Credit cards with annual fees promise higher rewards, travel perks, insurance coverage, and premium benefits. But those benefits only make sense if the extra value exceeds both the annual fee and what you could earn with a strong no-fee credit card.

Many Canadians assume premium cards automatically deliver better rewards. In reality, the difference depends on how much you spend and where you spend it.

In this guide we’ll break down:

- when annual fee credit cards are worth it

- when no-fee cards are the better option

- how to calculate the break-even point

- real examples based on Canadian household spending

If you’re comparing options broadly, start with our guide to Best Credit Cards in Canada.

Quick Picks: Best Annual Fee Credit Cards in Canada

| Card | Annual Fee | Best For | Apply |

|---|---|---|---|

| Neo World Elite Mastercard | $125 | High grocery and retail rewards | Apply Here |

| American Express Cobalt Card | $155.88 | Excellent food and travel rewards | Apply Here |

| TD Aeroplan Visa Infinite | $139 | Travel rewards and strong insurance | Apply Here |

You can compare these cards with others in Best Credit Cards in Canada.

Which Annual Fee Credit Card Is Right for You?

Different annual fee credit cards perform best depending on your spending habits.

| If you spend most on | Best Card | Why |

|---|---|---|

| Groceries and everyday shopping | Neo World Elite Mastercard | High grocery and retail rewards |

| Restaurants and dining | American Express Cobalt Card | Strong rewards on food spending |

| Flights and travel | TD Aeroplan Visa Infinite | Excellent travel rewards and insurance |

When Is an Annual Fee Credit Card Worth It?

An annual fee credit card is worth it when the extra rewards, benefits, and perks earned from the card exceed both the annual fee and the rewards available from a strong no-fee credit card. This typically happens when cardholders spend heavily in high-reward categories such as groceries, dining, or travel.

Annual Fee vs No-Fee Credit Cards at a Glance

| Feature | Annual Fee Card | No-Fee Card |

|---|---|---|

| Annual cost | $99–$799 | $0 |

| Rewards rates | Higher | Moderate |

| Travel perks | Often included | Rare |

| Insurance coverage | Strong | Limited |

| Best for | High spenders & travellers | Lower-spend households |

Best No-Fee Credit Cards in Canada

Before paying an annual fee, it’s important to understand what strong no-fee cards already offer.

| Card | Annual Fee | Best Feature | Apply |

|---|---|---|---|

| Tangerine Money-Back Credit Card | $0 | Customizable 2% categories | Apply Here |

| Simplii Cash Back Visa | $0 | High restaurant rewards | Apply Here |

| PC Financial World Elite Mastercard | $0 | Strong grocery rewards | Apply Here |

See the full list here: Best No-Fee Credit Cards in Canada

For comparison examples in this article, we assume an average 1.5% reward rate from a strong no-fee card.

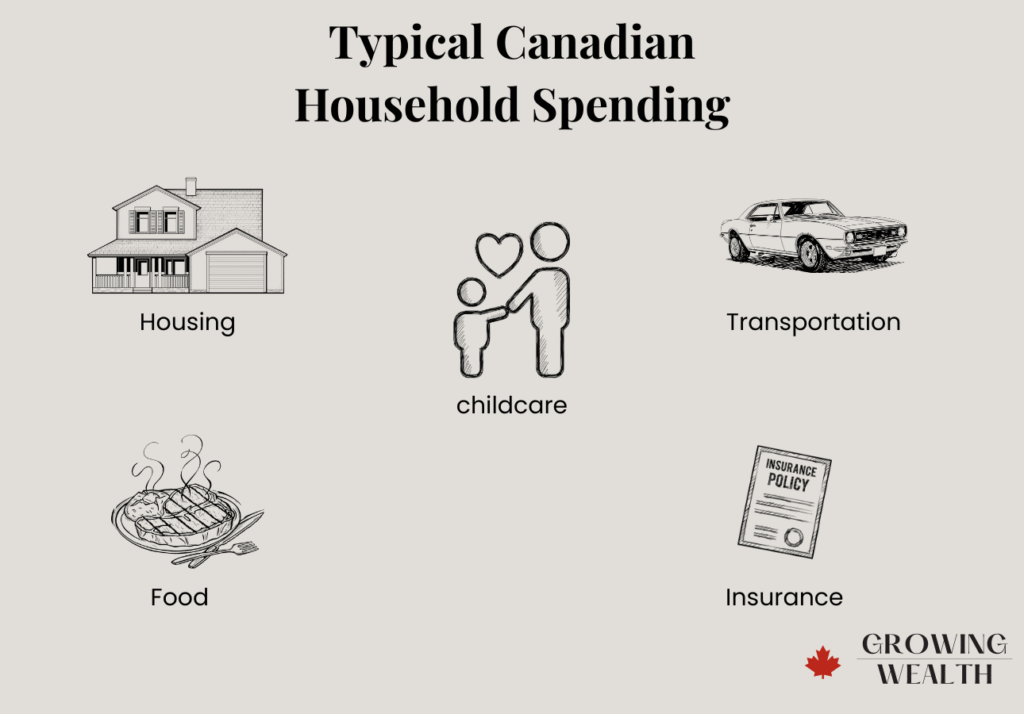

Typical Canadian Household Spending

To evaluate credit cards realistically, it helps to understand how Canadians actually spend money.

According to Statistics Canada, the largest household spending categories include:

- housing

- transportation

- food

- insurance

- childcare

Food spending alone often exceeds $8,000–$10,000 per year, which is why grocery reward categories are especially important when comparing credit cards.

How Much Do You Need to Spend for an Annual Fee Card to Be Worth It?

Use this simple formula.

Break-even spending = Annual fee ÷ extra reward rate

Example:

Annual fee: $150

Premium card reward rate: 2.5%

No-fee card reward rate: 1.5%

Extra reward rate = 1%

Break-even spending:

$150 ÷ 0.01 = $15,000 per year

If you spend more than this amount annually, the premium card may provide more value than a no-fee alternative.

Are Annual Fee Credit Cards Worth It? Real Spending Examples

Assumptions used:

No-fee card rewards: 1.5%

Premium card rewards: 2.5%

Annual fee: $150

| Household Type | Annual Spending | No-Fee Rewards | Premium Rewards | Extra Rewards | Annual Fee | Net Result | Winner |

|---|---|---|---|---|---|---|---|

| Low spend household | $12,000 | $180 | $300 | $120 | $150 | -$30 | No-fee card |

| Moderate spend household | $30,000 | $450 | $750 | $300 | $150 | +$150 | Annual fee card |

| High spend household | $54,000 | $810 | $1,350 | $540 | $150 | +$390 | Annual fee card |

How Spending Categories Change the Value of Annual Fee Cards

Many premium credit cards offer higher reward rates in specific categories such as groceries and restaurants.

Example spending breakdown for a household spending $30,000 per year on credit cards.

| Category | Annual Spending | No-Fee Card Rewards | Premium Card Rewards |

|---|---|---|---|

| Groceries | $9,000 | $135 | $450 |

| Gas & transportation | $4,000 | $60 | $80 |

| Restaurants | $3,000 | $45 | $150 |

| Other purchases | $14,000 | $210 | $280 |

| Total rewards | $450 | $960 |

Annual fee: $150

Net premium card rewards: $810

Even after the annual fee, the premium card generates significantly more rewards.

Many of the highest-earning cards for grocery spending appear in our guide to Best Cash Back Credit Cards in Canada.

Hidden Costs of Annual Fee Credit Cards

Premium cards can offer excellent rewards, but they also come with potential downsides:

- higher income requirements

- higher credit score requirements

- spending thresholds for bonuses

- temptation to overspend for rewards

For some Canadians, these factors reduce the real value of premium cards.

Cash Back vs Travel Rewards

Premium travel cards often justify annual fees through benefits such as:

- travel insurance

- airport lounge access

- trip cancellation coverage

- redemption bonuses

Cash back cards are simpler because their value is immediate.

See our full comparison: Cash Back vs Travel Rewards Credit Cards

Using Credit Cards Responsibly

Rewards should never come at the cost of financial stability.

The Financial Consumer Agency of Canada recommends:

- paying balances in full

- keeping credit utilization low

- reviewing statements regularly

- avoiding high-interest balances

Interest rates on Canadian credit cards frequently exceed 20% APR, according to the Bank of Canada.

Carrying balances at those rates quickly eliminates the value of rewards.

Quick Checklist: Should You Pay an Annual Fee?

An annual fee card may be worth it if you:

✔ spend more than $25,000 annually on your card

✔ maximize grocery or travel reward categories

✔ use travel insurance or perks

✔ earn rewards exceeding the annual fee

A no-fee card may be better if you:

✔ spend less than $15,000 annually

✔ prefer simple rewards

✔ rarely travel

✔ want zero risk of paying unnecessary fees

The Bottom Line

Annual fee credit cards can absolutely be worth it — but only if the extra rewards exceed both the annual fee and the rewards available from a strong no-fee card.

For many Canadians:

- low spenders are better off with no-fee cards

- moderate spenders may benefit from premium cards

- high spenders usually gain the most value from annual fee cards

The key is choosing a card that matches your real spending habits, not just the rewards advertised.

Frequently Asked Questions

Do annual fee credit cards improve your credit score?

No. Paying an annual fee does not directly affect your credit score. What matters is paying balances on time and maintaining low credit utilization.

Why do some credit cards charge annual fees?

Annual fees allow issuers to provide higher rewards, travel insurance, and premium benefits that basic credit cards cannot offer.

Can you cancel a credit card before the annual fee is charged?

Yes. Many Canadians cancel or downgrade cards before the next annual fee posts if the benefits no longer justify the cost.

How much should you spend for an annual fee credit card to be worth it?

In many cases, annual fee cards become worthwhile once spending exceeds $15,000–$25,000 per year, depending on the card’s reward rates and annual fee.

Affiliate Disclosure

💡 GrowingWealth.ca is supported by readers. Some of the links in this article are affiliate links, which means we may earn a small commission if you open an account or make a purchase — at no extra cost to you. We only recommend products and services we personally use, trust, or believe provide genuine value to Canadians. Our reviews and comparisons are always independent and objective.