD Aeroplan Visa Infinite →The Bottom Line

Choose based on the math, not the welcome bonus:

- ~$30K spend, want simplicity: Scotia Gold Amex

- ~$30K spend, not ready for a fee yet: Amex Cobalt, or a no-fee card while you build spending habits

- ~$60K spend, frequent Air Canada travel, will use the perks: Amex Aeroplan Reserve

- Loyal to one airline and fly it regularly: the matching co-branded card, but check whether you’ll actually use the companion voucher or checked-bag benefit every year

- Infrequent traveller: cashback usually wins — revisit our Best Cash Back Credit Cards in Canada guide instead

Frequently Asked Questions

For most households spending around $30,000 annually, the Scotiabank Gold American Express offers the best balance of rewards and annual fee. For higher-spend, frequent Air Canada flyers who will use the perks, premium cards like the American Express Aeroplan Reserve Card typically deliver the highest total value.

Travel credit cards are better only if their net rewards exceed a strong 2% cashback alternative after annual fees. Frequent travellers who use perks consistently may benefit more from travel rewards, while occasional travellers often receive more reliable value from cashback.

To justify a premium card with a high annual fee, most households need at least $25,000-$30,000 in annual spending and regular travel. Without frequent use of benefits, premium cards rarely outperform mid-tier options.

Most Canadian credit cards, including many travel cards, charge a 2.5% foreign transaction fee on purchases made in a foreign currency, whether online or while travelling abroad. A handful of premium travel cards waive this fee entirely — the Scotiabank Gold American Express is one of the few in this guide with no foreign transaction fee. Others, including the American Express Aeroplan Reserve Card, still charge the standard 2.5%. If you travel internationally often or shop online in US dollars regularly, prioritize a no-FX-fee card over a higher points-earning card with the fee, since the savings usually outweigh the difference in rewards.

Most premium travel credit cards include some level of travel insurance, typically covering emergency medical, trip cancellation and interruption, flight delay, and lost or delayed baggage. Coverage details vary significantly by card and often come with conditions: many require a set percentage of the trip cost be charged to the card, and several policies reduce or exclude coverage for cardholders over 65. Always read the certificate of insurance for your specific card rather than assuming coverage matches what’s advertised.

No. American Express acceptance in Canada has expanded significantly in recent years, but it’s still not universal. Costco does not accept American Express in-store or online, and stores under the Loblaws banner (including Loblaws, Real Canadian Superstore, and No Frills) don’t accept it either. If your travel card is an Amex, it’s worth carrying a Visa or Mastercard as backup for those specific retailers.

Most premium travel credit cards require a good to excellent credit score, typically 700 or higher, along with meeting income requirements. See What is a Good Credit Score in Canada? to understand where you stand.

As of January 1, 2026, Aeroplan switched from a distance-based earning system to a dollars-spent system for points earned on Air Canada flights, and Elite Status now runs on Status Qualifying Credits instead of the old mileage-based system. For cardholders, this makes card spending count more predictably toward status, which slightly favours Aeroplan co-branded cards for households who put heavy everyday spending on the card, regardless of how far they actually fly.

Want to see how travel cards stack up against every other card type? Read Best Credit Cards in Canada — our full guide comparing cash back, travel, and no-fee cards side by side so you can confirm travel is the right category before you apply.