This article contains affiliate links. We may earn a commission if you open an account — at no cost to you. We only recommend products we’ve researched and trust.

Registered Accounts

Registered Accounts

TFSA rules, contribution limits, and your personal contribution room can change. Always verify current information directly with the CRA’s TFSA page and check your exact available room through CRA My Account.

In This Article

- What Is a TFSA? (And Why the Name Is Misleading)

- The Triple Tax Advantage — With Real Numbers

- 2026 TFSA Contribution Rules

- What Can You Hold in a TFSA?

- Withdrawal Rules — Including the Re-Contribution Trap

- TFSAs vs. Other Registered Accounts

- Pros and Cons of TFSAs

- How Canadian Families Use TFSAs

- TFSA Strategies for Families

- Where to Open a TFSA in Canada

- The Bottom Line

- Frequently Asked Questions

What Is a TFSA? (And Why the Name Is Misleading)

The name “Tax-Free Savings Account” undersells what this account actually is. Despite what it says on the label, a TFSA is not a savings account — it’s a tax-sheltered investment container that can hold virtually any investment you’d find in a regular brokerage account, including stocks, ETFs, bonds, GICs, and mutual funds.

The CRA describes it as “a registered savings account that functions like an investment account.” The word “savings” in the name causes many Canadians to park their TFSA money in a basic savings account earning minimal interest — and in doing so, give up years of compounding tax-free growth.

Think of the TFSA as a basket. You fill that basket with after-tax dollars, and everything inside — however it grows — is permanently sheltered from the CRA. When you take money out, you pay no tax, and you report nothing on your return. Available to any Canadian resident aged 18 or older with a valid SIN, the TFSA has been running since 2009 and has quietly become one of the most powerful wealth-building tools in the country.

Annual limit: $7,000 · Total room since 2009: $109,000 · Tax on growth: None · Tax on withdrawals: None · Eligible age: 18+ · No income requirement to contribute

One nuance worth knowing: in British Columbia, New Brunswick, Newfoundland and Labrador, the Northwest Territories, Nova Scotia, Nunavut, and Yukon, the legal age to enter a contract is 19. You cannot open a TFSA at 18 in those provinces — but your contribution room starts accumulating at 18 regardless. So if you turn 18 in a province with a 19-year age of majority, you’ll have $14,000 in room waiting for you when you can finally open the account.

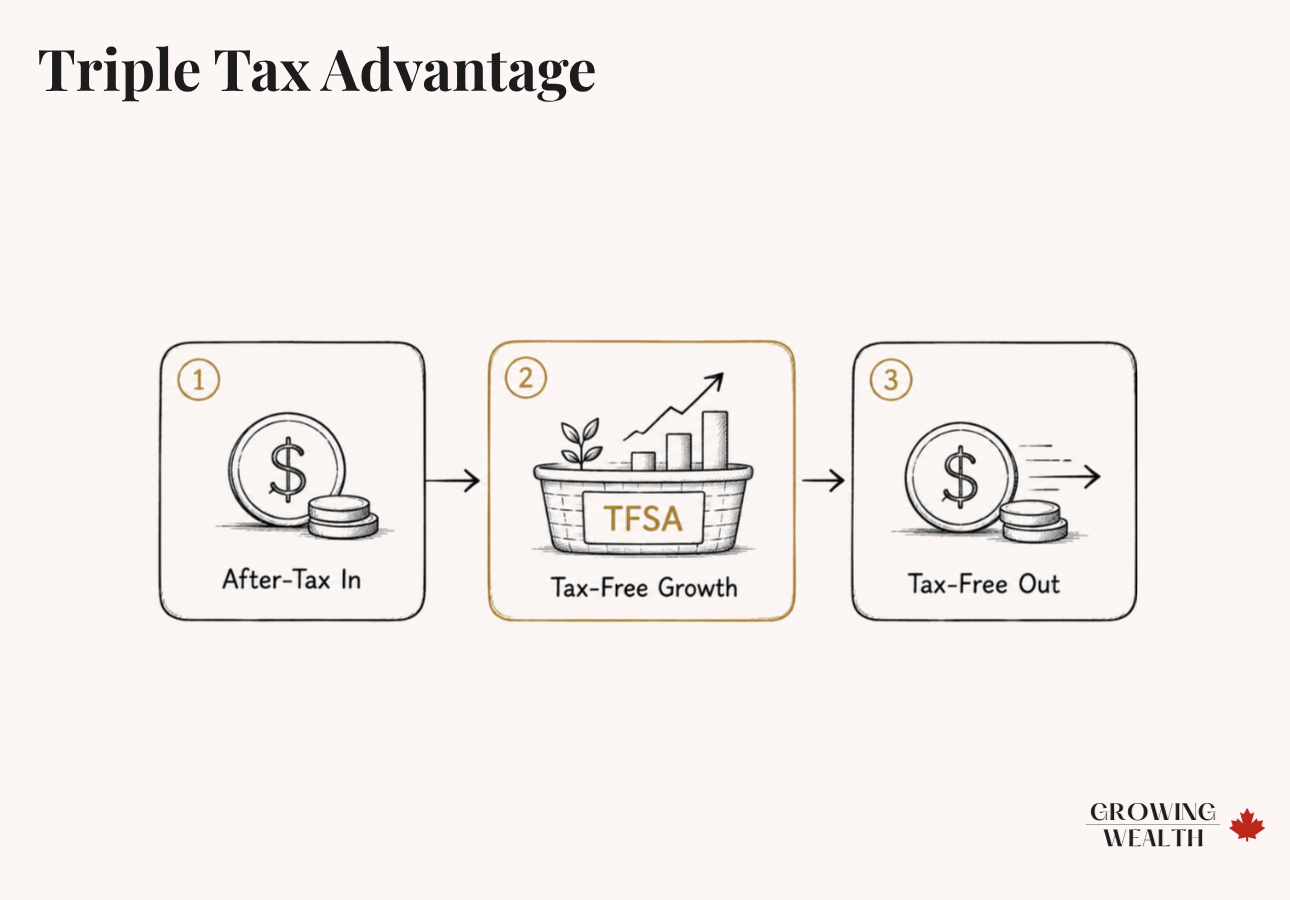

The Triple Tax Advantage — With Real Numbers

What separates the TFSA from a regular investment account is how it handles taxes at every stage.

To see what that actually means in dollars:

That gap widens significantly when you factor in annual contributions. A couple each maxing their TFSA at $7,000 per year — $14,000 combined — over 25 years at 7% annual growth would accumulate roughly $900,000. All of it completely tax-free to withdraw.

2026 TFSA Contribution Rules

Your personal contribution room

The $109,000 lifetime figure assumes you were 18 or older and a Canadian resident in 2009 when the TFSA launched. If you became eligible later — because you turned 18 after 2009, or because you immigrated to Canada — your room starts accumulating from the year you first qualified. Unused room carries forward indefinitely and never expires.

Your available room at any point is: all accumulated room to date, minus total contributions ever made, plus withdrawals from prior calendar years. The CRA tracks this in My Account for Individuals, but with a critical catch: the CRA updates their records only once per year in spring, reflecting the previous year’s transactions. If you contribute in January and check the CRA in February, your available room will look inflated. Always track your own contributions across all TFSA accounts at all institutions.

| Year(s) | Annual Limit | Running Total |

|---|---|---|

| 2009–2012 | $5,000/year | $20,000 |

| 2013–2014 | $5,500/year | $31,000 |

| 2015 | $10,000 | $41,000 |

| 2016–2018 | $5,500/year | $57,500 |

| 2019–2022 | $6,000/year | $81,500 |

| 2023 | $6,500 | $88,000 |

| 2024–2026 | $7,000/year | $109,000 |

The over-contribution penalty

Unlike RRSPs, which have a $2,000 lifetime grace buffer, the TFSA has none. Exceed your room by even $1 and you owe 1% per month on the excess for every month it stays in the account. On a $5,000 over-contribution that’s $50 a month — $600 a year — until you remove it. The CRA will eventually send a notice, but by then the penalties have compounded. If you hold multiple TFSAs at different institutions, you need to add up contributions across all of them — the $7,000 annual limit applies collectively, not per account.

For a deeper look at the most common errors, see our guide on TFSA mistakes Canadians make every year.

What Can You Hold in a TFSA?

The TFSA can hold most of the same investments as an RRSP or standard brokerage account. The right choice depends entirely on your timeline and goals.

Best for emergency funds and short-term goals. TFSA savings rates at top digital banks currently sit around 1.50%. Simple, liquid, and fully accessible.

Guaranteed returns locked for a term (1–5 years). Rates currently 3.15–4.00% depending on provider and term. Ideal for medium-term goals where you can commit the money for a defined period.

The best choice for long-term wealth building. Diversified, low-cost, and every dollar of compounding growth stays with you tax-free. Available commission-free at Wealthsimple and Questrade.

Any stock listed on a designated exchange (TSX, NYSE, NASDAQ, LSE, and roughly 43 others) qualifies. Bonds and bond ETFs suit conservative, income-focused portfolios.

One important trap for families holding US investments: US dividends paid inside a TFSA are subject to a 15% US withholding tax that cannot be recovered. This applies even though the TFSA is tax-free to Canada’s CRA — the US sees no distinction. This cost does not apply inside an RRSP, which benefits from Canada’s tax treaty with the US. For Canadian and international ETFs, the TFSA is the ideal home. For US dividend-paying stocks or ETFs specifically, the RRSP is more efficient. It’s worth knowing before you build your portfolio.

For a complete breakdown of what to hold where — and why — see our dedicated guide: What Should You Actually Hold in a TFSA?

Withdrawal Rules — Including the Re-Contribution Trap

You can withdraw from your TFSA at any time, in any amount, for any reason. No penalty, no tax, no question from the CRA about what you used the money for. This is the flexibility that makes the TFSA unlike any other registered account.

But there is one rule that catches Canadians off guard every year — and it’s responsible for more unexpected CRA penalties than almost anything else about the TFSA:

When you withdraw from your TFSA, that room is not immediately restored. It comes back on January 1 of the following year. If you withdraw $10,000 in June 2026, you cannot re-contribute that $10,000 until January 1, 2027 — unless you have other unused room available. Re-contributing in the same calendar year without available room counts as an over-contribution and triggers the 1% monthly penalty.

The account feels intuitive — put money in, take it out, put it back. But it keeps a calendar-year ledger, not a running balance. If you’re planning to use your TFSA for a goal and then rebuild it — a down payment, a renovation, a large purchase — plan around the January 1 reset date.

One other note: if you become a non-resident of Canada, keep your TFSA open but stop contributing. Any contributions made while you are a non-resident are subject to a 1% monthly penalty for every month they remain in the account.

TFSAs vs. Other Registered Accounts

The TFSA is one of four registered accounts most Canadian families need to understand. Each serves a different purpose — the best financial plan typically uses several in combination, not just one.

| Account | Tax on Contributions | Tax on Withdrawals | Best Use | 2026 Limit |

|---|---|---|---|---|

| TFSA | No deduction | Tax-free | Any goal — flexibility and lifelong tax-free growth | $7,000/yr ($109,000 lifetime) |

| RRSP | Tax-deductible | Taxed as income | Retirement savings — best for higher earners now | 18% of income, max $33,810 |

| FHSA | Tax-deductible | Tax-free (if used for home) | First-time home purchase — only | $8,000/yr, $40,000 lifetime |

| RESP | No deduction | Taxed to student (typically low) | Education savings for children | $50,000 lifetime per child |

The rule of thumb: if your household income is below roughly $60,000, the TFSA almost always outperforms the RRSP — your marginal rate is lower, so the RRSP’s upfront deduction is worth less, and the TFSA’s tax-free withdrawals in retirement protect your income-tested benefits. Above $80,000–$90,000, the RRSP deduction becomes significantly more valuable and both accounts should be running together.

If you’re buying your first home, the FHSA deserves serious consideration before you fill the TFSA — it gives you both the RRSP-style deduction and tax-free withdrawals on up to $40,000. That’s a double tax benefit that the TFSA alone cannot match for first-time buyers.

Not sure which account to prioritize? Our FHSA vs TFSA vs RRSP comparison works through the decision by income level and goal. And if you’re wondering whether to hold both a TFSA and an RRSP simultaneously, see Why Most Canadians Should Have Both.

Pros and Cons of TFSAs

- All growth — interest, dividends, capital gains — is permanently tax-free, even when withdrawn

- Withdraw any amount, at any time, for any purpose with zero tax consequences

- Withdrawn amounts are restored as contribution room on January 1 of the following year

- No earned income requirement — retirees, students, and stay-at-home parents all qualify

- Withdrawals don’t count as income and have no impact on CCB, OAS, GIS, or GST/HST credits

- Can hold cash, GICs, ETFs, stocks, bonds, and mutual funds

- Contributions are not tax-deductible — no upfront tax break the way an RRSP provides

- Annual room of $7,000 is modest; unlikely to fund retirement entirely on its own

- Over-contributions trigger a 1% monthly penalty with no grace buffer

- Withdrawn amounts don’t restore contribution room until January 1 of the following year

- US dividends face a 15% withholding tax inside a TFSA that cannot be recovered

How Canadian Families Use TFSAs

The TFSA’s flexibility is what makes it so useful for families — unlike the RESP, RRSP, or FHSA, there are no restrictions on what you use the money for. These are the four most common scenarios.

Sarah and Daniel keep $20,000 in a TFSA high-interest savings account at EQ Bank. It earns tax-free interest at 1.50% and is fully accessible if a furnace dies or a car needs replacing. Because the money is in a TFSA rather than a regular savings account, every dollar of interest stays with them. When they had it in a regular account, they were paying roughly $80/year in tax on that interest at their combined marginal rate — not life-changing, but the TFSA costs them nothing extra to run, so why give the money away.

Marcus and Priya are saving $50,000 for a down payment. They’ve each maxed their FHSA first — $8,000 per year each — because the FHSA gives both a tax deduction and tax-free withdrawal, a double benefit the TFSA can’t match for first-time buyers. Everything above the FHSA cap goes into the TFSA, invested in a short-duration bond ETF. When they close on their home, they pull the TFSA money tax-free to cover closing costs, legal fees, and the first round of renovations — expenses the FHSA can’t touch.

The Nguyen family maxes their RESP contributions to capture the full Canada Education Savings Grant ($500/year per child). But they also know the RESP has restrictions — it must be used for education, and their kids may not go to a college or university. Their TFSA runs alongside as a flexible backstop: if both kids go to school, the RESP covers tuition and the TFSA covers living costs and fees now. If one child skips post-secondary, the TFSA money remains theirs — no strings attached, no penalties.

Claire works full-time and contributes to her RRSP. Her husband James cares for their two children and has no earned income — which means he has no RRSP contribution room. But both accumulate $7,000 in TFSA room every year, regardless of who earns what. Claire contributes to her own TFSA and, where she has spare cash, gives James money to contribute to his. In retirement, James’s TFSA withdrawals come out tax-free and count as zero income — protecting their OAS and any income-tested benefits. It’s one of the cleanest income-splitting strategies available to Canadian couples.

TFSA Strategies for Families

In 2026, a couple has $14,000 in combined annual TFSA room. Maxing both accounts before adding to taxable investments is almost always the right first step — the tax-free compounding advantage is difficult to replicate outside a registered account. If cash is tight, prioritize the spouse in the higher tax bracket first, since they stand to gain the most from sheltering future growth.

The right account type depends on your timeline. For money you might need within one to three years — an emergency fund, a near-term renovation — a HISA TFSA or a GIC TFSA makes sense: guaranteed return, fully liquid or known maturity date. For money you won’t touch for five years or more, an investment TFSA holding low-cost ETFs gives you the full benefit of tax-free compounding. Holding two separate TFSAs at different providers for different purposes is completely legal and often the practical move.

Set up an automatic transfer to your TFSA on the day your pay arrives. A family contributing $583/month hits the $7,000 annual limit with no further decisions required. Automation removes the friction entirely, which is the point — the best financial habit is one you only have to make once.

A TFSA is a powerful tool, but not when you’re carrying credit card debt at 19–22% interest. The after-tax return on paying off that debt is guaranteed and far higher than any investment return available inside a TFSA. Clear high-interest debt first, then redirect to the account. This is not a nuanced position — it’s arithmetic.

The TFSA’s value multiplies when you hold high-growth investments. A $7,000 contribution earning 1.50% in a savings account grows to about $8,100 in 10 years. The same $7,000 in a diversified ETF at 7% annual growth becomes roughly $13,800 — and not one dollar of that $6,800 in gains is taxable. The more growth potential the investment has, the more powerful the TFSA shelter becomes. Don’t let the name convince you it’s just a savings account.

For a full breakdown of what to actually hold inside the account at each life stage, see: What Should You Actually Hold in a TFSA?

And if you’re working through how to split money between your TFSA and RRSP — or whether to run both — start with Why Most Canadians Should Have Both a TFSA and an RRSP.

Where to Open a TFSA in Canada

The right provider depends on what you’re using your TFSA for. For savings and short-term goals, the interest rate and fee structure matter most. For long-term investing, look at trading costs, investment selection, and platform quality.

EQ Bank offers one of the most complete product lineups among Canadian digital banks. Their TFSA savings account pays 1.50%, and their GICs range from 3.15% to 3.75% across 13 terms — among the best available in Canada. Zero fees, strong CDIC insurance up to $100,000, and a clean platform. Their everyday Personal Account pays 2.75%, making EQ a strong choice for families who want a reliable, no-maintenance place for both registered and non-registered savings.

Open an EQ Bank TFSA →Wealthsimple is the easiest way to hold a fully invested TFSA in Canada. Commission-free trading on Canadian and US stocks and ETFs, a clean mobile app, and a managed portfolio option for families who’d rather automate the investing entirely. No account minimums, no monthly fees. For most Canadian families opening an investment TFSA for the first time, Wealthsimple is the right starting point.

Open a Wealthsimple TFSA →- Emergency fund or short-term savings → EQ Bank (HISA or GICs)

- Long-term investing → Wealthsimple (beginner) or Questrade (DIY)

- Want everything in one place → Big Six bank, though rates will be significantly lower

- Already at a big bank → Open a second TFSA at EQ or Wealthsimple — holding multiple TFSAs simultaneously is completely legal

The Bottom Line

The TFSA is the most flexible registered account in Canada, and for most families it should be the first account they open and the last one they stop using. The tax-free growth is permanent — not deferred, not conditional, permanently sheltered from the CRA. Every dollar of compounding stays with you.

If your household income is below $60,000, the TFSA almost always beats the RRSP — contribute here first. If you earn more, the RRSP’s upfront deduction becomes more valuable, but the TFSA should still run alongside it. If you’re buying your first home, open an FHSA before filling the TFSA — you get a tax deduction and tax-free withdrawals on $40,000, a double benefit the TFSA alone can’t match. And if you have a spouse, max both TFSAs before directing money into a taxable account. That $14,000 of combined annual room is the most tax-efficient savings vehicle available to Canadian families at almost every income level.

The one rule to keep front of mind: withdrawn amounts don’t restore your contribution room until January 1 of the following year. That single rule catches more Canadians off guard than anything else about this account.Now that you know how the TFSA works, the next decision is what to actually put inside it. Read What Should You Actually Hold in a TFSA? — a complete breakdown of the right investments for each goal and timeline.

Frequently Asked Questions

Yes — there is no limit on the number of TFSAs you can hold at different institutions. However, your contribution room is shared across all of them. If your annual room is $7,000 and you hold three TFSAs, that $7,000 applies across all three combined. You cannot contribute $7,000 to each. Holding multiple TFSAs is practical if you want a savings account at one provider and an investment account at another, but tracking your contributions carefully becomes even more important when they’re spread across institutions.

If you name your spouse or common-law partner as a successor holder, the TFSA transfers to them intact — they absorb the account and its contribution room with no tax consequences and without affecting their own TFSA room. If you name anyone else as a beneficiary (children, siblings), the account pays out tax-free up to the date of death, but any growth earned after that date may be taxable. For married couples, naming your spouse as successor holder rather than beneficiary is almost always the better structure.

You can give your spouse money to contribute to their own TFSA, and unlike with RRSPs, there are no attribution rules — income earned inside their TFSA stays theirs with no tax consequences to you. The contribution uses their room, not yours. This is one of the cleanest income-splitting strategies available to Canadian couples, particularly useful when one spouse is in a lower tax bracket or has no earned income — such as a stay-at-home parent who can’t build RRSP room.

Log in to CRA My Account for Individuals — your available room is shown there. But the CRA updates this figure only once per year in spring, reflecting the previous year’s transactions. If you’ve contributed in the current calendar year, the CRA’s display won’t reflect it yet and your available room will look inflated. The most reliable method is to track it yourself: total accumulated room to date, minus all contributions you’ve ever made, plus all withdrawals from prior years. If you hold TFSAs at multiple institutions, you need to add up contributions across all of them.

You’ll owe 1% tax per month on the excess amount for every month it remains in the account. There’s no grace buffer — the penalty starts from the first dollar over your limit. The CRA will send a notice and a tax bill, but by the time you receive it, months of penalties may have accumulated. Remove the excess immediately once you realize the error to stop the penalty from growing. The CRA can waive penalties in cases of genuine mistake if you act quickly and apply in writing, but this is not guaranteed.

If your income is below roughly $60,000, the TFSA typically wins — your marginal rate is lower, so the RRSP’s upfront deduction is worth less, and TFSA withdrawals in retirement protect income-tested benefits. Above $80,000–$90,000, the RRSP deduction becomes significantly more valuable and both accounts should run together. Between those thresholds, it depends on your expected retirement income and whether benefit clawbacks are a concern. For a full breakdown by income level, see our RRSP vs TFSA guide.

Yes — US stocks and ETFs listed on designated exchanges (NYSE, NASDAQ, and others) are qualified TFSA investments. However, US dividends paid inside a TFSA are subject to a 15% US withholding tax that cannot be recovered, even though the TFSA is tax-free to the CRA. This cost does not apply inside an RRSP, which benefits from Canada’s tax treaty with the US. For Canadian and internationally diversified ETFs, the TFSA is ideal. For US dividend-paying stocks or dividend ETFs, consider holding those specifically inside your RRSP instead.

Your room starts accumulating in the year you turn 18, not from 2009. If you turned 18 in 2020, your total accumulated room as of 2026 is the sum of annual limits from 2020 through 2026: $6,000 + $6,000 + $6,000 + $6,500 + $7,000 + $7,000 + $7,000 = $45,500. Room builds on January 1 of each year — so even if your birthday falls on December 31, you receive the full year’s contribution room for the year you turn 18.