Most Canadian Families Overpay Taxes Every Year

Most Canadian families overpay thousands in taxes every year—not because they earn too much, but because they miss key opportunities.

Canada’s tax system isn’t just about collecting tax. It’s designed to encourage certain behaviours—saving, investing, raising children, and planning for the future. If you’re not actively using those incentives, you’re likely paying more than necessary.

Reducing your tax bill isn’t about loopholes or aggressive tactics. It’s about understanding how the system works and making better decisions throughout the year—not just at tax time.

Who This Guide Is For

This guide is written for Canadian families who want practical, real-world tax strategies—especially households earning between $60,000 and $200,000+, where tax planning starts to have meaningful impact.

How Taxes Work in Canada (Quick Context)

Canada uses a progressive tax system, meaning higher portions of your income are taxed at higher rates. But not all income is treated the same—and that’s where planning matters.

The goal isn’t simply to “pay less tax.” It’s to:

- Reduce taxable income where appropriate

- Use credits and deductions effectively

- Structure income in a more tax-efficient way

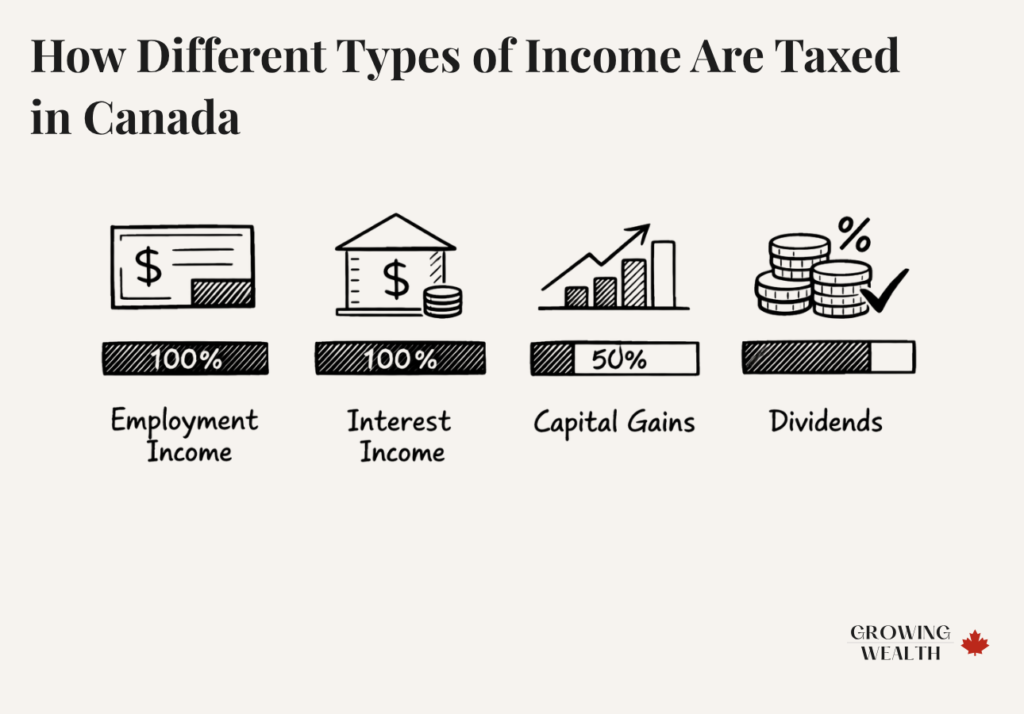

How Different Types of Income Are Taxed in Canada

One of the most overlooked parts of tax planning is understanding that not all income is taxed equally.

| Income Type | Tax Treatment | Efficiency |

|---|---|---|

| Employment income | 100% taxable | Lowest |

| Interest income | 100% taxable | Lowest |

| Capital gains | 50% taxable | High |

| Dividends | Tax credit applied | High |

Employment and interest income are taxed fully at your marginal rate, making them the least efficient forms of income.

Capital gains are significantly more favourable—only half of the gain is taxable. Dividends, particularly from Canadian companies, benefit from dividend tax credits, which reduce the effective tax rate.

This is why two families earning the same amount can pay very different taxes depending on how their income is structured.

Where to Start (Simple Tax Strategy Order)

If you’re unsure where to begin, focus on the fundamentals in this order:

- Use RRSP contributions if you’re in a higher tax bracket

- Maximize tax-free growth through your TFSA

- Ensure all credits and deductions are being claimed

- Look at opportunities to optimize across spouses

- Only then consider more advanced strategies

Tax Strategies by Income Level in Canada

Tax planning isn’t one-size-fits-all. What works at $50,000 income is very different from what works at $150,000.

Under $60,000

At lower income levels, flexibility matters more than deductions. TFSAs are typically more valuable than RRSPs because withdrawals remain tax-free and don’t impact benefits.

Government benefits like the Canada Child Benefit and GST/HST credits also play a larger role, so keeping taxable income lower can actually increase overall cash flow.

$60,000–$120,000

This is where planning starts to matter more.

A balanced approach often works best:

- Use RRSP contributions strategically

- Continue building TFSA investments

- Take advantage of deductions like child care expenses

At this level, even modest planning decisions can result in meaningful tax savings.

$120,000+

At higher income levels, tax strategy becomes critical.

RRSP contributions become significantly more valuable due to higher marginal tax rates. Income splitting, investment structure, and advanced strategies like donating investments can all have a meaningful impact.

The Most Effective Ways to Reduce Your Tax Bill

RRSP Contributions

RRSPs remain one of the most powerful tools available because they directly reduce taxable income.

For example, a $10,000 contribution at a higher marginal rate can result in several thousand dollars in tax savings. The higher your income, the more impactful this becomes.

For a deeper breakdown of when each account makes sense, see our guide on RRSP vs TFSA in Canada.

Using Your TFSA Properly

A TFSA doesn’t reduce taxes today, but it eliminates taxes on growth entirely. That includes capital gains, dividends, and interest.

The mistake most people make is treating their TFSA as a savings account instead of an investment vehicle.

If you’re not fully using your TFSA yet, this complete TFSA guide for Canadians walks through how to use it effectively.

Income Splitting

Because Canada taxes individuals—not households—shifting income between spouses can reduce total tax paid.

This is commonly done through:

- Spousal RRSPs

- Pension income splitting

- Business income planning (where applicable)

Tax Credits and Deductions

Credits reduce your tax bill directly, while deductions reduce your taxable income.

Some of the most commonly missed opportunities include:

- Child care expenses

- Medical expenses

- Tuition credits

- Professional dues

For full details on available credits and deductions, refer to Canada Revenue Agency.

Capital Gains and Investment Strategy

If you invest in taxable accounts, managing capital gains becomes important.

Losses can be used to offset gains, reducing your tax liability. These losses can also be carried back or forward, which gives flexibility across tax years.

RESPs for Long-Term Planning

If you invest in taxable accounts, managing capital gains becomes important.

Losses can be used to offset gains, reducing your tax liability. These losses can also be carried back or forward, which gives flexibility across tax years.

For a full breakdown of how RESPs work and when to use them, see our RESP guide for Canadian families.

Charitable Donations (A Highly Effective Tax Credit)

Charitable donations provide a direct reduction in taxes through non-refundable tax credits.

Smaller donations receive a lower credit rate, while amounts above $200 receive a higher rate. This means larger or combined donations are generally more effective.

Donating Stocks Instead of Cash

For investors, donating appreciated investments can be significantly more tax-efficient than donating cash.

When you donate publicly traded securities:

- You avoid paying capital gains tax

- You receive a tax receipt for the full market value

For example, if an investment grew from $5,000 to $10,000, donating it directly avoids tax on the $5,000 gain while still providing a $10,000 donation credit.

This strategy is particularly effective for higher-income families.

You can verify eligible charities through Canada Revenue Agency.

Complete List of Common Tax Deductions in Canada

- RRSP contributions

- Child care expenses

- Moving expenses (if eligible)

- Union and professional dues

- Investment carrying charges

- Home office expenses

Each of these reduces your taxable income, which can lower your overall tax bill.

Tax Credits Every Canadian Family Should Know

- Basic personal amount

- Spousal amount

- Tuition tax credits

- Medical expense credits

- Disability tax credit

- Charitable donation credits

Understanding the difference between credits and deductions—and using both effectively—is key to reducing taxes.

Real Examples: How Much You Can Save

Scenario 1: Middle-Income Family

A household earning $70,000 that contributes to an RRSP and claims child care expenses can reduce their tax bill by several thousand dollars, often in the range of $2,000–$3,000 depending on the province.

Scenario 2: Higher-Income Family

A household earning $150,000 that maximizes RRSP contributions and uses charitable donation strategies can reduce taxes by $8,000 or more.

Real Examples: How Much You Can Save

| Strategy | Reduces Tax Today | Reduces Tax Later | Best For |

|---|---|---|---|

| RRSP | Yes | No | Higher income |

| TFSA | No | Yes | Long-term growth |

| RESP | No | Yes | Families with children |

| Donations | Yes | No | Higher income |

| Credits/Deductions | Yes | No | All households |

Common Tax Mistakes Canadians Make

Many families don’t overpay taxes because of complexity—they overpay because of missed basics.

Some of the most common mistakes include:

- Using a TFSA only for cash instead of investing

- Not contributing to an RRSP in high-income years

- Holding investments in taxable accounts unnecessarily

- Missing eligible credits like child care or medical expenses

- Failing to coordinate tax strategy between spouses

These are simple issues—but they often result in thousands of dollars lost each year.

How This Fits Into Your Financial System

Tax savings should not be treated as a one-time benefit. They should feed into a broader financial system.

This approach works best when it’s part of a broader system. Here’s how it fits into a simple family finance system for Canadians.

A simple flow looks like:

- Tax savings → build emergency fund → invest through TFSA → long-term growth

Tax Reduction Is About Year-Round Decisions

Reducing your tax bill isn’t about filing differently—it’s about planning differently.

The families who consistently pay less tax are the ones who:

- Think ahead

- Use the right accounts

- Structure income intentionally

Even a few adjustments can result in meaningful, ongoing savings.

Frequently Asked Questions

What is the most effective way to reduce taxes in Canada?

For most higher-income families, RRSP contributions provide the largest immediate impact.

Is TFSA or RRSP better?

It depends on your income level—higher incomes benefit more from RRSPs, while lower incomes often benefit more from TFSAs.

Are dividends more tax-efficient than interest income?

Yes, due to dividend tax credits, dividends are generally taxed more favourably.

Can donating stocks reduce taxes more than cash?

A high-interest savings account.

Yes. Donating investments avoids capital gains tax while still providing a full tax credit.

Do tax refunds mean I overpaid?

In most cases, yes. A refund typically means too much tax was withheld during the year.

Affiliate Disclosure

💡 GrowingWealth.ca is supported by readers. Some of the links in this article are affiliate links, which means we may earn a small commission if you open an account or make a purchase — at no extra cost to you. We only recommend products and services we personally use, trust, or believe provide genuine value to Canadians. Our reviews and comparisons are always independent and objective.