January 1 matters for Canadians because it’s when new TFSA contribution room becomes available. More importantly, it’s the cleanest moment of the year to reset how your TFSA actually supports your finances.

This isn’t about rushing to invest or trying to be perfect on day one. It’s about positioning your TFSA so decisions throughout the year are simpler, cleaner, and less stressful.

What Actually Changes on January 1 for a TFSA

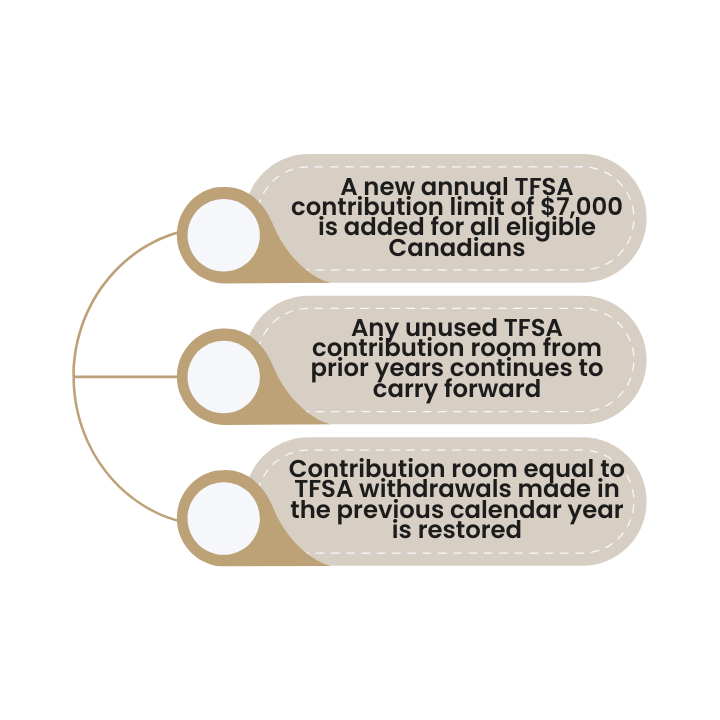

On January 1, three things happen for a TFSA:

In practical terms

Your total TFSA contribution room on January 1, 2026, is the sum of:

- Your unused contribution room from prior years

- Plus the new $7,000 for 2026

- Plus any amounts you withdrew from your TFSA during 2025

This is also a natural point to reassess whether new savings should go into a TFSA or an RRSP. If you’re unsure which makes sense for your situation, see: RRSP vs TFSA: Which Should You Use?

For official definitions and CRA guidance, refer to: Tax-Free Savings Account (CRA)

Why January 1 Is Still a Useful Reset Point

January 1 is valuable because it:

- Creates a clean planning moment before spending habits kick in

- Makes TFSA vs RRSP decisions easier to frame

- Helps you decide where future savings should live• Reduces rushed, mid-year decisions

January TFSA Reset: A Simple Checklist

1. Know Your Contribution Room (Approximately Is Fine)

You don’t need a perfect spreadsheet. You do need a reasonable estimate based on past contributions, past withdrawals, and the years you’ve been eligible.

2. Decide Whether to Contribute Now or Later

There’s no requirement to act on January 1. Contribute now if you have idle cash and clear intent, stage contributions if cash flow varies, or wait if your emergency fund isn’t solid.

3. Decide What Your TFSA Is For This Year

There’s no requirement to act on January 1. Contribute now if you have idle cash and clear intent, stage contributions if cash flow varies, or wait if your emergency fund isn’t solid.

Where New TFSA Money Should Sit in January

Using a TFSA for Cash or Short-Term Savings

For many households, this is the most practical use. A TFSA holding cash keeps interest tax-free, preserves flexibility, and acts as a buffer against uncertainty.

Recommended Platform: EQ Bank TFSA Savings Account

Using a TFSA for Long-Term Growth

Long-term investing inside a TFSA makes sense when your emergency fund is in place, you won’t need the money short-term, and you have a strategy you can stick with.

Recommended Platform: Wealthsimple TFSA

How the TFSA Fits Into a Family Finance System

The TFSA works best when it’s part of a broader structure alongside emergency funds, RRSPs, and day-to-day cash flow.

In a well-built system:

- Emergency funds reduce pressure on investing

- RRSPs handle long-term tax deferral

- TFSAs provide flexibility across life stages

This is why TFSA decisions often change over time—and that’s normal.

Related guides:

- Family Finance System – Cornerstone

- Emergency Fund Explained

- Best High-Interest Savings Accounts in Canada

When the system is clear, TFSA decisions stop feeling complicated.

What to Do on January 1 — Based on Your Situation

Rebuilding or Tight on Cash

Don’t rush to contribute. If you do contribute, keep funds accessible and focus on flexibility.

Stable but Undecided

Contribute partially or stage contributions. Use your TFSA as a holding account and revisit later.

Long-Term Focused

Contribute early if cash allows, invest according to a clear plan, and avoid unnecessary tinkering.

Final Takeaway

January 1 isn’t a deadline. It’s a reset point. You don’t need to maximize your TFSA immediately. You need to position it correctly—aligned with your cash needs and integrated into your broader plan.

Before making your January decisions, review TFSA Mistakes to avoid common pitfalls that derail TFSA strategies—like over-contributing, withdrawing strategically, or mixing up TFSA and RRSP rules.

Affiliate Disclosure

💡 GrowingWealth.ca is supported by readers. Some of the links in this article are affiliate links, which means we may earn a small commission if you open an account or make a purchase — at no extra cost to you. We only recommend products and services we personally use, trust, or believe provide genuine value to Canadians. Our reviews and comparisons are always independent and objective.