Choosing between Wealthsimple and Questrade isn’t as straightforward as it used to be.

Both platforms now offer self-directed investing, managed portfolios, and access to TFSAs, RRSPs, and FHSAs. On the surface, they look very similar.

But once you start using them, the differences become clear.

Most investors don’t struggle because they picked the wrong platform. They struggle because they don’t stay consistent—missing contributions, hesitating during downturns, or overthinking decisions early.

If you’re not fully clear on how investing works yet, start with this step-by-step guide to investing in Canada (coming soon). It will make the rest of this comparison much easier to understand.

Quick Answer: Wealthsimple or Questrade?

If you want a direct answer:

Wealthsimple is the better choice if your priority is simplicity and consistency. It removes friction and makes it easy to stay invested.

Questrade is the better choice if your priority is long-term efficiency. It gives you more control and helps reduce costs—but requires discipline.

For most Canadians, the best path isn’t choosing one forever.

👉 Open a Wealthsimple account and start investing

Start simple. Then optimize later.

Many readers ask: is Wealthsimple better than Questrade?

The real answer is that it depends less on the platform—and more on how you invest.

Most people delay investing because they overthink this decision. Choosing a simple platform and starting now is almost always better than waiting to optimize.

Wealthsimple vs Questrade: Side-by-Side Comparison

| Feature | Wealthsimple | Questrade |

|---|---|---|

| Core strength | Simplicity & UX | Flexibility & control |

| Self-directed investing | Yes (commission-free) | Yes |

| Managed portfolios | Yes | Yes |

| Managed fees | ~0.4–0.5% | ~0.25% |

| Trading fees | $0 | ETFs free; stocks ~$5–$10 |

| Ease of use | Very high | Moderate |

| Automation | Strong | Limited |

This gives you a quick snapshot. But the real decision comes down to how each platform influences your behaviour.

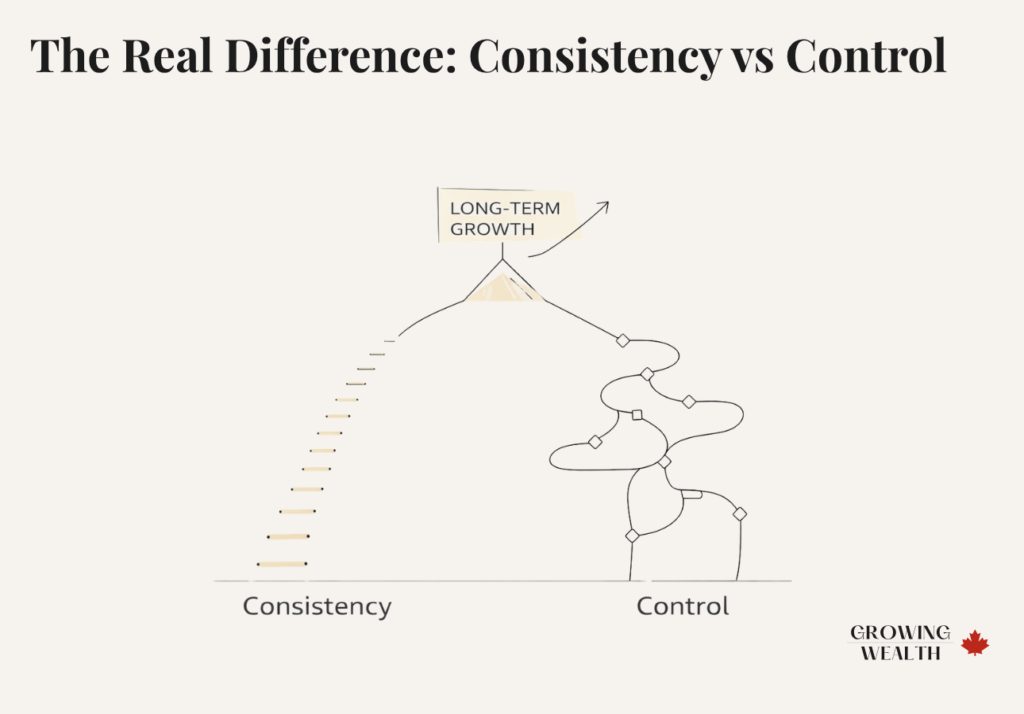

The Real Difference: Consistency vs Control

Both platforms can do the same things. You can buy ETFs, open registered accounts, and build a long-term portfolio on either one.

What separates them is how they guide your decisions.

Wealthsimple is designed to reduce friction. It makes it easy to start investing and even easier to continue. You don’t need to make many decisions, which lowers the chances of getting stuck.

Questrade gives you more control. You choose what to buy, how to allocate your portfolio, and when to invest. That flexibility is valuable—but only if you use it properly.

In simple terms, Wealthsimple helps you stay consistent, while Questrade helps you become more efficient.

Wealthsimple vs Questrade Fees: What You Actually Pay

At first glance, both platforms look inexpensive. The difference shows up over time.

Wealthsimple charges a management fee for its managed portfolios, usually around 0.4–0.5%. That fee applies every year and gradually reduces your long-term returns.

Questrade doesn’t charge a management fee for self-directed investing. If you’re buying ETFs, that creates a meaningful cost advantage over decades.

If you’re still deciding how to build your portfolio, it’s worth reviewing what you should actually invest in.

The structure of your investments has a bigger impact than small fee differences early on.

Foreign Exchange Fees: The Overlooked Cost

This is where the comparison becomes more nuanced.

Wealthsimple applies a foreign exchange spread of roughly 1.5% when converting Canadian dollars to U.S. dollars. This affects any investor buying U.S.-listed ETFs or stocks.

Questrade offers lower FX costs and gives investors ways to reduce them further.

For example, converting $10,000 CAD might cost around $150 on Wealthsimple, while Questrade can reduce that cost significantly depending on the method used.

That difference compounds over time—especially if you invest regularly in U.S. assets.

Example: $500 per Month Over 25 Years

To make this tangible, imagine investing $500 per month for 25 years at a 6% return.

Using a managed approach with Wealthsimple, you might end up around $290,000.

Using a low-cost ETF strategy through Questrade, that number could be closer to $315,000.

That’s roughly a $25,000 difference, driven primarily by fees.

The biggest risk isn’t choosing the wrong platform—it’s not investing at all.

A cheaper platform only wins if you actually use it.

If you’re also deciding how to invest over time, this breakdown of lump sum vs dollar-cost averaging will help you understand how timing affects your results.

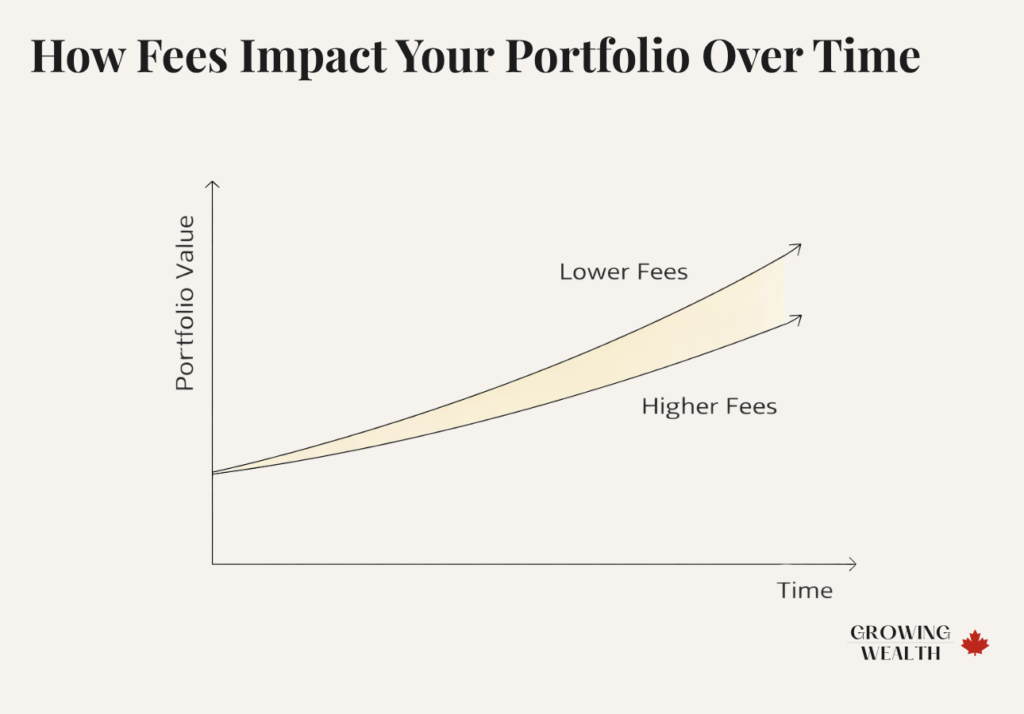

How Fees Impact Your Portfolio Over Time

Even small differences in fees compound over time.

A 0.3–0.5% annual difference may not seem significant, but over decades, it can translate into tens of thousands of dollars in lost returns.

This is why experienced investors eventually move toward lower-cost structures—but only after they’ve built consistent investing habits.

Wealthsimple: What People Misunderstand

Wealthsimple is often described as “too simple.”

That’s exactly the point.

Its biggest advantage is that it removes barriers. You can set up automatic contributions, avoid overthinking, and stay invested without constant decision-making.

Its drawback is cost efficiency. Between management fees and FX costs, it isn’t the most optimized platform for long-term investors who want full control.

Questrade: What People Misunderstand

Questrade is often framed as the better option because it’s cheaper.

That only holds if the investor behaves correctly.

More control sounds appealing, but it also increases the likelihood of mistakes—delaying contributions, changing strategies, or reacting emotionally.

👉 Open a Questrade account for self-directed investing

For disciplined investors, Questrade is more efficient. For everyone else, it can quietly lead to worse outcomes.

Wealthsimple vs Questrade TFSA: Which Is Better?

For most Canadians, the TFSA is the first place they invest.

Wealthsimple is typically the better starting point. It makes it easy to contribute regularly and removes unnecessary complexity.

Questrade becomes more useful as your strategy evolves—especially if you want to minimize costs and invest in U.S. ETFs.

A practical way to think about it:

Start with Wealthsimple. Optimize with Questrade later.

The Biggest Mistake Canadians Make

Most people focus on fees before they’ve built consistency.

They compare platforms, analyze costs, and try to optimize everything from the start. That usually leads to hesitation—and hesitation leads to inaction.

A platform that is slightly more expensive but easy to use will outperform a cheaper one that you don’t use consistently.

The order matters:

- Start investing.

- Stay consistent.

- Optimize later.

Can You Switch Between Platforms?

Yes—and many investors do.

Accounts like TFSAs and RRSPs can be transferred between platforms. The process takes time, but it’s straightforward.

It’s common to start simple, then transition once you’re more comfortable managing your investments.

Regulation and Protection

Both platforms are regulated by the Canadian Investment Regulatory Organization.

They are also members of the Canadian Investor Protection Fund (CIPF), which protects client assets if a firm becomes insolvent.

Where This Fits in Your Investing Plan

Before choosing a platform, you need a system.

That includes deciding how much you’ll invest and staying consistent over time. If you haven’t done that yet, define how much you should invest each month based on your income and goals.

Once that’s clear, the platform decision becomes much easier.

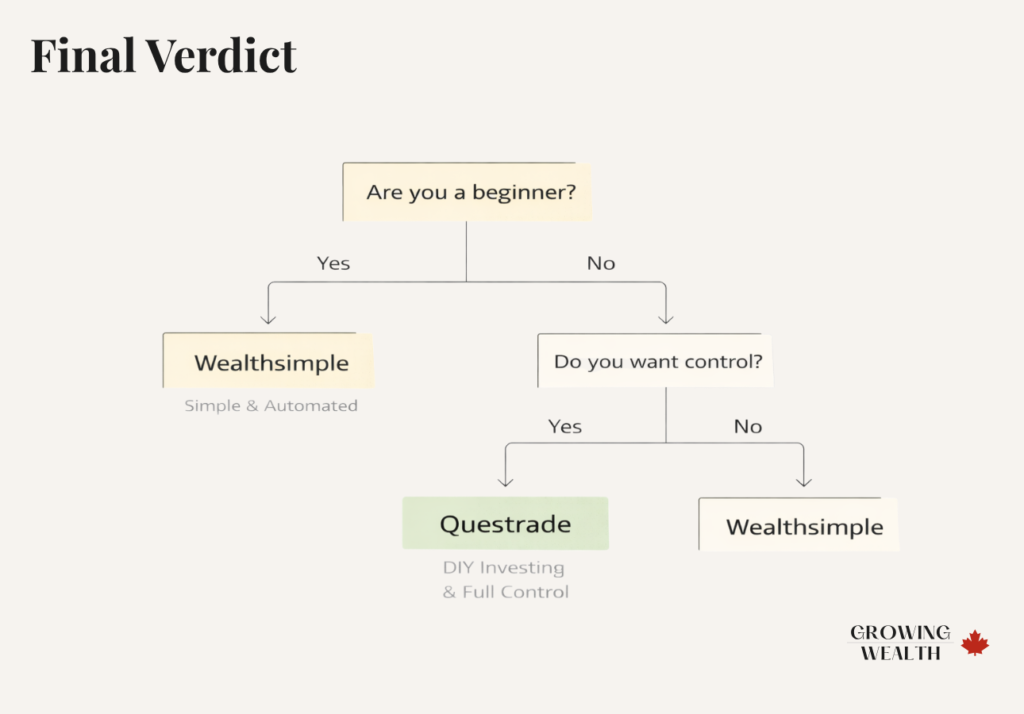

Final Verdict

Wealthsimple is the better choice for most Canadians starting out. It removes friction and makes it far more likely that you’ll actually invest consistently.

Questrade is the better choice once you understand ETFs and want to reduce costs. It gives you more control—but only pays off if you use it properly.

Clear answer:

Start with Wealthsimple. Move to Questrade once you’re confident managing your own portfolio.

Waiting to optimize too early usually leads to worse outcomes.

Frequently Asked Questions

Is Wealthsimple better than Questrade?

For beginners, yes. For long-term cost efficiency, Questrade is typically better.

Is Questrade cheaper?

Yes, especially for DIY ETF investing and U.S. assets.

Which is better for a TFSA?

Wealthsimple for simplicity. Questrade for efficiency.

Can I switch later?

Yes. Many investors transition over time.

Should I use both?

Yes. It’s a practical way to balance ease and optimization.

Affiliate Disclosure

💡 GrowingWealth.ca is supported by readers. Some of the links in this article are affiliate links, which means we may earn a small commission if you open an account or make a purchase — at no extra cost to you. We only recommend products and services we personally use, trust, or believe provide genuine value to Canadians. Our reviews and comparisons are always independent and objective.